Author: Joel Schofer, MD, MBA, CPE

Invest Your Taxable Account Thoughtfully

Jonathan Clements was a longtime personal finance columnist for The Wall Street Journal, and he offers great advice at the best price you can get (free) on his blog Humble Dollar. Here is one piece of advice from his site:

“INVEST YOUR TAXABLE ACCOUNT THOUGHTFULLY. If you purchase the wrong investments in your taxable account, you may be reluctant to sell, because you’ll trigger capital gains taxes. A good choice: low-cost U.S. and international total stock market index funds, which should be tax-efficient—and which shouldn’t ever lag far behind the market averages.”

For those of us in the military, investing in a taxable account comes into play in a few scenarios…

Scenario #1 – You and your spouse (if you have one) have filled your Thrift Savings Plan (TSP) and all other retirement accounts available including IRAs, yet you want to save more for retirement. In this case, you put the rest in a taxable account with the investment company of your choice (Vanguard, Fidelity, Schwab, etc.). This is what I do when all of my retirement accounts are full, and just like Jonathan mentions I invest purely in broad, low-cost index funds at Vanguard. The only taxable holdings I have are the Vanguard U.S. and international total stock market index funds.

Scenario #2 – You are saving for a financial goal that is not related to retirement, such as a downpayment on a home or for a new car. If you’re saving for college, you’d use a 529 plan, but for just about anything else you could use a taxable account. For example, you could put your emergency money and extra spending money in a money market fund among your taxable accounts. The alternative to this is to use a bank and invest in a high-yield savings account (which is what I do), a certificate of deposit (CD), or a money market account. Bankrate.com will show you the best rates for each of these reasonable alternatives.

If you are using a taxable account, there are a few things to consider. If you are investing in bonds, you may want to invest in municipal bonds in your taxable account due to the tax benefits. If you are a fan of target date funds, you may not want to use them in a taxable account because the bond portion will kick off income that is taxed at your full marginal tax rate. This is less of an issue with bond yields being low right now, but most experts feel that bonds are better placed in a tax-advantaged retirement account unless you are using municipal bonds.

The New PFA Has Arrived

Local conditions permitting (as it relates to the COVID-19 pandemic), the Navy will be conducting only one PFA in 2021 (beginning in March 2021). Also of interest, planks will replace curl-ups (sit-ups) and the rowing machine will be an alternative method of performing the cardio portion of the PRT. Please see the NAVADMIN, other supporting documents, and the CNP’s message below for specifics.

From: Nowell, John B Jr VADM USN (USA)

Sent: Wednesday, November 18, 2020 7:18 PM

Subject: PFA Changes: CY 2021 Cycle

Admirals and Senior Leaders,

Earlier today, I released the attached NAVADMIN 304/20 – Physical Readiness Program Policy Changes – CY2021 Cycle, Plank and Rower Modalities. This NAVADMIN announces a single Physical Fitness Assessment cycle in calendar year 2021, beginning 15 March and ending NLT 15 September 2021.

Shifting the PFA cycle to March allows Navy to execute the PFA after the primary influenza season, while also leveraging outdoor venues as the weather warms for the conduct of the test.

Echelon II Commanders may waive the PFA cycle 2021 requirements if COVID-19 conditions prevent commanders from executing safely. It also authorizes the resumption of group physical training (Command/Department/Division PT, FEP) when authorized by the appropriate Echelon II commander. This authority may be delegated to the first flag officer in the chain of command.

