BRS

Throwback Thursday Classic Post – A Simple and Military Specific Summary of How to Save for Retirement

I’m a huge fam of Jim Lange. He’s a noted expert in financial management, saving for retirement, and estate planning. He’s written a number of books, some of which you can get for free on this page. If I ever move back to Pennsylvania, I’ll probably have him do my estate planning so that I don’t have to worry about anything in retirement.

He sends out a monthly newsletter that I get via snail mail, and it usually has a useful article in it. If you want it, you can get it here.

A previous edition had a section called “Jim’s Point-by-Point Summary of the Whole Retirement & Estate Planning Process.” It was simple but extremely useful. Below in bold are each of the points he lists for people who are still working, which is most of my readership. Let’s take each bolded point and militarize it for you so it is specific to those of us in the military.

Contribute at least the amount to your retirement plan that your employer is willing to match or partially match.

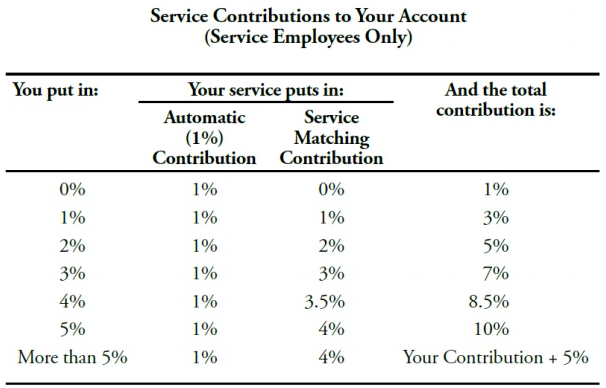

For those under the legacy retirement plan, this is not an option. For those under the new Blended Retirement System (BRS), you need to contribute 5% of your basic pay to the Thrift Savings Plan (TSP) to get the pull 5% DoD match:

You also need to make sure you contribute 5% every month and don’t fill the TSP too early. If you max it out in October, you won’t get a match in November or December.

If you can afford to, contribute the maximum allowed to your retirement plan even if your employer does not match.

This is $19,500 in 2021. You can do an extra $6,500 if you are 50 or over. You can even do more if you are in a combat zone.

Once you have maximized contributions to your plan at work, contribute the maximum you can to an IRA, even if you cannot take a tax deduction on it.

If you are able to fill your TSP account, next you’ll need to open an IRA at an investment firm. Vanguard is the obvious choice due to their across the board low investment fees and unique non-profit structure, but you can do this anywhere (Schwab, Fidelity, etc.).

If you make too much to contribute to a Roth IRA, you just use the back door Roth IRA option.

Consider your personal tax bracket when trying to decide if you should contribute to a Roth or a traditional IRA/retirement plan.

With a traditional plan, you take a tax deduction now and pay taxes later when you take the money out. With a Roth plan you pay the taxes now and the withdrawals are completely tax free.

The general principle is that if you are in a lower tax bracket now than when you are retired, you do the Roth. If you are in a higher tax bracket now, you use the traditional.

No one really knows what the future holds, though, making this decision tough. Here are some resources for you to check out when making this decision:

Traditional and Roth TSP Contributions

Roth vs. Traditional IRAs: A Comparison

Do not take loans against your retirement plan. Allow the tax-deferred or tax-free status of the account to maximize the growth of your money.

While the TSP allows loans, I refuse to link to any information about it. Once you put money away for retirement, you don’t borrow from it unless it is an ABSOLUTE EMERGENCY.

Period.

The Bottom Line

Here are the point-by-point summary of steps Jim Lange suggests you take if you are saving for retirement:

- Contribute at least the amount to your retirement plan that your employer is willing to match or partially match, which is 5% of basic pay in the BRS.

- If you can afford to, contribute the maximum allowed to your retirement plan even if your employer does not match, which is $19,500 in the TSP ($26,000 if you’re 50+).

- Once you have maximized contributions to your plan at work, contribute the maximum you can to an IRA, even if you cannot take a tax deduction on it. Use a back door Roth IRA if you need to.

- Consider your personal tax bracket when trying to decide if you should contribute to a Roth or a traditional IRA/retirement plan.

- Do not take loans against your retirement plan. Allow the tax-deferred or tax-free status of the account to maximize the growth of your money.

Military Times 2020 Guide to Military Benefits

Here’s a link to this on-line guide that covers Basic Pay, BAH, retirement, family support, VA loans, TRICARE, and educational benefits. It is a great resource if you have questions about how something works:

Guest Post – How to Apply for Continuation Pay Under the Blended Retirement System

By Dustin Schuett, DO

Note: The views expressed in this chapter are those of the author(s) and do not necessarily reflect the official policy or position of the Department of the Navy, Department of Defense, or the United States Government.

For those who elected into the Blended Retirement System (BRS), there is the opportunity to receive a one-time Continuation Pay bonus in exchange for 4 additional years of obligated service.

