Author: Joel Schofer, MD, MBA, CPE

DHA FY21 Campaign Plan

Here is the DHA’s FY21 strategic plan:

Updated Awards Section in Promo Prep

I’m slowly but steadily working on the 2021 version of the Promo Prep and Fitrep Prep, but because Navy Personnel Command retired NDAWS (awards.navy.mil) and now uses BOL for awards, the awards section needed to be updated. The version with the updated awards section has been uploaded to the Promo Prep page.

Bottom Line – If your awards are accurate on your OSR, there is no action to take. If they are not, have fun!

Buy the Big Three

Jonathan Clements was a longtime personal finance columnist for The Wall Street Journal, and he offers great advice at the best price you can get (free) on his blog Humble Dollar. Here is one piece of advice from his site:

“BUY THE BIG THREE. The global market portfolio consists of four major sectors, roughly equal in size: U.S. stocks, U.S. bonds, foreign shares and foreign bonds. Arguably, foreign bonds are optional, offering modest yields but wild currency swings. The other three sectors, however, are crucial to a diversified portfolio. Do you have enough exposure to all three?”

It’s a good thing that Mr. Clements considers foreign bonds optional, because they are not available in the Thrift Savings Plan (TSP). The rest of the asset classes are, though. U.S. stocks can be purchased in the C and S funds. U.S. bonds in the G and F funds. The I fund will get your foreign stocks, albeit not in any emerging markets.

In other words, you can get “the big three” very easily in the TSP. If you missed it, you can read about the TSP and all its funds here in my TSP guide.

Multiple Navy NEJM Articles on COVID-19 Outbreak

Below are the recent Navy Medicine related NEJM articles. Congrats to the multiple Navy authors!

- SARS-CoV-2 Transmission among Marine Recruits during Quarantine

- An Outbreak of Covid-19 on an Aircraft Carrier

- SARS-CoV-2 in the U.S. Military — Lessons for Civil Society

Below is a summary story from BUMED about the aircraft carrier article:

Courtesy Story

U.S. Navy Bureau of Medicine and Surgery

A multidisciplinary team of US Navy Medicine personnel published a comprehensive analysis of the USS Theodore Roosevelt SARS-CoV-2 outbreak of spring 2020 in the New England Journal of Medicine on November 11.

While preliminary findings and a CDC MMWR report were released in June from a limited population, this paper provides an epidemiological description of the outbreak that includes all of the crew.

The paper contributes to the growing body of knowledge on the behavior of the new coronavirus and will support continued efforts to stem the impact of the virus in the Navy, in the United States and around the world.

Over the course of the outbreak, 1,271 sailors (27 percent of the crew) tested positive for severe acute respiratory syndrome coronavirus 2 (SARS-CoV-2) by rRT-PCR testing. The authors found that working in confined spaces, enlisted rank, history of angiotensin converting enzyme inhibitor use, respiratory disease, and obese body mass index were associated with an increased risk of infection.

In their conclusions, the authors noted SARS-CoV-2 spread quickly among the USS Theodore Roosevelt’s crew. Transmission was facilitated by close quarters and asymptomatic and pre-symptomatically infected crewmembers. Nearly half of those who tested positive for the virus never developed symptoms. These findings show that young, healthy working-age adults can play a role in the spread of SARS-CoV-2.

“We must continue to be aggressive about studying COVID-19 and SARS-CoV-2,” said co-author of the paper, Lt. Cmdr. Matthew Kasper. “It’s about keeping our operational forces ready and underway, protecting the health of our personnel, while contributing to the general body of knowledge of this virus.”

The New England Journal of Medicine article can be found here.

