Playing the Game and Managing Your Military Career

What better to do during a global pandemic than listen to a screencast about managing your career! Here are the PPT slides I used for it:

Playing the Game – Managing Your Military Career

More Stringent DoD Travel Restrictions Released Stopping All Domestic Travel

Below is the text from this original DoD article/release dated 13 MAR 2020. FAQs are here as well.

Today, the Deputy Secretary of Defense David L. Norquist approved new travel restrictions for service members, DoD civilians, and their families assigned to DoD installations, facilities and surrounding areas within the United States and its territories. This restriction will halt all domestic travel, including Permanent Change of Station, and Temporary Duty. This restriction will also pause civilian hiring at DoD installations and components for persons who do not reside within the hiring entity’s local commuting area.

Additionally, service members will be authorized local leave only, following Service guidelines. This new guidance is effective March 16 and continues through May 11.

Similar to other travel guidance regarding COVID-19, travel exceptions may be granted for compelling cases where the travel is mission-essential, for humanitarian reasons, or warranted due to extreme hardship. Approval authority for these exceptions belongs to the Combatant Commander, the Service Secretaries, the Chief Management Officer, or the Director of the Joint Staff, but may be delegated.

The Department will continue to issue additional guidance with regard to the COVID-19 as conditions warrant. Our goal is to remain ahead of the virus spread so our military force remains effective and ready.

For more information on the CDC travel restrictions, visit https://wwwnc.cdc.gov/travel/notices/.

We encourage all DOD personnel to visit https://www.defense.gov/Explore/Spotlight/Coronavirus/for information on staying healthy during the outbreak. The Department will issue follow-on guidance on this directive prior to implementation.

What is an Active Duty Credit Alert?

One option that military personnel have to protect their credit is to use an active duty alert. What exactly is an active duty alert?

A 12 month active duty alert is available if you are active duty in the US military. In addition to the normal fraud alert that civilians can use, your name is removed from prescreened credit or insurance offers you get in the mail for 2 years. It is designed to protect your credit while you are deployed, but you don’t have to be deployed to use it. We have this placed on our credit on a continuous basis to prevent fraud.

It forces businesses to take reasonable steps to verify your identity before issuing credit in your name. If you provide a telephone number when you place the alert, a business must either contact you at the telephone number you provided or take other reasonable steps to verify your identity. This helps them confirm that the credit application is really from you and not from someone who has stolen your identity. If you actually are deployed and are difficult to reach, you can assign a personal representative to answer for you, place, or remove the alert.

You can end the alert before 12 months, or request another one when the initial one expires.

You can place a fraud alert or active duty alert by visiting any one of the three nationwide credit reporting agencies – Equifax , Experian , or TransUnion. The one that you contact must notify the other two. You also can find links to their websites at IdentityTheft.gov/CreditBureauContacts.

COVID-19 NAVADMIN That Discusses PCS and Travel

Below is the recently released NAVADMIN. Again, it is long, but if you are PCSing, traveling, have board exams coming up, want to go to a conference, etc. I’d take the time to read the relevant parts:

UNCLASSIFIED//

PRIORITY

P 122210Z MAR 20 MID510001053027U

FM CNO WASHINGTON DC

TO NAVADMIN

INFO SECNAV WASHINGTON DC

CNO WASHINGTON DC

BT

UNCLAS

NAVADMIN 064/20

MSGID/NAVADMIN/CNO WASHINGTON DC/CNO/MAR//

SUBJ/NAVY MITIGATION MEASURES IN RESPONSE TO CORONAVIRUS OUTBREAK//

REF/A/OPLAN/NORTHCOM/DOD GCP-PI&ID-3551-13/15OCT13//

REF/B/INST/DODI 6200.03/28MAR19//

REF/C/MEMO/OSD/30JAN2020//

REF/D/EXORD/JOINT STAFF J3/012240ZFEB20//

REF/E/MEMO/OSD/07FEB2020//

REF/F/MEMO/OSD/25FEB2020//

REF/G/NAVADMIN/OPNAV/071613ZFEB20//

REF/H/NAVADMIN/OPNAV/112054ZFEB20//

REF/I/NAVADMIN/OPNAV/051456ZMAR20//

REF/J/GENADMIN/JOINT STAFF/051908ZMAR20//

REF/K/MEMO/JOINT STAFF/06MAR2020//

REF/L/MEMO/OSD/10MAR2020//

REF/M/MEMO/OSD/11MAR2020//

REF/N/ALNAV/SECNAV/025-20//

REF/O/MEMO/OSD/11MAR2020//

NARR/REF A IS DEPARTMENT OF DEFENSE (DOD) GLOBAL CAMPAIGN PLAN FOR PANDEMIC

INFLUENZA AND INFECTIOUS DISEASE.

REF B IS DODI 6200.03, PUBLIC HEALTH

EMERGENCY MANAGEMENT WITHIN THE DOD.

REF C IS MEMO FROM UNDER SECRETARY OF DEFENSE FOR PERSONNEL AND READINESS

PROVIDING FORCE HEALTH PROTECTION GUIDANCE FOR PERSONNEL RETURNING FROM CHINA

DURING THE NOVEL CORONAVIRUS (COVID-19) OUTBREAK.