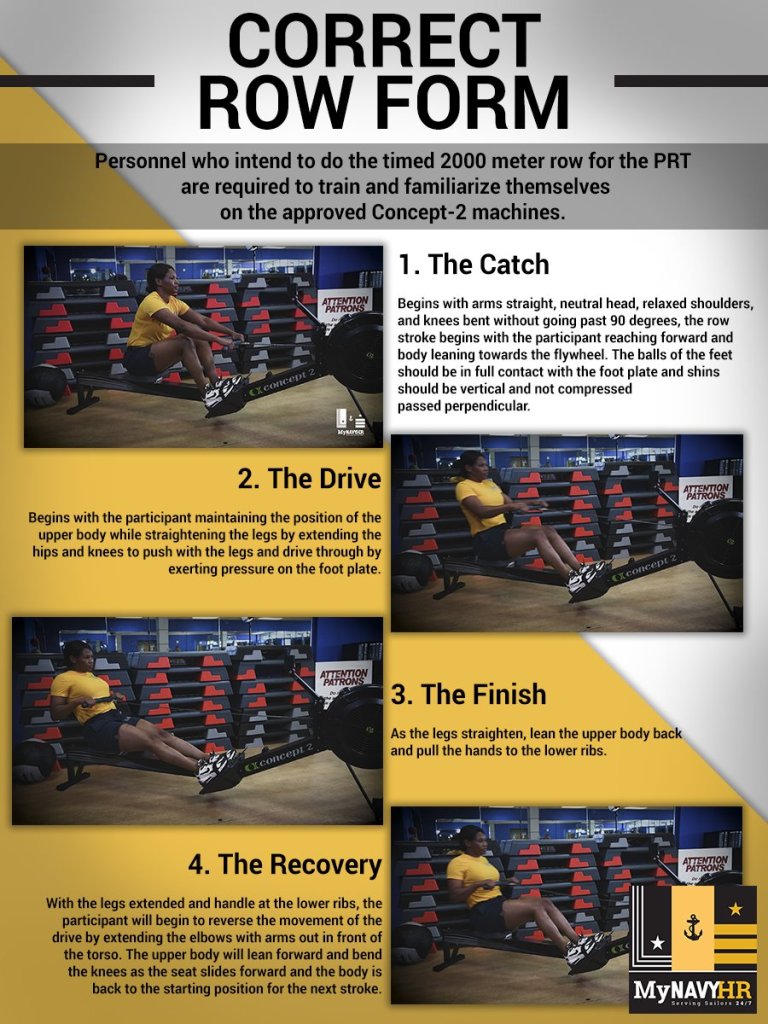

Additionally, as previously announced to the Fleet, this NAVADMIN implements new fitness modalities as part of the Navy Physical Readiness Program. The forearm plank and 2000-meter (m) row are officially incorporated into the Navy Physical Readiness Test (Infographics attached).

The forearm plank has replaced the curl-ups as the abdominal muscular endurance assessment. The forearm plank is a better test of core strength and abdominal muscular endurance. The repeated spinal flexion movement of the curl-up is not operationally relevant, may aggravate low back injuries, and does not strongly challenge the abdominal musculature—also the forearm plank has the additional benefit as being a much safer test amidst a COVID environment. Service Members who do not meet the minimum passing score for the forearm plank modality will not receive a “fail” score for the 2021 cycle PRT only. However, Service Members must still pass the BCA, the push-up and cardio modalities of the PRT.

The 2000-m row on the “Concept-2 Rower” will serve as another alternate cardio option in addition to the 12-min stationary cycle, 500-yd/450-m swim and 1.5-mile treadmill run. The 2000-m row is a non-weight bearing, low impact exercise, which reduces stress on the legs. More importantly, rowing provides a great full-body cardio workout because it engages 80 percent of the body’s musculature. Similar to the stationary cycle, the Concept-2 Rower is space saving and can be used on any naval vessel or installation.

I ask your help in getting the word out to your leadership teams. Standing by for questions or concerns.

V/r, John

VADM John B. Nowell, Jr.

Chief of Naval Personnel (CNP)

Here’s a link to a Navy article:

The Navy’s New Fitness Test is Here – What You Need to Know

Here’s also a Military.com article on the same:

Goodbye Curl-Ups: Navy Releases New PRT Rules for Planks and Rowing

Navy ACHE Regent’s Fellow Accelerator Program

If you are working toward Fellowship in the American College of Healthcare Executives (FACHE), read the message below:

ACHE Superstars,

I’m writing to share with you a fantastic opportunity that will assist all those diligently working towards becoming a credentialed healthcare executive. Brought to you by the Navy RAC’s Advancement, Deckplate Education, & Local Chapter Committee, the Fellow Accelerator Program is scheduled to commence in 2021 (see attached flyer for details):

This program will help drive all potential ACHE Fellow candidates toward:

- Completing an application and achieving all requirements

- Matching candidates with Fellow mentors to complete interviews

- Participating in the Navy’s Virtual Board of Governor’s (BOG) Exam Study Forum for exam preparation

For registration, please contact LCDR Richard Bly. Please spread the word as we start on this marvelous journey of achieving our Navy Medicine goal of increasing advancement to Fellow by 20%!

LCDR Eugene Smith, Jr., MSC, FACHE

ACHE Navy Regent

November Message and Newsletter from ASD(HA)

MHS TEAM:

Every year on November 11, we pause to show our admiration and appreciation to our veterans — both living and deceased — for their bravery, loyalty, and sacrifice. Many veterans walk among us, as colleagues and friends, as partners in bringing world-class health care to our nation’s veterans, service members, and their families. Thank you once again for taking the time to celebrate them and to thank them for their service. November is also Warrior Care Month, a time to contemplate the perseverance and strength of our wounded and injured service members. I met some of these amazing men and women, and the people that care for them, when I visited the Center for the Intrepid in San Antonio. As you know, caring for these service members is a top priority for the DoD. The resources available for our wounded warriors goes far beyond their immediate health needs. From adaptive sports to education and employment resources, there are many ways that we support these wounded, injured, and ill service members.

