Author: Joel Schofer, MD, MBA, CPE

COVID-19 Travel Restrictions Installation Status Update, Oct. 7, 2020

Here is the latest update:

Learn About Irregular Warfare

When you are preparing for interviews for positions in the Navy, you want to have read recent strategic guidance. Here are some recent updates on irregular warfare:

Great Power Competition Can Involve Conflict Below Threshold of War

Irregular Warfare Annex to National Defense Strategy Made Public

Here’s a Defense News article that discussed these issues as well:

Irregular warfare strategies must move beyond special forces, Pentagon says

Check Your Fund Expenses

Jonathan Clements was a longtime personal finance columnist for The Wall Street Journal, and he offers great advice at the best price you can get (free) on his blog Humble Dollar. Here is one piece of advice from his site:

CHECK YOUR FUND EXPENSES. If you own index funds, aim for weighted average annual expenses below 0.2%. If you own actively managed funds, you’ll pay more—but allocate enough of your portfolio to index funds to keep your average below 0.4%. By holding down costs, you’ll keep more of what you make, plus low-cost funds typically outperform high-cost competitors.

In the military, we’re blessed with the Thrift Savings Plan (TSP) and its industry leading low expenses. Outside of the TSP, if you want to keep your costs down you should just invest with Vanguard. Their unique structure makes them a non-profit, unlike their competitors, so no matter what you invest in you know it will be among the lowest cost investments available. Admittedly, though, there is a price war and you can find the same funds for even lower costs at Schwab and Fidelity.

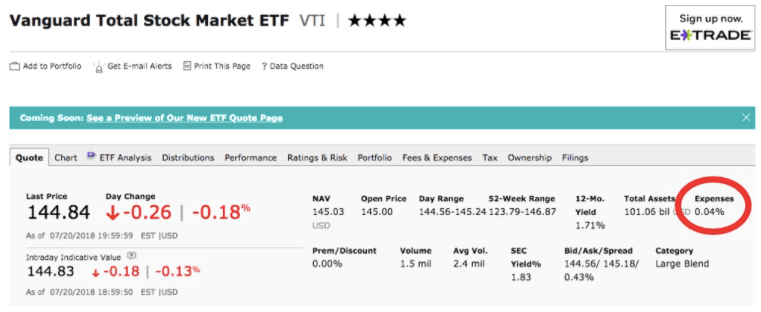

Whatever you invest in, take the time to look up the investments at Morningstar. Just type your investment in the search bar at the top and check the expense ratio. As an example, I typed in VTI, which is the Vanguard Total Stock Market Exchange Traded Fund (ETF). The expense ratio of 0.04% is circled in red:

As Mr. Clements mentions, if the expense ratios for index funds are more than 0.2% then you are paying too much. You should try to keep the total expense ratio of all your investments less than 0.4%.

Why Didn’t More GMOs, UMOs, and Flight Surgeons Promote to O4?

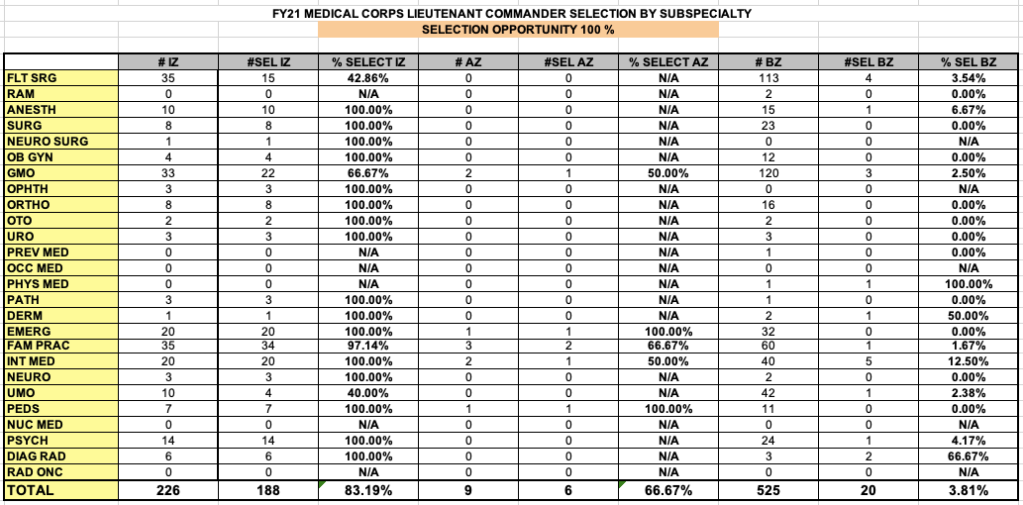

I’ve been asked this question multiple times since the FY21 LCDR promotion board stats came out. Many looking at the stats noticed these facts:

- The overall in-zone promotion rate was 83.19%.

- The rate for GMOs, UMOs, and Flight Surgeons were all lower than this:

- GMO – 66.67%

- UMO – 40%

- Flight Surgery – 42.86%

This seems to argue against the recent advice to “go operational” to successfully compete for promotion. What gives? The following is my best guess, and it is a guess. I was not on the board, and if I was I wouldn’t be able to talk about it.

Let’s look at the typical career path for a Medical Corps LT who does GMO, UMO, or Flight Surgery:

- Year 0 – Graduate from medical school and put on LT.

- Year 1 – Finish internship and go GMO, UMO, or Flight Surgery.

- Years 2-4 – Do a 2-3 year operational tour.

- Years 3-4 – Match in a residency program.

- Year 5 – You are in-zone for LCDR.