REF D IS SECDEF-APPROVED EXORD THAT DIRECTS USNORTHCOM TO EXECUTE ITS

PANDEMIC PLAN 3551-13 AND SUPPORTING GEOGRAPHIC COMBATANT

COMMANDERS TO EXECUTE THEIR PANDEMIC PLANS IN RESPONSE TO THE NCOV (COVID-19)

OUTBREAK.

REF E IS SUPPLEMENT 1 TO REF C.

REF F IS SUPPLEMENT 2 TO REF C.

REF G IS NAVADMIN 033/20, OPNAV REPORTING GUIDANCE SUPPORTING DOD RESPONSE TO

THE COVID-19 OUTBREAK.

REF H IS NAVADMIN 039/20, UPDATED DOD GUIDANCE FOR MONITORING PERSONNEL

RETURNING FROM CHINA DURING THE NOVEL CORONAVIRUS OUTBREAK.

REF I IS NAVADMIN 058/20, UPDATED NAVY GUIDANCE DURING THE NOVEL CORONAVIRUS

OUTBREAK. REF J IS JOINT STAFF MESSAGE FOR DOD COVID-19 PASSENGER

SCREENINGGUIDELINES FOR OVERSEAS MILITARY TRANSPORTATION TERMINALS.

REF K IS JOINT STAFF FORCE HEALTH PROTECTION GUIDANCE TO MITIGATE THE RISK OF

COVID-19 TRANSMISSION.

REF L IS MEMO FROM UNDER SECRETARY OF DEFENSE FOR PERSONNEL AND READINESS

PROVIDING FORCE HEALTH PROTECTION GUIDANCE FOR THE USE OF PERSONAL PROTECTIVE

EQUIPMENT AND NON-PHARMACEUTICAL INTERVENTIONS DURING THE CORONAVIRUS DISEASE

2019 OUTBREAK.

REF M IS MEMO FROM UNDER SECRETARY OF DEFENSE FOR PERSONNEL AND READINESS

PROVIDING FORCE HEALTH PROTECTION GUIDANCE FOR PERSONNEL TRAVELING DURING THE

NOVEL CORONAVIRUS OUTBREAK.

REF N IS ALNAV 025/20, FORCE HEALTH PROTECTION GUIDANCE FOR THE DEPARTMENT OF

NAVY.

REF O IS MEMO FROM SECRETARY OF DEFENSE FOR TRAVEL RESTRICTIONS FOR DOD

COMPONENTS IN RESPONSE TO CORONAVIRUS DISEASE.//

POC/RADM KARL THOMAS/OPNAV N3N5B/703-692-9291/KARL.O.THOMAS1(AT)NAVY.MIL/

RADM JEFFREY JABLON/OPNAV N13/703-604-5040/JEFFREY.JABLON(AT)NAVY.MIL/

RADM GAYLE SHAFFER/OPNAV N093B/703-697-7399/GAYLE.SHAFFER(AT)MED.NAVY.MIL//

RMKS/1. This NAVADMIN announces further measures to mitigate the spread of

COVID-19 throughout the Navy enterprise and amplifies DoD and DON references

(o) and (n) guidance for Navy military members. It summarizes and repeats

applicable guidance where appropriate so that this will serve as a one-stop

information source.

1.A. Background. The DoD has transitioned to Phase Two Mitigation of

reference (a), the global campaign in response to the COVID-19 outbreak. The

U.S. Centers for Disease Control and Prevention (CDC) is now reporting over

100,000 cases worldwide, to include cases in the U.S. During the COVID-19

outbreak, the DoD and Navy will continue to protect and preserve the

operational effectiveness of forces worldwide in accordance with (IAW)

references (a) and (b). Utilizing force health protection guidance (FHPG)

from the Under Secretary of Defense for Personnel and Readiness (USD (P&R))

provided in reference (c) and (m), USNORTHCOM is executing its pandemic plan

and geographic combatant commanders are executing their supporting pandemic

plans IAW reference (d). In compliance with updated USD (P&R) FHPG issued in

references (e) and (f), Office of Chief Naval Operations (OPNAV) published

initial reporting guidance supporting DoD response to the COVID-19 outbreak

in reference (g) and updated that guidance in references (h) and (i).

1.B. Role of the CDC. As the leading U.S. government Public Health

Agency, the CDC continues to assess the risk of COVID-19 and to provide

guidance for those residing in the U.S. and traveling abroad. Because CDC

guidance is principally tailored for persons residing in the continental U.S.

(CONUS), some CDC COVID-19 guidance may have limited applicability for

commanders, particularly those outside the United States, and is not

recognized by other sovereign nations. While DoD continues to follow the

lead of the CDC, when needed, additional military specific measures are

authorized to mitigate risk to U.S. forces stationed or deployed around the

world, and to protect Service Members, DoD civilian employees, and their

family members. USD (P&R) FHPG issued in reference (m) provides guidance for

DoD personnel traveling during the novel coronavirus outbreak.