Our mission requires an array of dedicated men and women at the top of their profession. This month, Dr. David Smith, Deputy Assistant Secretary of Defense for Health Readiness Policy and Oversight, was named Healthcare Government Executive of the Year at the Pinnacle Awards, an annual program that highlights successful executives and businesses saving money and fostering innovation across the DC region. Dr. Smith spearheaded DOD’s change management effort to reform the Military Health System (MHS) developing 11 comprehensive initiatives resulting in sustained improvements in readiness, patient outcomes, and taxpayer savings of over $1 billion in 2019 alone. I would like to give a shout out to the MHS Communications Team for winning two awards at last month’s Public Relations Society of America virtual awards ceremony.

The 2019 Infectious Disease and Summer Safety Campaign called “Bug Week” received the Silver Anvil in the category Events and Observances, and the team also received a runner up Award of Excellence for their content marketing program. The Silver Anvil is recognized as the Oscar in the Public Relations career field. This is the second straight year the MHS has received a Silver Anvil. Congratulations to the entire communications team for this great achievement. As you know, each year on the 4th Thursday in November, Americans take a collective breath to celebrate the blessings of the last year. While 2020 has been a challenging year for all of us, much occurred that reminded us how grateful we should be, especially the dedication of our nation’s health care workers and our MHS colleagues who have passionately supported the nationwide response to COVID-19. As we pause to celebrate on November 26th, I sincerely hope that your table will be filled with loved ones, whether in person or virtually, and filled with gratitude for our many blessings in this trying year.

Finally, please see attached, my November Monthly Newsletter:

Tom

Eliminate Duplication

Jonathan Clements was a longtime personal finance columnist for The Wall Street Journal, and he offers great advice at the best price you can get (free) on his blog Humble Dollar. Here is one piece of advice from his site:

“ELIMINATE DUPLICATION. Many folks have multiple bank and brokerage accounts, multiple funds that invest in the same market sector and even multiple advisors. This can make sense if, say, the goal is to increase FDIC insurance. But often it reflects a naïve notion of diversification—that more accounts somehow mean greater safety. Our advice: Simplify—for your sake and the sake of your heirs.”

I totally agree with this, especially after having to deal with my father in-law’s finances after his recent death. My financial life is relatively simple. We only have our investments in three places – the Thrift Savings Plan (TSP), Vanguard, and Fidelity. The last one is only because my wife’s employer uses Fidelity for their 401k. As soon as the job goes, so will that account as I roll it into the TSP or a Vanguard account.

Yes, you can rollover money from other retirement accounts into the TSP. Even if you get out of the military, keep the TSP and use it to rollover accounts. You won’t find a lower cost option anywhere.

To me, you only need to use one investment company in addition to the TSP. While Vanguard is my choice and what I recommend, there are certainly others. Just make sure that you keep an eye on your investment costs. If you use Vanguard, you know they’ll be among the lowest cost investments no matter what you pick. While some investment companies have index funds that are even lower in cost than Vanguard’s, their other funds are probably more expensive than the similar investment at Vanguard.

DSS Position at NMRTC Camp Pendleton

NMRTC Camp Pendleton is looking for the next Director of Surgical Services. Please see the announcement and PD below. Individuals applying need PERS/Detailer clearance.

Finance Friday Post

Here are this week’s articles:

- Check out the most underused veterans benefits in your state

- Don’t Mix Insurance and Investing

- How to Open a Brokerage Account

- How to Save for a Big Purchase

- Private Real Estate Lending Funds

- Should Index Fund Investors Care About Tesla Getting Added to the S&P 500?

- What’s the right emergency fund amount?

November Sailor 2 Sailor Newsletter

This newsletter has some pertinent info discussing ROM not being chargeable as leave as well as procedures if you or a family member test positive for COVID during a PCS:

Thowback Thursday Classic Post – TSP Fund Deep Dive – The F Fund

There are only five investments available in the Thrift Savings Plan (TSP), so let’s take a detailed look at them one at a time. In this post we’ll cover the F Fund.

