Author: Joel Schofer, MD, MBA, CPE

PPT About Transferring GI Bill Benefits

Here is what appears to be a useful PPT about a process people frequently jack up:

Save Some for Your Future Self

Jonathan Clements was a longtime personal finance columnist for The Wall Street Journal, and he offers great advice at the best price you can get (free) on his blog Humble Dollar. Here is one piece of advice from his site:

“SAVE SOME FOR YOUR FUTURE SELF. Looking to lose weight? At restaurants, transfer half your serving to a second plate and ask the waiter to box it up. If the food will make good leftovers, it’s easy to do, because you know you’ll have a treat tomorrow. Want to save more? Think about it the same way—and set aside some of today’s spending money for tomorrow.”

If you are wondering how much to save for your future self, here are a few ways to figure that out.

To start, you have to figure out your gross (pre-tax) income. Include every dollar you get, even the non-taxable allowances. If you’re not sure exactly, take your best guess.

The Minimum

In my opinion, the absolute bare minimum you need to save for retirement is 10% of your gross income. You can include all of your employee contributions in this, like the DoD match in the Blended Retirement System. This doesn’t have to all be your money.

That said, 10% is the minimum. You’ll likely work into your 60s unless you stay in long enough to have a pension.

The Most Common Recommendation

Most commonly people recommend you save 12-15% of your gross income for retirement. If you read this article from Vanguard about how much to save, you’ll see:

If retirement is decades away, setting a specific goal amount is probably unnecessary. For now, focus on:

1. Immediately saving at least enough to get the full match offered by your employer plan, if you have one. This is free money—don’t let it pass you by.

2. Working your way up to 12%–15% of your pay, including any employer match. For example, you could increase your savings rate 1% every year until you reach your target rate. This should get you in the ballpark of what you’ll need.

The Early Retirement Recommendation

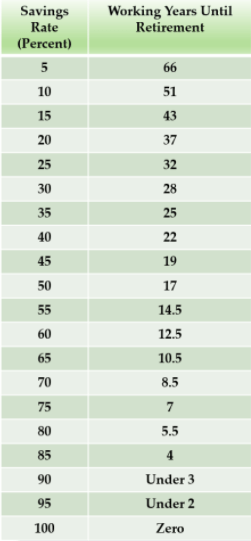

If you want to achieve financial independence or have the option of retiring early, you probably need to save more than 15%. Mr. Money Mustache’s amazing post about the shockingly simple match of early retirement has this table that shows you how long you’ll need to work based on your savings rate:

The Bottom Line

Start with your gross pay. You need to save a minimum of 10% of that, but you should try to save at least 15%. If you want to achieve financial independence and have the option to retire early or go to part-time work, you need to save more than 15%. I’d recommend 20% or more. I’ve done 30% my whole career.

If you want out help saving for retirement, start here where we discuss it in more depth.

Finance Friday Articles

- 7 Truths From a Gut-Wrenching Stock Market Crash, One Year Later

- 12 Things to Know About Choosing a Financial Advisor

- Everyone is Using The 4% Rule Wrong

- Retirement Checklist for Physicians

- Second TSP investment manager to be added

- The Simplest Asset to Hedge Against Inflation

- Top 10 Ways to Lower Your Taxes

- We’re All Active Investors

- You have an extra month to file your federal tax returns

Throwback Thursday Classic Post – All the Posts About Letters to the Board in One Place

The question most people ask me is answered in these posts:

Should You Send a Letter to the Promotion Board?

Do You Still Need to Send the Above Zone Letter?

The bottom line is:

Pretend that you did not send a letter to the board, the board is over, and you were not selected for promotion. Are you going to be kicking yourself for not sending the letter? If the answer is yes or maybe, then send the letter. As long as you keep it short and sweet, there is no real downside.

Frankly, I think that when officers send letters to promotion boards they are often just making themselves feel better, and there is nothing wrong with that. You want to make sure that when the promotion board results come out, no matter what happened, you feel like you did everything you could to get promoted.

Letters to promotion boards have a new due date. You can’t send them the day before the board anymore:

Letters to Promotion Boards Now Due 10 Calendar Days Before the Board

If you know you are getting out of the Navy and really don’t care about getting promoted, you should read this post:

What is a “Don’t Pick Me” Promotion Board Letter? Why Would You Send One?

Have you been on active duty for less than 1 year? Read this:

How to Be Considered for Promotion if You’ve Been on Active Duty for Less Than 1 Year

You now need to use your DoD ID number and not your Social Security number on letters to the board. Read this:

Use DoD ID Number and Not Your SSN on Letters to the Board

You can now submit letters electronically:

Director for Mental Health at NMRTC San Diego

See the announcement for all the details:

Applications are due 2 APR 2021 (POC in the above file), and anyone applying needs Detailer clearance to do so.

Estimate Your Retirement Income Needs

Jonathan Clements was a longtime personal finance columnist for The Wall Street Journal, and he offers great advice at the best price you can get (free) on his blog Humble Dollar. Here is one piece of advice from his site:

“ESTIMATE YOUR RETIREMENT INCOME NEEDS. Take your annual salary. Subtract how much you save each year and pay in Social Security payroll taxes. Also subtract your annual debt payments, including your mortgage—assuming these debts will be paid off by retirement. Result: You’ll know roughly how much you will need each year for a comfortable retirement.”

I’ll take this action one step further. Once you have the rough estimate of how much annual retirement income you need, go to this calculator and figure out how much your military pension will be worth. Then go to this calculator and figure out how much Social Security you’ll get. What is left is what you need to generate with the rest of your investments. Now take that number and divide it by 0.04. That is approximately how much you need to accumulate in your investment accounts to be able to retire.

For example, let’s say you use Mr. Clements’ method and get a number of $120,000/year for a comfortable retirement. The calculators tell you that you will get about a $42,000/year military pension and $18,000/year from Social Security. That leaves $60,000/year you need to generate from your investments. Divide that by 0.04 and you get $1,500,000, which is how much you’d need in your investment accounts to retire.