1.C. CDC Travel Health Advisories. The CDC provides travel health

advisories at https://www.cdc.gov/coronavirus/2019-ncov/travelers/index.html.

The levels of advisories are noted below and will be referenced in this

NAVADMIN (note that CDC warning levels DO NOT apply to

CONUS):

Level 1 Watch, practice usual precautions (risk of limited community

transmission)

Level 2 Alert, practice enhanced precautions (sustained (ongoing) community

transmission)

Level 3 Warning, avoid nonessential travel (widespread sustained (ongoing)

transmission)

1.D. Department of the Navy (DON) Civilian Guidance. The DON civilian

workforce more than 220,000 strong plays an integral role in supporting our

Sailors and building, manning and maintaining our ships and submarines.

Working shoulder to shoulder with our military members, it is imperative to

have alignment between DON civilian and military COVID-19 policy and

guidance. To avoid any ambiguity, DON civilian guidance is contained in

reference (n).

1.E. Military Health Protection Guidance. The Secretary of Defense

(SECDEF) has provided explicit Force Health Protection Guidance in both

references (c) and (m) which is more restrictive than CDC guidance.

Commanders must read both documents in their entirety and ensure they are

following the Service Member actions spelled out in this guidance. Local

Commanders can be more restrictive based on Command location, local community

transmission, risk to mission and risk to force. Each and every Sailor must

ensure they proactively manage and minimize their personal risk to exposure,

and that of their families. Commands are charged with ensuring they track

and monitor each Sailor and aggressively follow SECDEF guidance in these

references.

2. Mission. All commands will take specific actions to mitigate the spread

of COVID-19 worldwide and adhere to the policies and reporting requirements

contained in this NAVADMIN.

3. Policy. In order to maintain force health protection, readiness of the

force and mitigate the risk of transmission among personnel, the Secretary of

Defense directed a stop movement to affected countries and areas effective 13

Mar 2020 in reference (o). This includes all forms of travel to include

Permanent Change of Station, Temporary Duty and leave. This order will

remain in effect until 13 May 2020, 60 days after implementation:

3.A. Permanent Change of Station (PCS). Service Members and dependents

under OCONUS PCS orders to locations designated CDC COVID-19 Warning Level 3

or CDC COVID-19 Alert Level 2 will follow the guidance in section 3.A. of

this NAVADMIN. Note that CDC warning levels DO NOT apply to CONUS. CONUS

PCS moves may continue for now, UNODIR.

3.A.1. PCS orders to or from CDC COVID-19 Warning Level 3

locations. Service Members and their dependents under PCS orders to or from

a CDC COVID-19 Warning Level 3 location will stop movement. This policy

applies to currently designated CDC COVID-19 Warning Level 3 locations, or

those designated Level 3 at a later date.

3.A.1.a. Service Members who have detached from their

parent command prior to the date of this NAVADMIN and are in transit are

directed to contact Navy Personnel Command (NPC) for follow-on guidance per

paragraph 5.A. NPC is standing by to address each specific case and will

authorize entitlements based on current location and situation.

3.A.1.b. Detaching and gaining commands shall make every

effort to contact affected Service Members enroute to/from their command to

advise them of the contents of this message.

3.A.2. PCS orders to CDC COVID-19 Alert Level 2 locations.

Service Members under PCS orders to a CDC COVID-19 Alert Level 2 location

will execute orders. Dependents of Service Members executing accompanied PCS

orders to a CDC COVID-19 Alert Level 2 location will delay travel to the CDC

COVID-19 Alert Level 2 location until 13 May 2020, 60 days after

implementation. This policy applies to currently designated CDC Alert

Level 2 locations and those designated at a later date. For Service Members

with dependents, non-concurrent dependent travel entitlements will vary

depending on each case. NPC is standing by to address each specific case and

authorized entitlements based on current location and situation.

3.B. Other Official Travel (Meetings, Conferences, Site Visits, etc).

3.B.1. All other official travel by Service Members to or from a

country designated as CDC COVID-19 Warning Level 3, will require an exception

IAW paragraph 3.E. All other official travel by Service Members, including

within CONUS, is strongly discouraged. If required, official travel must be

determined to be mission essential and will be approved by the first flag

officer or senior executive service member (SES) in the chain of command of

the traveler.

3.B.2. All OCONUS travel, other than those countries designated as

CDC COVID-19 Warning Level 3, for Selected Reserve personnel conducting

annual training or other duty shall be IAW Geographic Combatant Commander

(CCDR) or Navy Component Commander COVID-19 policy. Selected Reserve travel

to a CDC COVID-19 Warning Level 3 location shall be in accordance with this

NAVADMIN.

3.C. Travel for Official Training.

3.C.1. Service Members or initial accessions travel from an OCONUS

CDC COVID-19 Alert Level 2 location to attend formal training in CONUS must

be determined to be mission essential and will be approved by the first flag

officer or SES in the chain of command of the traveler, require advance

coordination with the training command and will comply with Navy Component

Commander guidance concerning pre- and post- travel medical screening and

reception procedures to include restriction of movement (ROM).