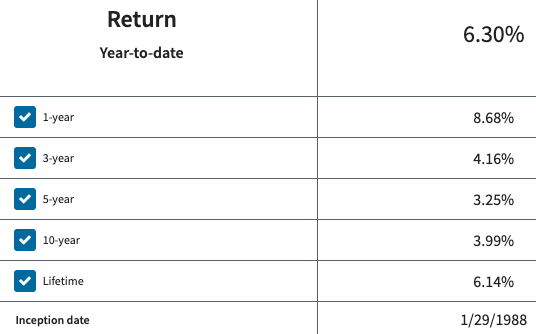

Inception Date

29 JAN 1988

Fund Management

The Federal Retirement Thrift Investment Board currently contracts BlackRock Institutional Trust Company, N.A. (BlackRock) to manage the F Fund assets. The F Fund remains invested regardless of the performance of the securities markets or the overall economy.

Investment Strategy

The F Fund is invested in a bond index fund that invests in government, corporate, and mortgage-backed bonds. The F Fund’s objective is to match the performance of the Bloomberg Barclays U.S. Aggregate Bond Index.

The F Fund is a passively managed fund that remains invested according to its indexed investment strategy regardless of securities market movements or general economic conditions.

What is the Risk?

Your investment in the F Fund is subject to market risk, credit risk, prepayment risk, and inflation risk.

Because the F Fund returns move up and down with the returns in the bond market, your F Fund investment is subject to market risk. For example, when interest rates rise, bond prices (and thus, the returns of the index and the F Fund) fall. Conversely, in an environment of falling interest rates, bond prices, as well as the index and F Fund returns, rise.

As an F Fund investor, you are also exposed to credit (default) risk, or the possibility that principal and interest payments on the bonds that comprise the index will not be paid.

The F Fund is subject to inflation risk, meaning your F Fund investment may not grow enough to offset the reduction in purchasing power that results from inflation.

Your F Fund investment is also exposed to prepayment risk, which is the probability that if interest rates fall, bonds that are represented in the index will be paid back early thus forcing lenders to reinvest at lower rates.

What is the Benefit?

Although there are several types of risks associated with the F Fund, the overall risk is relatively low in comparison to certain other fixed income investments in the market because the F Fund includes only investment-grade securities. As a result, F Fund investors are rewarded with the opportunity to earn higher rates of return over the long term than they would from investments in short-term securities such as the G Fund. Here is all the performance data as of 14 NOV 2020:

Types of Earnings

The F Fund changes in value as the market price of its bond holdings change. In addition, the F Fund makes money for its investors with capital gains (net of trading costs), interest on notes and bonds, interest on short-term investments, and securities lending income.

BlackRock credits interest income each business day. This income is then reflected in the TSP share prices.

Share Price Calculations

The value of your account is determined each business day based on the daily share price and the number of shares you hold. At the end of each business day, after the stock and bond markets have closed, the total value of the funds’ holdings (net of accrued administrative expenses) is divided by the total number of shares outstanding to determine the share price for that day. The daily change in TSP share prices reflects all investment income (interest on short-term investments, dividends, capital gains or losses, and securities lending income) net of TSP administrative expenses.

Expenses

The net expenses paid by investors is 0.042% or 4.2 basis points, which like all the TSP funds is ridiculously low and is a major benefit of the TSP. It cost $0.42 for each $1,000 invested.

How Should I Use the F Fund in my TSP Account?

In periods of falling interest rates, the F Fund will experience gains from the resulting rise in bond prices. So in the long run, you may expect F Fund returns to exceed those of the G Fund; however, you should also expect greater price volatility (up and down movements).

It is also important to know that higher returns are not guaranteed. This is because losses may occur when interest rates are rising, causing bond prices to fall.

The F Fund can be useful in a portfolio that also contains stocks funds. This is because the prices of bonds and stocks don’t always move in the same direction or by the same amount at the same time. So a retirement portfolio that contains stock funds, like the C, S, and I Funds, along with the F Fund, will tend to be less volatile than one that contains stock funds alone.

Advice from My Favorite Short Investing Book

Here is what my favorite investing book, The Elements of Investing: Easy Lessons for Every Investor, says about investment-grade bond index funds like the F Fund:

If indexing has advantages in the stock market, its superiority is even greater in the bond market. You would never want to hold just one bond (such as an IOU from General Motors or Chrysler) in your portfolio – any single bond issuer could get into financial deficiency and be unable to repay you in full. That’s why you need a broadly diversified portfolio of bonds – making a mutual fund essential. And it’s wise to use bond index funds: They have regularly proved superior to actively managed bond funds.

They also say, “Well-diversified portfolios should have holdings of bonds as well as stocks.”

If you want to know how to integrate the F fund into your own TSP investments, read the Crush the TSP series. In particular, step 3 tells you how to figure out how much of your portfolio to devote toward bonds.