Continuation pay can in theory be taken anytime between 8 and 12 years of active service as calculated by the Pay Entry Base Date (PEBD, which can be found in block 4 of the LES labeled “PAY DATE”). The Navy (as well as the other branches) currently only allows Continuation Pay to be taken at the 12th anniversary of the member’s PEBD. Members can currently submit for Continuation pay when they are between 11.5 and 12 years from their PEBD. Essentially if you opted into the BRS and will be serving to 16 years due to pre-existing obligations or career plans/aspirations, you can take the continuation pay at 12 years. If you plan to get out of the Navy prior to serving 16 years, you should not take Continuation Pay as currently available.

The amount of the Continuation Pay can be set between 2.5 and 13 times monthly base pay for Active Duty servicemembers. The Navy (as well as the other branches) have taken the low end setting Continuation Pay bonus at 2.5x since its inception though 2020 rates have not been officially released. This bonus can be taken as a single lump sum or as 2 or 4 annual payments paying 50% or 25% per year respectively.

Understand that this means you will need to serve 4 years after receipt of the Continuation Pay. This obligation will “run concurrently with any other service obligation, unless other service obligations incurred specifically preclude concurrent obligations” per MILPERSMAN 1810-081 Section 7.

Verify that any pre-existing obligations can be served concurrent to (at the same time as) not consecutive to (following) any pre-existing obligations (ROTC, USNA, HPSP, USUHS, FTOS Training etc). I am currently carrying obligations for FTOS GME time for Fellowship training and a Retention Bonus which I am serving concurrently to my fellowship obligation as well as resident obligations. I contacted BUMED Special Pays who confirmed that my obligations do not require consecutive payback with other obligations.

I would strongly recommend anyone taking Continuation Pay to verify with BUMED Special Pays that their current obligations do not preclude a concurrent payback of obligation for Continuation Pay. Four years is a long additional commitment in exchange for only 2.5 months of base pay.

Here are the steps to obtain Continuation Pay in PDF form as well as below:.

- Go to the NSIPS website and log in.

- Select “Employee Self-Service” on the left side in the Menu box.

- Select “Blended Retirement System” under “Retirements and Separations” on the far right side.

- On the Blended Retirement System page, confirm that you are enrolled into the BRS and that the current date is between the 1st and last day eligible to elect by looking in the 2nd Box on this page.

- Select the “Continuation Pay” tab.

- Click the link for your “Continuation Pay Notification Letter” in the 3rd box from the top

- Save/print this letter for your records.

- Select “Yes, I elect Continuation Pay and agree to serve for an additional four years of obligated service from my date of eligibility”.

- Choose the Continuation Pay Payment option you desire from the listed options.

- Single Lump Sum Payment

- Two Annual Payments (50%)

- Four Annual Payments (25%)

- Click “Save” at the bottom of the page. This locks in your selection (don’t worry, you can still change the selection and opt out if you desire).

- I recommend checking to ensure everything has saved, to do this:

- Click “Home” in the top right corner of the page.

- Follow steps 2-5 above and ensure that your selections have been saved.

- Await your payment which per MILPERSMAN 1810-081 Section 8 b. will be on the 12th year anniversary of your PEBD (Pay Entry Base Date).

References:

The Blended Retirement System Lump Sum – Probably Not a Good Idea

Now that the Blended Retirement System (BRS) is in full effect, it is time to start digging a little deeper on some of its features, like the lump sum payment. Here is a pocket card put out by the DoD Office of Financial Readiness to explain the lump sum feature of the BRS:

Reading through the card, I think it does the best job I’ve seen so far at explaining how the lump sum option works, especially for those who don’t understand what discounting is:

Discounting is the process of determining the present value of a payment or a stream of payments that is to be received in the future. Given the time value of money, a dollar is worth more today than it would be worth tomorrow. Discounting is the primary factor used in pricing a stream of tomorrow’s cash flows.

When discounting future cash flows to determine the present value, you have to use what is very much like a reverse interest rate, called the discount rate:

The discount rate also refers to the interest rate used in discounted cash flow analysis to determine the present value of future cash flows.

The higher the discount rate, the lower the present value of your future cash flows and the smaller your lump sum would be. Some have criticized the DoD for setting the discount rate too high. While adjusted annually, it is 6.75% for 2020.

What I really found interesting about this pocket card I had found, and what caused me to write this blog post, was this part of it:

Note that the DoD Office of Financial Readiness is admitting, “For most Service members, a guaranteed stream of income for life is likely better than a lump sum.”

Yes! One of my biggest beefs against the BRS is that it gives you options like this and the chance to make a mistake. You can’t screw up the guaranteed stream of inflation-adjusted income that comes with the legacy retirement system.

You can screw up a lump sum, reduced by a high discount rate, by blowing it on an expensive car, too large of a house, a weekend in Vegas, or whatever else people like to waste money on. Yes, you could use it productively, perhaps to start a business, buy a franchise, or acquire high-paying skills with further education. But you could just as easily buy one of these:

Do yourself a favor. If you are in the BRS, when the time comes think long and hard before you reduce your future income streams and take a lump sum payment. As the DoD itself admits, “For most Service members, a guaranteed stream of income for life is likely better than a lump sum.”