3.C.2. Service Members or initial accessions traveling from an

OCONUS CDC COVID-19 Warning Level 3 location to attend formal training in

CONUS require an exception as outlined in paragraph 3.E. and will coordinate

with the training command prior to approval.

3.C.3. Service Members currently in training who are from a CDC

COVID-19 Alert Level 2 or higher location are authorized to complete training

and return to their parent command.

3.D. Personal Leave and Liberty. Commanders and commanding officers

shall carefully review OCONUS/CONUS leave and liberty plans to minimize

personnel traveling to locations that have declared a public health

emergency, even within CONUS. These decisions should be based on local

community transmission, risk to mission and risk to force, as well as

personal hardship or family concerns of the individual. Approval authority

for leave requests to areas for which a travel advisory has been issued by

the CDC for countries other than COVID-19 Warning Level 3, is the first flag

officer or SES in the chain of command. Leave or personal travel to a COVID-

19 Warning Level 3 Country requires a waiver as outlined in paragraph 3.E.

3.E. Exceptions.

3.E.1. Individuals pending retirement or separation within the

next 60 days are exempt from this stop movement.

3.E.2. Commanding officers and officers in charge may request an

exception to paragraphs 3.A. through 3.D. in the following cases: (1)

determined to be mission essential, (2) necessary for humanitarian reasons,

or (3) warranted due to extreme hardship. Mission-essential travel refers to

work that must be performed to ensure the continued operations of mission

essential functions, as determined by the local Commander.

3.E.2.a. Navy Personnel Command (PERS-4) is authorized to

approve or deny stop movement exceptions for PCS travel in paragraphs 3.A.

and 3.C. Approvals of exception requests shall be made via message traffic

to all concerned and will specify whether dependents are authorized to

accompany the Service Member. OCONUS Commanders endorsement is required.

Upon receipt of an approved exception, Transaction Service Center or

Personnel Support Detachment/personnel offices will process the Service

Member for transfer to the gaining command. Send all exception requests to

pers451(at)navy.mil with the subject line PCS EXCEPTION REQUEST. Exception

request formats will be provided by PERS-4 and posted on MyNavy

Portal. Service Members who are granted an exception and are traveling from

a CDC COVID-19 Warning Level 3 or Alert Level 2 location will receive

guidance from NPC concerning Navy Component Commander pre- and post-travel

medical screening and reception procedures to include ROM.

3.E.2.b. The first flag officer or SES in the chain of

command is authorized to approve or deny stop movement exceptions for

official travel in paragraph 3.B., and for official training, not associated

with a PCS, in paragraph 3.C. and for leave in paragraph 3.D. Service

members who are granted an exception and are traveling from a CDC COVID-19

Warning Level 3 or Alert Level 2 location will comply with Navy Component

Commander guidance concerning pre- and post- travel medical screening and

reception procedures to include ROM.

3.F. Actions upon return from a CDC COVID-19 Alert Level 2 or higher

location or if in close contact with a confirmed COVID-19 infection.

3.F.1. Service Members who travel or have traveled in the prior 14

days to or through a CDC COVID-19 Warning Level 3 or Alert Level 2 location

will immediately notify their chain of command and be placed in a 14 day ROM

status. Immediate supervisors will not require Service Members to report to

their duty location or otherwise disregard the ROM. Service Members will

comply with reference (m) and Navy Component Commander guidance concerning

pre- and post-travel medical screening and reception procedures to include

ROM. Commanders may, pursuant to DoD and Navy regulations and policies,

authorize telework opportunities, permissive TAD/TDY or work from home as

necessary.

3.F.2. Service Members who have had close contact with someone

with a confirmed COVID-19 infection and feel sick with a fever, cough or

difficulty breathing shall:

3.F.2.a. Inform their Senior Medical Department

Representative immediately.

3.F.2.b. Seek medical care immediately. Before going to

the office of a doctor or emergency room, call ahead to provide recent travel

locations and symptoms.

3.F.2.c. Avoid contact with others.

3.F.2.d. Stay home except to get medical care.

3.F.2.e. Cover mouth and nose with tissue or sleeve (not

hands) when coughing or sneezing.

3.G. Conferences. All Navy personnel shall maximize the conduct of

virtual conferences, meetings and classes to the fullest extent. Holding

conferences are discouraged and must be approved by a Navy Component

Commander, Deputy Fleet Commander, Task Force Commander or Navy Region

Commander charged with hosting the conference.

3.H. General Health Guidance. Compliance with CDC guidance is critical

to minimize the spread of COVID-19. All personnel shall:

3.H.1. Wash hands often with soap and water for at least 20

seconds, especially after going to the bathroom, before eating, and after

blowing your nose, coughing or sneezing. If soap and water are not readily

available, use an alcohol-based hand sanitizer with at least 60 percent

alcohol. Always wash hands with soap and water if hands are visibly dirty.

3.H.2. Avoid close contact with people who are sick.

3.H.3. Avoid touching your eyes, nose and mouth.

3.H.4. Stay home when you are sick.