App for Military Resources Available to Service Members, Families

Here’s an article about the new My Military OneSource app:

App for Military Resources Available to Service Members, Families

It has resources to aid with:

- Child care options

- Relationship counseling

- Domestic violence awareness

- Parenting tips

- A Morale, Welfare and Recreation Program digital library

- Tips for communicating in a long-distance relationship

- Moving and housing

- Tax services

- Confidential help

- Financial and legal assistance

- Education and employment

- Confidential non-medical counseling

- Health and wellness

- Benefits finder

- Recreation, travel and shopping

- Installation program directory

Finance Friday Articles

There are continued pushes to keep the TSP I Fund from investing in China and other emerging markets:

Senate Measure Backs Pay Freeze, I Fund Limitation

Here are this week’s articles:

MTF Transition Update from ASD(HA) and DHA

Here is the message from the ASD(HA):

MHS Team:

As you know, we have been on a temporary pause in our implementation plan to transition the administration and management of military medical treatment facilities from the Military Departments to the Defense Health Agency. Yesterday, the Secretary lifted this pause and directed that we continue implementation of the transition in accordance with Section 702 of the FY2017 National Defense Authorization Act. Attached you will find yesterday’s guidance from the Secretary (note that I did not attach this as I was uncomfortable putting a SECDEF memo on a blog, but you can see it here if you have a CAC reader and can log onto MilSuite).

I am confident we will achieve this important Military Health System milestone through collaboration between the DHA and the Military Departments with a continued focus on sustaining a ready medical force and a medically ready force while supporting our 9.6 million beneficiaries across the globe.

— Tom

Here is the message from DHA:

This week we received guidance from both the Secretary of Defense and the Assistant Secretary of Defense for Health Affairs to resume the transition of MTF administration and management from the Military Departments (MILDEPs) to the DHA in support of our implementation plan. Paraphrasing the Secretary, he charged DHA with three priorities: ensuring the delivery of high-quality health care, utilize the MTFs as much as possible for readiness workload, and ensuring the medical readiness of the force. We must work collaboratively with our colleagues in the Services to implement a smooth and successful transition while ensuring safe, high-quality care for our 9.6 million beneficiaries. You can read the complete memorandum from the Secretary of Defense here:

Throwback Thursday Classic Post: TSP Fund Deep Dive – The I Fund – The TSP’s Most Controversial Fund

There are only five investments available in the Thrift Savings Plan (TSP), so let’s take a detailed look at them one at a time. In this post we’ll cover the I Fund, which is the most controversial of all the TSP funds.

What’s all the controversy? You can read about it below, but to give you a preview it is because of two things.

First, investment experts disagree on how much of your investments should go into international stocks, which is what the I Fund is composed of.

Second, the I Fund misses out on a key portion of a comprehensive international stock portfolio, emerging markets.

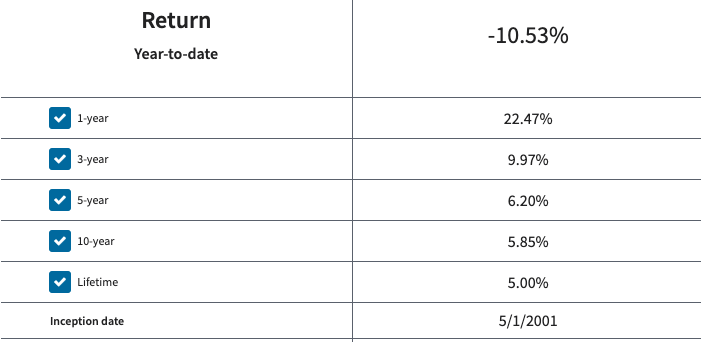

Inception Date

1 MAY 2001

Fund Management

The Federal Retirement Thrift Investment Board currently contracts BlackRock Institutional Trust Company, N.A. (BlackRock) to manage the I Fund assets. The I Fund remains invested regardless of the performance of the securities markets or the overall economy.

Investment Strategy

The I Fund is invested in a stock index fund that invests in international stocks of more than 20 developed countries. The I Fund’s objective is to match the performance of the MSCI EAFE (Europe, Australasia, Far East) Index. Also, some of the money in the I Fund is temporarily invested in the G Fund and earns the G Fund return.

The I Fund is a passively managed fund that remains invested according to its indexed investment strategy regardless of stock market movements or general economic conditions.

What is the Risk?

Your investment in the I Fund is subject to market risk because the prices of the stocks it invests in rise and fall. You are also exposed to inflation risk, meaning your I Fund investment may not grow enough to offset inflation. Unlike the C or S Funds, you are also exposed to currency risk. What’s that? The TSP defines it as:

The risk that the value of a currency will rise or fall relative to the value of other currencies. Currency risk could affect investments in the I Fund because of fluctuations in the value of the U.S. dollar in relation to the currencies of the 22 countries in the EAFE index.

