Save Some for Your Future Self

Jonathan Clements was a longtime personal finance columnist for The Wall Street Journal, and he offers great advice at the best price you can get (free) on his blog Humble Dollar. Here is one piece of advice from his site:

“SAVE SOME FOR YOUR FUTURE SELF. Looking to lose weight? At restaurants, transfer half your serving to a second plate and ask the waiter to box it up. If the food will make good leftovers, it’s easy to do, because you know you’ll have a treat tomorrow. Want to save more? Think about it the same way—and set aside some of today’s spending money for tomorrow.”

If you are wondering how much to save for your future self, here are a few ways to figure that out.

To start, you have to figure out your gross (pre-tax) income. Include every dollar you get, even the non-taxable allowances. If you’re not sure exactly, take your best guess.

The Minimum

In my opinion, the absolute bare minimum you need to save for retirement is 10% of your gross income. You can include all of your employee contributions in this, like the DoD match in the Blended Retirement System. This doesn’t have to all be your money.

That said, 10% is the minimum. You’ll likely work into your 60s unless you stay in long enough to have a pension.

The Most Common Recommendation

Most commonly people recommend you save 12-15% of your gross income for retirement. If you read this article from Vanguard about how much to save, you’ll see:

If retirement is decades away, setting a specific goal amount is probably unnecessary. For now, focus on:

1. Immediately saving at least enough to get the full match offered by your employer plan, if you have one. This is free money—don’t let it pass you by.

2. Working your way up to 12%–15% of your pay, including any employer match. For example, you could increase your savings rate 1% every year until you reach your target rate. This should get you in the ballpark of what you’ll need.

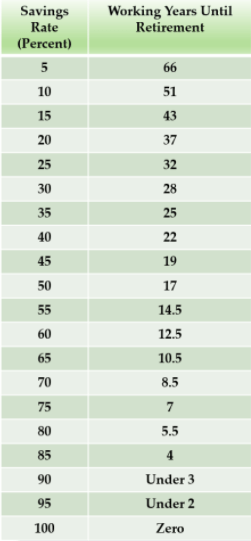

The Early Retirement Recommendation

If you want to achieve financial independence or have the option of retiring early, you probably need to save more than 15%. Mr. Money Mustache’s amazing post about the shockingly simple match of early retirement has this table that shows you how long you’ll need to work based on your savings rate:

The Bottom Line

Start with your gross pay. You need to save a minimum of 10% of that, but you should try to save at least 15%. If you want to achieve financial independence and have the option to retire early or go to part-time work, you need to save more than 15%. I’d recommend 20% or more. I’ve done 30% my whole career.

If you want out help saving for retirement, start here where we discuss it in more depth.