3.H.5. Cover your cough or sneeze with a tissue, then throw the

tissue in the trash.

3.H.6. Clean and disinfect frequently touched objects and surfaces

using a regular household cleaning spray or wipe.

3.H.7. Maximize open doors within area with equivalent

classification levels.

3.H.8. Minimize meetings of more than five persons.

3.H.9. Practice social distancing.

3.H.10. Minimize attendance at large group gatherings outside of

the workplace (for example concerts and sporting events with large

attendance).

3.I. Supplemental Guidance for Commanders.

3.I.1. IAW reference (m), Commanders should identify and track all

Service Members who travel or have a history of travel in the prior 14 days

to, through or from a CDC COVID-19 Alert Level 2 or Warning Level 3 OCONUS

location. This includes travel by military or commercial means as well as

private conveyance and includes all forms of travel to include PCS, temporary

duty and leave. Commanders shall ensure Service Members implement the

following actions for the next 14 days:

3.I.1.a. Implement self-observation, i.e., take

temperature twice a day and remain alert for fever (>100.4 degrees F or 38

degrees C) and remain alert for fever, cough or difficulty breathing.

3.I.1.b. To the extent possible implement social

distancing, i.e., remain out of congregate settings, avoid mass gatherings

and maintain 6 feet or 2 meter distance from others when possible.

3.I.1.c. If individuals feel feverish or develop measured

fever, cough or difficulty breathing, immediately self-isolate, limit contact

with others and seek advice by telephone from the appropriate healthcare

provider to determine whether medical evaluation is required.

3.I.2. Commanders will adhere to DoD guidance for personnel

traveling during the novel coronavirus outbreak per reference (m) to include

COVID-19 screening at overseas military transportation terminals per

reference

(j). Commanders will review the supplemental risk-based measures

and observe the operational risk level mitigation actions for COVID-19

outlined in reference (b).

3.I.3. For individuals traveling OCONUS to OCONUS, Commanders will

ensure travel is mission essential and follow the guidance listing in

reference (o) if compelling exceptions are necessary. Military air crew are

exempt from the requirements in this NAVADMIN, but will ensure they actively

practice social distancing and prudent measures to mitigate potential contact

and COVID-19 transmission.

3.I.4. Commanders will comply with status of forces agreements

when applicable.

3.I.5. Consider measures to place mission essential shore staffs

on alternating day or port/starboard work rotations.

3.I.6. Use maximum latitude to authorize telework, liberal leave,

permissive TDY as necessary to minimize spread within your teams.

3.I.7. Implement social distancing techniques for any meetings you

conduct.

4. Regular Reporting. For CONUS commands, ensure your point of contacts

submit accurate and timely COVID-19 daily reports and CCIRs to USFFC for

consolidation and subsequent reporting to OPNAV. For OCONUS commands, ensure

your POCs submit accurate and timely COVID-19 daily reports and CCIRs to

Fleet Commanders for consolidation and subsequent reporting to OPNAV. Navy

commands will report the following CCIRs immediately through their chain of

command and via OPREP where appropriate:

4.A. Any confirmed cases of COVID-19 among Navy Service Members, DoD

civilians, or military family members. In addition, a report should be made

if a command learns of a confirmed case with an assigned contractor,

4.B. The death of a Navy Service Member, DoD civilian, Navy contractor

or family member due to COVID-19,

4.C. Any shortage of medical personal protective equipment (PPE) or test

kits,

4.D. Installation or facility closures,

4.E. Installation or facility is unable to meet isolation requirements,

4.F. Any change to health protection condition (HPCON).

5. Points of Contact.

5.A. Sailor Support. Service Members with questions regarding this stop

movement or entitlements for PCS travel should contact the MyNavy Career

Center (1-833-330-6622) or email ASKMNCC(AT)NAVY.MIL. Detailers are ready to

support all order modifications and commands should work with their placement

officers.

5.B. Medical Questions. BUMED Watch: 703-681-1087/1125 or NIPR

EMAIL: usn.ncr.bumedfchva.list.bumed---2019-ncov-response-cell@mail.mil.

5.C. Reporting Requirements. OPNAV Battle Watch Captain at

703-692-9284.

6. The Navy will ensure the best possible Navy-wide Force Health Protection

for its Sailors, civilian employees and family members. However, all members

of the Navy family must do their part by adhering to CDC guidelines as they

relate to basic hygiene and human interaction. The Navy will remain focused

on meeting our global commitments while also ensuring the health and well-

being of our Service Members, Navy civilians and our families.

7. Released by ADM R. P. Burke, Vice Chief of Naval Operations.//

BT

#0001

NNNN

UNCLASSIFIED//

Finance Friday Articles

Here are my favorites:

3 Reasons Why You Should Invest in Bonds

Can You Handle 100% of Your Money in Stocks During a Correction?

Four Opportunities Due to Coronavirus

Here are the rest of the articles:

3 tips for trading in volatile markets

20 Things You Need to Know About Asset Protection

All-Equity ETF Portfolio Doesn’t Add Up

Asset Allocation (Part 3): What’s in My Dream Bucket?

