Military Health System Achievements in 2019 Provide Strong Foundation for Year Ahead

Here’s a link to this article from the Defense Health Agency:

Military Health System Achievements in 2019 Provide Strong Foundation for Year Ahead

Will the Government Ever Get Rid of the “Free Lunch” of the TSP G Fund?

They say there’s no free lunch, but in the Thrift Savings Plan there is a free lunch, and it’s called the G Fund. Will the government get rid of this free lunch?

The G Fund Free Lunch

What is this free lunch? You can read about it on this page in the Rewards section:

The G Fund interest rate calculation is based on the weighted average yield of all outstanding Treasury notes and bonds with 4 or more years to maturity. As a result, participants who invest in the G Fund are rewarded with a long-term rate on what is essentially a short-term security. Generally, long-term interest rates are higher than short-term rates.

The government is paying you a higher interest rate than it should. That is the G Fund free lunch.

Why is the Free Lunch at Risk?

The government periodically considers getting rid of it. For example, you can read about it in this article, which is discussing the President’s FY19 budget plan/request. Here’s the relevant portion:

The plan also proposes reducing the statutorily mandated rate of return for the government securities (G) fund to be based on either the three-month or four-week Treasury bill, at a projected savings of $8.9 billion over 10 years.

“G Fund investors benefit from receiving a medium-term Treasury Bond rate of return on what is essentially a short-term security,” the White House wrote. “The budget would instead base the G-fund yield on a short-term T-bill rate.”

TSP spokeswoman Kim Weaver said changing the G Fund’s yield, which is currently 2.75 percent annually, would have a disastrous effect on participants’ ability to save for retirement. If Congress changed the G Fund to track the three-month Treasury bill, the yield would decrease to 1.46 percent, and for the four-week bill it would drop to 1.43 percent.

“Such a change would make the G Fund inadequate and ineffective from an investment standpoint for TSP participants who are saving for retirement,” Weaver said in an email. “More than 3.6 million TSP participants (69 percent) have all or some of their account balance invested in the G Fund. Of those with money in the G Fund, 2 million (39 percent) hold the G Fund as their sole investment choice.”

For a TSP participant who has just retired and is invested entirely in the L Income Fund, which is designed for people who have begun taking annuity payments, they would run out of money at age 84 instead of the current projected age of 92, Weaver said.

Jessica Klement, staff vice president for advocacy at the National Active and Retired Federal Employees Association, said the change would make G Fund investments “useless” and likely force TSP administrators to divest from it entirely.

“[The new rate] would not even keep up with inflation,” she said. “So if you wanted to keep your money in a mostly secure fund, you would not be getting any return, and you’d actually be losing money. And if you took your money out, there would be no other safe, secure investment for those nearing or in retirement.”

What Does This Mean For You?

Right now, it means nothing. This is all just discussion about something that might happen in the future.

What you do need to understand, though, is that the G Fund serves a specific purpose in your portfolio. As the TSP site says:

Consider investing in the G Fund if you would like to have all or a portion of your TSP account completely protected from loss. If you choose to invest in the G Fund, you are placing a higher priority on the stability and preservation of your money than on the opportunity to potentially achieve greater long-term growth in your account through investment in the other TSP funds.

It is alarming that Ms. Weaver from the TSP said, “Of those with money in the G Fund, 2 million (39 percent) hold the G Fund as their sole investment choice.” Those 2 millions people are sacrificing long-term growth for the safest and most conservative investment available in the TSP.

There’s nothing wrong with that if you’re doing it because you are very conservative, near retirement, or the G Fund serves as the bond portion of a larger, more diversified portfolio that has more risky assets like stocks or real estate.

The sad reality is that most who are solely invested in the G Fund are that way because it used to be the default option for those starting a TSP account, and they never switched it to a more aggressive investment option. Under the new Blended Retirement System, the default investment switched from the G Fund to an age-appropriate Lifecycle fund.

What’s the Bottom Line?

The G Fund gives you a free lunch, paying you a higher long-term interest rate while you are investing in short-term securities. The government periodically talks about getting rid of that free lunch.

If you are invested in the G Fund, make sure you are doing it purposely and are aware of its conservative nature. Its emphasis is on preserving wealth rather than growing wealth.