Make Sure You Snatch the Blended Retirement System Match

Here’s a tip from one of my favorite blogs and authors, Jonathan Clements from Humble Dollar:

SNATCH THE MATCH. Are you on track to contribute enough to your 401(k) to get this year’s full matching employer contribution? If not, crank up your contribution now, so you can spread the required sum over this year’s remaining paychecks. In 2020, the maximum 401(k) contribution is $19,500, or $26,000 if you’re age 50 or older.

For nearly my entire career this wasn’t an issue for those in the military, but it is now due to the new Blended Retirement System (BRS) and its matching Thrift Savings Plan (TSP) contributions. To refresh your memory, if you contribute 5% of your pay to the TSP you get up to a 5% match. If you are in the BRS and you don’t contribute at least 5% every month, you are leaving free money on the table:

Also, you want to make sure you don’t fill up your TSP too early. While many service members will find it hard to get to the 2020 annual limit of $19,500, for those that do they want to space it out over the whole year. If you fill up your TSP in October and can no longer contribute for November or December, you won’t a get a match that month and will lose out on that money.

While I’m not in the BRS, I do a few things with my TSP contributions that I’d recommend everyone do:

- Contribute from your basic pay and not from bonuses or other variable or one-time pays. Your basic pay is the most consistent so use that.

- Spread it out over the whole year. For 2020, I’m contributing about $1625/month so that I come in just at the $19,500 limit in December.

- I see how much of my TSP is left after the November LES is released, and adjust December to get as close to the limit as possible.

A Simple and Military Specific Summary of How to Save for Retirement

I’m a huge fam of Jim Lange. He’s a noted expert in financial management, saving for retirement, and estate planning. He’s written a number of books, some of which you can get for free on this page. If I ever move back to Pennsylvania, I’ll probably have him do my estate planning so that I don’t have to worry about anything in retirement.

He sends out a monthly newsletter that I get via snail mail, and it usually has a useful article in it. If you want it, you can get it here.

A previous edition had a section called “Jim’s Point-by-Point Summary of the Whole Retirement & Estate Planning Process.” It was simple but extremely useful. Below in bold are each of the points he lists for people who are still working, which is most of my readership. Let’s take each bolded point and militarize it for you so it is specific to those of us in the military.

Contribute at least the amount to your retirement plan that your employer is willing to match or partially match.

For those under the legacy retirement plan, this is not an option. For those under the new Blended Retirement System (BRS), you need to contribute 5% of your basic pay to the Thrift Savings Plan (TSP) to get the pull 5% DoD match:

You also need to make sure you contribute 5% every month and don’t fill the TSP too early. If you max it out in October, you won’t get a match in November or December.

If you can afford to, contribute the maximum allowed to your retirement plan even if your employer does not match.

This is $19,500 in 2020. You can do an extra $6,500 if you are 50 or over. You can even do more if you are in a combat zone.

Once you have maximized contributions to your plan at work, contribute the maximum you can to an IRA, even if you cannot take a tax deduction on it.

If you are able to fill your TSP account, next you’ll need to open an IRA at an investment firm. Vanguard is the obvious choice due to their across the board low investment fees and unique non-profit structure, but you can do this anywhere (Schwab, Fidelity, etc.).

If you make too much to contribute to a Roth IRA, you just use the back door Roth IRA option.

Consider your personal tax bracket when trying to decide if you should contribute to a Roth or a traditional IRA/retirement plan.

With a traditional plan, you take a tax deduction now and pay taxes later when you take the money out. With a Roth plan you pay the taxes now and the withdrawals are completely tax free.

The general principle is that if you are in a lower tax bracket now than when you are retired, you do the Roth. If you are in a higher tax bracket now, you use the traditional.

No one really knows what the future holds, though, making this decision tough. Here are some resources for you to check out when making this decision:

Traditional/Roth TSP Comparison Matrix

Roth vs. Traditional IRAs: A Comparison

Do not take loans against your retirement plan. Allow the tax-deferred or tax-free status of the account to maximize the growth of your money.

While the TSP allows loans, I refuse to link to any information about it. Once you put money away for retirement, you don’t borrow from it unless it is an ABSOLUTE EMERGENCY.

Period.

The Bottom Line

Here are the point-by-point summary of steps Jim Lange suggests you take if you are saving for retirement:

- Contribute at least the amount to your retirement plan that your employer is willing to match or partially match, which is 5% of basic pay in the BRS.

- If you can afford to, contribute the maximum allowed to your retirement plan even if your employer does not match, which is $19,500 in the TSP ($26,000 if you’re 50+).

- Once you have maximized contributions to your plan at work, contribute the maximum you can to an IRA, even if you cannot take a tax deduction on it. Use a back door Roth IRA if you need to.

- Consider your personal tax bracket when trying to decide if you should contribute to a Roth or a traditional IRA/retirement plan.

- Do not take loans against your retirement plan. Allow the tax-deferred or tax-free status of the account to maximize the growth of your money.