Because of its exposure to currency risk, the I Fund returns will rise or fall as the value of the U.S. dollar decreases or increases relative to the value of the currencies of the countries represented in the EAFE index.

What is the Benefit?

Historically, this increased risk has been rewarded with an increased return. It offers the opportunity to experience gains from equity ownership of international stocks of more than 20 developed countries. Here is all the performance data as of 7 NOV 2020:

Types of Earnings

The I Fund changes in value as the market price of its stocks change. In addition, the I Fund makes money for its investors when those stocks pay dividends. Unlike a traditional mutual fund, though, income from dividends is included in the share price calculation. It is not paid directly to participants’ accounts. Finally, the I fund will change in value due to currency risk, as described above.

It also makes some money on interest on short-term investments and securities lending income.

BlackRock credits interest and dividend income each business day. This income is then reflected in the TSP share prices.

Share Price Calculations

The value of your account is determined each business day based on the daily share price and the number of shares you hold. At the end of each business day, after the stock and bond markets have closed, the total value of the funds’ holdings (net of accrued administrative expenses) is divided by the total number of shares outstanding to determine the share price for that day. The daily change in TSP share prices reflects all investment income (interest on short-term investments, dividends, capital gains or losses, and securities lending income) net of TSP administrative expenses.

Expenses

The net expenses paid by investors is 0.042% or 4.2 basis points, which like all the TSP funds is ridiculously low and is a major benefit of the TSP. It cost $0.42 for each $1,000 invested.

How Should I Use the I Fund in my TSP Account?

The I Fund can be useful in a portfolio that also contains stock funds that track other indices, such as the C Fund (which tracks an index of large U.S. company stocks) and the S Fund (which tracks an index of small-medium U.S. company stocks). The C, S, and I Funds track different segments of the global stock market without overlapping. This is important because the prices of stocks in each market segment don’t always move in the same direction or by the same amount at the same time. By investing in all segments of the stock market (as opposed to just one), you reduce your exposure to market risk.

The controversy among investment experts, though, is how much of your stock portfolio should be invested internationally. You’ll find respected investment experts who recommend anywhere from 0% of your stocks being invested in international markets (like John Bogle, the founder of Vanguard) to about 50%. An extensive discussion on this can be found in Step 4 of our Crush the TSP Series – Invest. What’s the bottom line? Here is what I think…

A 40% international allocation is between the 0% Bogle viewpoint and the 50% global weighting viewpoint, so it seems fine to me and that is what I do. Ultimately, you can pick anywhere from 0% to 50% and find someone really smart who agrees with you. I’d encourage you to have some exposure to international, so I’d say you should pick at least 20%, but it really is up to you.

The I Fund can also be useful in a portfolio that contains bonds. Again, it is because the prices of stocks and bonds don’t always move in the same direction or by the same amount at the same time. So a retirement portfolio that contains a bond fund like the F Fund, along with other stock funds, like the C and S Funds, will tend to be less volatile than one that contains stock funds alone.

Advice from My Favorite Short Investing Book

Here is what my favorite investing book, The Elements of Investing: Easy Lessons for Every Investor, says about international stock funds like the I Fund:

We do believe that investors should combine one of the total U.S. stock market index funds with a total international stock market index fund.

How do you do this with the TSP? Well…you can’t, and that is why the I Fund is controversial.

If you want to invest in the total US stock market, you just combine the C Fund with the S Fund in a 3:1 ratio. To see how I use the S Fund, read the Crush the TSP series.

But you cannot invest in a total international stock market index fund in the TSP because the I Fund is its only international stock option and it does not invest in emerging markets. Emerging markets include some of the largest economies in the world, like China and India. You can read more about emerging markets here.

At one point, the TSP was going to have the I Fund switch its index to include emerging markets. They were going to be switching to the MSCI All Country World Index Ex-U.S. index, which is broader and includes both developed and emerging markets. These efforts were halted, however, due to controversy about investing in China.

Until this change occurs, you won’t be able to use the TSP to invest in a total international stock market index fund because that is what the I Fund will be. That’s why all my international stock exposure is through my investments at Vanguard.