Check Your Beneficiary Designations

Here’s a tip from one of my favorite blogs and authors, Jonathan Clements from Humble Dollar:

CHECK YOUR BENEFICIARY DESIGNATIONS. Your retirement accounts and life insurance will typically pass to the beneficiaries specified on those accounts, not the people named in your will. If your family situation has changed, or you simply don’t remember who you listed, take a moment to review your beneficiary designations.

Don’t let the ex-spouse get your money when you die! Update your beneficiaries.

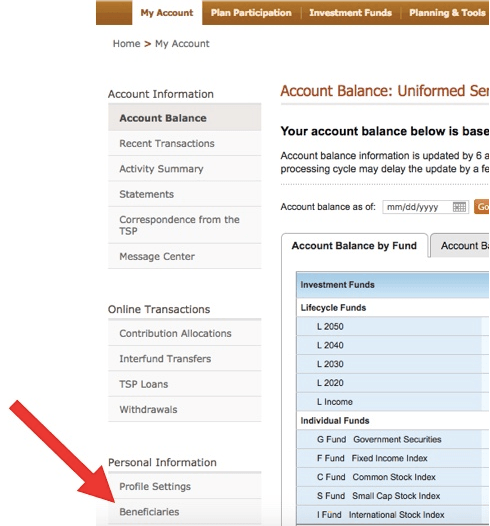

How to See Your Beneficiaries for the Thrift Savings Plan (TSP)

If you log on to the TSP page, you need to click on the link along the lower left, marked by the large red arrow:

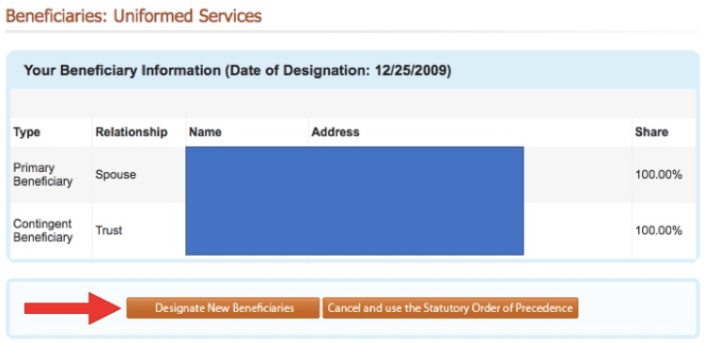

Then you’ll see this, and you can change them at the bottom:

Then you’ll see this, and you can change them at the bottom:

Invest in Your Taxable Account Thoughtfully

Here’s a tip on investing in your taxable account from one of my favorite blogs and authors, Jonathan Clements from Humble Dollar:

INVEST YOUR TAXABLE ACCOUNT THOUGHTFULLY. If you purchase the wrong investments in your taxable account, you may be reluctant to sell, because you’ll trigger capital gains taxes. A good choice: low-cost U.S. and international total stock market index funds, which should be tax-efficient—and which shouldn’t ever lag far behind the market averages.

For those of us in the military, investing in a taxable account comes into play in a few scenarios…

Scenario #1 – You and your spouse (if you have one) have filled your Thrift Savings Plan (TSP) and all other retirement accounts available including IRAs, yet you want to save more for retirement. In this case, you put the rest in a taxable account with the investment company of your choice (Vanguard, Fidelity, Schwab, etc.). This is what I do when all of my retirement accounts are full, and just like Jonathan mentions I invest purely in broad, low-cost index funds at Vanguard. The only taxable holdings I have are the Vanguard U.S. and international total stock market index funds.

Scenario #2 – You are saving for a financial goal that is not related to retirement, such as a downpayment on a home or for a new car. If you’re saving for college, you’d use a 529 plan, but for just about anything else you could use a taxable account. For example, I have my emergency money and extra spending money in a money market fund among my taxable accounts. The alternative to this is to use a bank and invest in a high-yield savings account, a certificate of deposit (CD), or a money market account. Bankrate.com will show you the best rates for each of these reasonable alternatives.

If you are using a taxable account, there are a few things to consider. If you are investing in bonds, you may want to invest in municipal bonds in your taxable account due to the tax benefits. If you are a fan of target date funds, you may not want to use them in a taxable account because the bond portion will kick off income that is taxed at your full marginal tax rate. Most feel that bonds are better placed in a tax-advantaged retirement account unless you are using municipal bonds.