If in year 5 you are still a GMO, UMO, or Flight Surgeon, you probably haven’t matched in a residency either because you can’t or you’ve chosen to pay back the 3-4 years you owe the Navy and get out. In the latter case, you may have approved resignation orders in the system, which the promotion board will see on your record.

This timeline is obviously not applicable to anyone with prior service, entry-grade credit, or an abnormal promotion timeline, but it is applicable to the majority of Medical Corps LTs. For example, I did internship, 1 year as a GMO, 3 years of residency, and then was picked on-time/in-zone for LCDR, which I put on as a staff Emergency Physician. Back in the day, I showed up in the stats under Emergency Medicine. Anyone in a residency will show up under their specialty’s statistics.

Bottom Line – Why didn’t more GMOs, UMOs, and Flight Surgeons promote to LCDR?

Again, this is just a guess, but if you are in an operational billet your 5th year you either can’t match in a residency or are getting out, both of which do not portend well for promotion.

Takeaway – Your primary job and career goal as a LT is to match in a residency program that will lead to board certification. You can always “go operational” later. Spending too much time in the operational setting can lead to difficulties promoting.

On-Line Global Health Training

Please see the message from the Global Health Engagement Office:

GHEO is committed to providing educational opportunities for our GHE community. While the COVID-19 pandemic continues to put in-person trainings on hold, there are an abundance of online trainings available. On Milsuite you will find a list GHE-related trainings that you may take online:

https://www.milsuite.mil/book/groups/navy-global-health-engagement

If you are aware of any additional trainings that are not included on this list, please send them to our office for inclusion.

V/r,

CAPT Huddleston

Director, Global Health Engagement

BUMED Liaison to USAID

Office of Global Health Engagement (M52)

Finance Friday Articles

Here are my favorites:

- 6 Fixed-Income Options for a Low-Yield Environment

- Anchoring & Adjustment in the Stock Market

- Seems So Easy

- True Wealth

Here are the rest of the articles:

- Analyzing Winning Mutual Funds

- Buy One Property a Year and Retire Early

- Can I Employ My Spouse?

- Five Reasons I Like Hanging Out with Millionaires

- How to Buy a Second Home that Pays for Itself

- How to Deal with High Anxiety Due to the Election

- How to Find an Emerging Real Estate Market

- International Stocks & Asset Location: Is Taxable or Tax-Advantaged Best?

- Is Refinancing Your Student Loans the Right Move?

- Low Income Doctor in a High Cost of Living Area

- Not Exactly True

- Student Loan Advice: 7 Rules of Thumb

- The Arrival Fallacy

- The Coming Psychological Revolution in the Housing Market

- The Importance of Automating Your Real Estate Investments

- Wanting a tax deferral opt-out a ‘reasonable issue,’ says Trump official

- What to Do with Suboptimal Assets in Your Portfolio

- What You Need to Know About Ground-Up Multifamily Development

COVID-19 Travel Restrictions Installation Status Update, Sept. 30, 2020

Here are the latest updates:

Throwback Thursday Classic Post – Step 6 to Crush the TSP – Rebalance Annually

We’ve talked about steps 1-5 to crush the Thrift Savings Plan (TSP). Now we move on to the final step (unless I think of more), step 6 – rebalance annually.

What is Rebalancing?

Let’s say that your desired TSP asset allocation is 70% stocks and 30% bonds. After the last year, though, stocks earned more than bonds and now you’re sitting at 85% stocks and 15% bonds. In order to rebalance back to your desired asset allocation, you’d sell approximately 15% of your stocks and buy bonds, restoring your desired asset allocation. It’s that simple.

Why Should You Rebalance?

If you don’t, you may be assuming more or less risk than you desire.

Also, by rebalancing you force yourself to sell what has overperformed and buy what has underperformed. Although this seems counter-intuitive because you are selling what has given you the largest return, by doing this you are systematically selling high and buying low. When left to themselves, investors typically buy high and sell low, the opposite of what you want to do. Rebalancing forces you to do it right.

How Often Should You Rebalance?

Vanguard has researched this, and you can read their full report here:

Best Practices for Portfolio Rebalancing

Their conclusion is:

We conclude that for most broadly diversified stock and bond fund portfolios (assuming reasonable expectations regarding return patterns, average returns, and risk), annual or semiannual monitoring, with rebalancing at 5% thresholds, is likely to produce a reasonable balance between risk control and cost minimization for most investors.

In other words, you rebalance annually or semiannually (twice per year) whenever your current asset allocations are off by 5% or more from your desired allocations. If the current and desired allocations are within 5% of each other, you do nothing.

How Do You Rebalance in the TSP?

You just log on and do what they call an “interfund transfer” or IFT. You can read all about it on this page from the TSP website.

Because you are doing it in a tax-advantaged retirement account, there are no expenses, fees, or taxes associated with rebalancing (unlike if you were rebalancing a taxable account).

You can only do it twice per month without restrictions, but since you are smart you are only doing it once per year anyway.

Do You Need to Rebalance With Lifecycle Funds?

No, you don’t. This is one of the major advantages of the L funds. If you are hitting the easy button on your TSP and just using a Lifecycle fund, you don’t need to rebalance…EVER!

That’s It. Crush the TSP!

That’s the final step to crush it in your TSP account. Read the whole series, maximize your TSP contributions, and get rich in the military.

CTF-80 Surgeon Position – Norfolk, VA

The CTF-80 Surgeon position is opening in 2021 and the PD with all the info on the billet is here:

Packages must include submission of a Bio, CV and Letter of Intent (LOI) no later than 1 NOV 20. The POC for submission is CAPT Todd Gardner, Senior Detailer. His e-mail address is in the PD above.