Bearing Up – 4 Lessons from Previous Bear Markets

Buying a $3 Million Umbrella Insurance Policy for $170 Per Year

Creating an Overreaction Plan for the Coronavirus

How the Coronavirus is Impacting Commercial Real Estate

It’s time to change the retirement planning conversation

Making the best of a market downturn

Partner, Parent, or Physician? A False Dilemma

Should We Buy Our Dream House?

The Best Cities To Buy Real Estate In America

The One Guarantee in the Stock Market

The Potential Impact of Coronavirus on Private Real Estate Investments

The Relationship Between Recessions and Market Crashes

Why Does The Stock Market Go Up Over Time?

Why Hospital Administrators Should Eat Last

Why I’m More Worried About the Bond Market Than the Stock Market

Why I Still Work (Even Though My Physician Husband Out-Earns Me)

Why One Mother Left Her GI Fellowship to Raise a Family

ALNAV Dictating Restrictions Due to COVID-19

The ALNAV came out and is pasted below. I’d summarize, but you should probably just read it.

I know…I know…you’re allergic to reading an ALNAV. Take some Benadryl and Prednisone and read it! (Or you can read this Military Times article or the SECDEF memo.)

Especially if you are PCSing or are (were?) traveling anytime soon.

UNCLASSIFIED//

ROUTINE

R 121914Z MAR 20 MID110000460428U

FM SECNAV WASHINGTON DC

TO ALNAV

INFO SECNAV WASHINGTON DC

CNO WASHINGTON DC

CMC WASHINGTON DC

BT

UNCLAS

ALNAV 025/20

MSGID/GENADMIN/SECNAV WASHINGTON DC/-/MAR//

SUBJ/VECTOR 15 FORCE HEALTH PROTECTION GUIDANCE FOR DEPARTMENT OF THE NAVY//

REF/A/MEMO/OSD/30JAN20//

REF/B/MEMO/OSD/07FEB20//

REF/C/MEMO/OSD/25FEB20//

REF/D/MEMO/OSD/11MAR20//

REF/E/MEMO/OSD/11MAR20//

REF/F/MEMO/JCS/06MAR20//

REF/G/GENADMIN/JCS/04FEB20//

REF/H/MEMO/OPM/03MAR20//

REF/I/NAVADMIN/OPNAV/033-20//

REF/J/NAVADMIN/OPNAV/058-20//

REF/K/NAVADMIN/OPNAV/039-20//

REF/L/MARADMIN/082-20//

REF/M/MARADMIN/150-20//

NARR/REF A IS MEMO FROM UNDERSECRETARY OF DEFENSE FOR PERSONNEL AND READINESS

PROVIDING FORCE HEALTH PROTECTION GUIDANCE FOR PERSONNEL RETURNING FROM CHINA

DURING THE CORONAVIRUS DISEASE 2019 (COVID-19) OUTBREAK. REF B IS SUPPLEMENT

1 TO REF A. REF C IS SUPPLEMENT 2 TO REF A. REF D IS SUPPLEMENT 4 TO REF A

AND REF E. REF E IS MEMO FROM SECRETARY OF DEFENSE (SECDEF) PROVIDING

GUIDANCE TO TRAVEL RESTRICTIONS FOR DEPARTMENT OF DEFENSE (DOD) COMPONENTS IN

RESPONSE TO COVID-19. REF F IS A MEMO FROM DIRECTOR OF JOINT STAFF TO JOINT

STAFF PERSONNEL. REF G IS THE JOINT STAFF GENERAL ADMIN ON THE COVID-19.

REF H IS THE OFFICE OF PERSONNEL MANAGEMENT (OPM) PRELIMINARY GUIDANCE TO

AGENCIES DURING COVID-19. REF I IS NAVADMIN 033/20, WHICH IS THE OPNAV

REPORTING GUIDANCE SUPPORTING DOD RESPONSE TO COVID-19 OUTBREAK. REF J IS

NAVADMIN 058/20 IS AN UPDATED NAVY GUIDANCE DURING THE COVID-19 OUTBREAK.

REF K IS NAVADMIN 039/20 AN UPDATED DOD GUIDANCE FOR MONITORING PERSONNEL

RETURNING FROM CHINA DURING THE COVID-19 OUTBREAK. REF L IS MARADMIN 082/20

THE U.S. MARINE CORPS DISEASE CONTAINMENT PREPAREDNESS PLANNING GUIDANCE FOR

COVID-19. REF M IS MARADMIN 150/20 THE U.S. MARINE CORPS DISEASE CONTAINMENT

PREPAREDNESS PLANNING GUIDANCE FOR COVID-19; COMMANDERS RISK-BASED MEASURED

RESPONSES.

RMKS/1. This ALNAV provides guidance to Department of the Navy (DON)

personnel and commands on the COVID-19 outbreak and is subject to additional

guidance provided by the SECDEF. Anticipate modifications to this policy

over the next several weeks as more information becomes available. The

COVID-19 outbreak continues, with the Centers for Disease Control and

Prevention (CDC) reporting over 100,000 cases worldwide, to include over

1,000 cases in the United States.