Can You Now Sue the Military for Medical Malpractice?

Here’s a Navy Times article that answers that question:

Explainer: Can you now sue the military for medical malpractice?

MOAA – President Signs NDAA: What the Law Includes, and What’s Next

Here’s a link to this good NDAA summary:

President Signs NDAA: What the Law Includes, and What’s Next

Finance Friday Articles

Here are my favorites this week:

10 Things That Matter Most In Personal Finance

End of the Year Financial Checklist for High Earners

Here are the rest of this week’s articles:

7 Things to Learn From the Periodic Table of Investment Returns

Creating a Personal Finance Curriculum: 5 Questions

Big overhaul set for IRAs could be more or less taxing

Explaining the Different Types of Real Estate Crowdfunding Platforms

Eyes Forward – Saving vs Spending

How Did These Physicians Create Passive Income?

Joining a Cult: The Financial Independence Counterculture

Military spouses will get reimbursed up to $1,000 for professional relicensing costs

Real Estate Investing for Doctors

Retirement and 529 Changes from the SECURE Act

Six Months of Part-Time Work. Or How to Save $60,000 on Taxes.

Throwback Thursday Classic Post – How to Be Considered for Promotion if You’ve Been on Active Duty for Less Than 1 Year

The FY21 promotion board NAVADMIN was released in December. If you are in-zone or above-zone for an upcoming promotion board but you’ve been on active duty for less than 1 year, you should read #5 from the NAVADMIN, which says:

5. In-zone and above-zone eligible officers in the grades of lieutenant,

lieutenant commander, and commander, whose placement on the Active-Duty List

is within one year of the convening dates of these boards, are automatically

deferred unless they specifically request to be considered. The officer may

waive this deferment and request consideration for promotion, in writing,

emailed to NPC_Officer_SELBD_Elig_Waivers.fct@navy.mil or mailed to:Commander, Navy Personnel Command (PERS-802)

5720 Integrity Drive

Millington, TN 38055-0000The request must be received by PERS-80 not later than 30 days prior to the

convening date of the board. All officers are reminded it is their

responsibility to ensure their personnel records are substantially accurate

and complete.

What does this mean and why would it apply to you? Maybe you had prior service, you went to medical school, and now you’re a senior LT who is in-zone for LCDR right away. Maybe you did a civilian NADDS residency and you are in-zone right away for LCDR. There might be other situations that would put you in this position, like getting time-in-grade credit for a PhD.

If you believe you are in this position, here is what I’d do:

- Confirm you are in-zone or above-zone. How can you do this? The easiest way is to either read the Promo Prep or get the FY21 lineal list. Or you can use this document from PERS.

- If you wish to be considered for promotion to LCDR, CDR, or CAPT, so what it says above. Send the letter simply requesting this. It can probably be a very short letter. There is no need to be verbose.

- Finally, contact PERS-802: Selection Board Eligibility Branch because I know people who did only #2 (sent a letter) and were not considered. Here’s what their website says:

If you have questions concerning promotion boards, eligibility for promotion boards, please contact the MyNavy Career Center at (833) 330-MNCC or askmncc@navy.mil.

- PERS-802, Branch Head: (901) 874-4537

- Officer Active and Reserve Eligibility Section, Lead: (901) 874-3324

- Enlisted Active and Reserve Eligibility Section, Lead: (901) 874-3217

- Also, here is a great article on this topic from the August 2018 Medical Corps Newsletter:

6 Director Positions Available in Southern California – Merry Christmas!

Naval Hospital Camp Pendleton will have the following leadership positions available this upcoming spring/summer:

- Director, Branch Clinics (March 2020)

- Director, Medical Services (March 2020)

- Director, Public Health (June 2020)

- Director, Mental Health (June 2020)

- Research Medical Director (June 2020)

- Designated Institutional Official (June 2020)

All position descriptions are above. They are available to all Corps who are in the PCS window for next summer. This is probably clear, but you need Detailer clearance to apply if you are not already inbound or at NHCP. I’m sure an e-mail from the Detailer would suffice.

Interested applicants can submit their CV, Bio, and Letter of Intent to CDR Dave Lang (the DFA at NHCP – contact info in the global) by 31 January 2020 (for Branch Clinics and Medical Services), and 1 March 2020 for the remaining positions.

Merry Christmas!