2. Effective 13 March 2020, all DON personnel, including, active, reserve,

civilian, and foreign military under DON authority, shall comply with this

guidance to mitigate the risk of further transmission of COVID-19. Our

priority is to ensure the welfare and safety of DON personnel and their

families, and to ensure mission readiness and success.

3. Individual and Workplace Preventative Measures. During the COVID-19

outbreak, the DoD will continue to protect and preserve the operational

effectiveness of forces worldwide in accordance with utilizing Force Health

Protection Guidance (FHPG) from the Undersecretary of Defense for Personnel

and Readiness provided in references (a) through (e), FHPG for the Joint

Staff references (f) and (g), and preliminary Office of Personnel Management

(OPM) guidance to agencies during COVID-19 reference (h).

In accordance with references (a) and (d), the following guidelines will help

minimize the spread of COVID-19:

a. Appropriately wash hands with soap and water for at least 20 seconds.

If soap and water are unavailable, use an alcohol-based hand sanitizer that

contains at least 60 percent alcohol.

b. Avoid touching eyes, nose, and mouth.

c. Avoid close contact with those who are sick.

d. Cover your cough or sneeze with a tissue or sleeve.

e. Clean and disinfect frequently touched objects and surfaces using an

appropriate disinfectant cleaning solution.

f. Minimize large group meetings or gatherings and implement social

distancing, by maintaining six feet or two meter distance from others when

possible.

g. Personnel who have symptoms of acute respiratory illness shall remain

home until they are free of fever (100.4of or 37.8oc or greater using an oral

thermometer) without the use of medication.

h. Personnel who arrive at work and appear to have acute respiratory

illness symptoms will be separated from other employees and sent home. DON

military and civilian employees should be placed on sick leave or annual

leave or if able, allowed to telework if the employee is telework ready.

4. Official and Personal Travel:

a. Official Travel: Effective immediately travel to, from, or through

Outside the Continental United States (OCONUS) CDC Travel Health Notice (THN)

level 3 locations is prohibited. Mission essential travel to locations other

than CDC THN level 3 locations is permitted. Defer non-mission essential

travel to all locations until further notice.

b. Authority to Waive Policy: Waiver authority of the policies

delineated in this guidance, when mission critical, is delegated to the

Commandant of the Marine Corps (CMC) and Chief of Naval Operations (CNO),

and/or their designees but not below the level of General Officer, Flag

Officer, or Senior Executive Service for approval.

c. Temporary Additional Duty (TAD) and Permanent Change of Station (PCS)

Travel: All military and civilian personnel on TAD and PCS orders to, from,

or through OCONUS CDC THN level 3 locations are on hold until further notice.

Gaining and detaching commands should use authorities such as delay travel or

temporary duty travel on a case-by-case basis in order to decrease the

financial impact to Service Members delayed due to this policy. Service

Members should be placed in a telework, sick-in-quarters, or other non-

chargeable leave status for the duration of the hold.

d. DON Military Personnel: Personal or government-funded leave

with

travel to, from, or through OCONUS CDC THN level 3 locations is not

authorized. Waiver authority designees may approve exceptions for personal

travel to, from, or through OCONUS CDC THN level 3 locations.

e. DON Civilian Employees: Official travel to, from, or through OCONUS

CDC THN level 3 locations is not authorized for DoD civilian employees. DON

civilian employees with approved leave to OCONUS CDC THN level 1, 2, or 3 may

continue to travel to their desired locations but should be advised of the

health risk they may assume and requirements outlined in paragraph 5. Upon

return from approved leave, DON civilian employees who are telework ready may

be asked to telework for 14 days or more in order to ensure they have not

been exposed to the virus. Civilian personnel hiring actions for positions

in CDC THN level 2 and level 3 designated locations are postponed for non-

essential civilian personnel until restrictions are lifted.

f. Family Members: Concurrent official travel for family members of

Service Members and civilian personnel is denied to CDC THN level 2 and 3

locations for the next 60 days. Early return of dependent request process

and approval authority remain consistent with current policies.

g. Retiring or Separating Service Members Within the Next 60 Days:

These restrictions do not apply to retiring or separating Service Members

unless there is a need for self-quarantine per CDC guidelines.

h. Waivers or Exemption: Individuals traveling under a waiver or

exemption remain subject to travel screening protocols. Waivers may be

granted, by waiver authority, for compelling cases where the travel is: (1)

determined to be mission essential; (2) necessary for humanitarian reasons;

and (3) warranted due to extreme hardship. Waivers are to be done on a case-

by-case basis, shall be limited in number, and shall be coordinated between

the gaining and losing organizations.

i. DON travelers should carefully plan travel to ensure their scheduled

flights do not transit through or originate in OCONUS CDC THN level 2 or 3

locations. Travel on military aircraft shall ensure a screening of personnel

is conducted at the point of embarkation. At a minimum:

(1) Questionnaire to assess risk of exposure;

(2) Temperature check; and

(3) Visual check for signs and symptoms of COVID-19.

j. DON personnel traveling to or from a non-CDC THN level 2 or 3

location will inform their immediate supervisor of their travel itinerary and

a history of all locations traveled through and visited.

k. Transition to military or DoD contracted aircraft for DoD sponsored

travelers coming from or going to CDC level 2 or 3 designated areas, to the

greatest extent practical.

5. DON military and civilian personnel who have returned in the past 14 days

from countries or areas identified as OCONUS CDC THN level 2 or 3 locations,

or who have had close contact with someone with a confirmed infection of

COVID-19, will immediately notify their supervisor following service specific

guidelines: Navy see references (i) through (k) and Marine Corps see

references (l) through (m). Minimum self-quarantine procedures must follow

CDC issued guidelines at https://www.cdc.gov/coronavirus/2019-ncov.

Civilians subject to quarantine who are telework ready may be asked to

telework. Employees who are not telework ready may be granted weather and

safety leave in accordance with OPM guidance.

6. Pursuant to DoD and service regulations and policies, commands will

maximize the proportion of the workforce who may be eligible to perform their

duties via telework by ensuring appropriate personnel have a completed

telework agreement in place in accordance with command policy. Leadership

will identify and inform all military and civilian personnel designated as

mission essential who must report to duty during an outbreak.

7. Foreign Visits: Consistent with Joint Chiefs of Staff policy, all

foreign visits are cancelled until further notice. Exceptions may be granted

by CMC, CNO, and/or their designated representative(s).

8. All daily reporting requirements outlined in the above references will be

followed unless modified or cancelled by the appropriate organization.

9. Released by the Honorable Thomas B. Modly, Acting Secretary of the

Navy.//

BT

#0001

NNNN

UNCLASSIFIED//

Throwback Thursday Classic Post – Did You Really Fail to Select for Promotion?

If your name was not on the promotion list, you probably weren’t selected for promotion. There is, however, a chance that you actually were selected for promotion but your name was removed after the promotion board. Why would this happen?

After promotion boards there are some systems that are “scrubbed” to ensure that no adverse or reportable information exists for the officers selected by a promotion board or by an administrative board (the CO/XO/CMO/OIC board, for example). Here is a chart that shows you the systems that are checked:

As you can see, if you have problems with your security clearance, the Inspector General, Naval Criminal Investigative Services, or any legal issues, your name could be removed and your promotion put on hold. How do you tell if this happened to you?

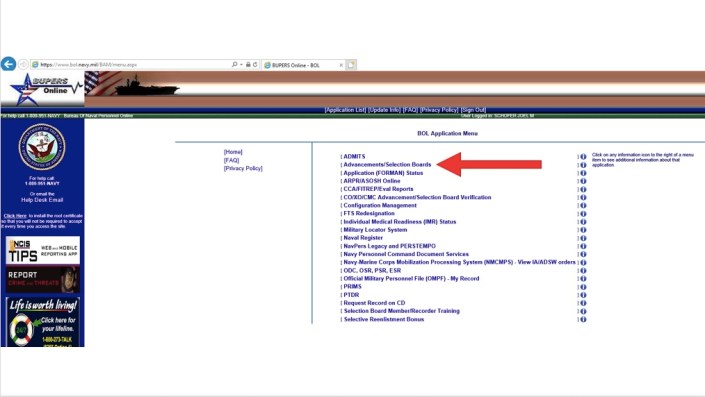

First, go to BUPERS On-Line and click on the link for “Advancements/Selection Boards” as pointed out with the large arrow:

Now you should see a screen similar to this one:

As you can see, I was a “SELECT” for O6. If you actually were a non-select for promotion you’d see a “N” where my “S” is. If you were “scrubbed” from the promotion list, you’ll see an “H” for HOLD.

If you don’t see anything, then you didn’t fail to select. You probably weren’t looked at by the board. This most often happens to people who trained in the NADDS program in civilian training programs and weren’t on active duty for a whole year. Sometimes, though, these people will show up on the reserve promotion lists, so don’t lose hope until you check that list as well. As of now, the FY19 LCDR list for the reserves isn’t out yet.

If you are on hold, I’d contact your Detailer to try and find out why.

Director and Deputy Director of Professional Education at NMRTC Lejeune – O5+

The Director of Professional Education (DPE) and Deputy DPE positions will be opening at NMRTC Camp Lejeune this spring/summer. They are hoping to have at least one of the positions filled by the end of April.

If you have interest and clearance from your Detailer, the info is in the position descriptions below:

Assistant/Deputy Chief of GME and Medical Director of the Darnall Medical Library at WRNMMC – O4+

Details are in this document, and applications are due 23 MAR. Make sure you are already at WRNMMC or USUHS or have Detailer clearance to apply:

Director of Branch Clinics in 29 Palms

The Director of Branch Clinics (DBC) position for NMRTC-29 Palms is opening. The deadline for applications is 1 APR 2020 with the ability to assume duties in MAY 2020. All inquiries can be addressed to LCDR Jeremy Ramsey (contact in the global). Details are in this document:

As usual, you need clearance from your Detailer to apply.