Finance Friday Articles

Here is an article about the pay raise we just got:

Biggest military pay raise in years takes effect Jan. 1; check out the complete chart

Here are my favorites this week:

3 Examples of Why Workaholic Real Estate Investors Have It All Wrong

6 Subjects That Should Have Sparked Your Curiosity in 2019

SECURE Act — 8 Things You Need to Know

Here are the rest of the articles:

7 Financial Planning Tips for Locums Docs

11 SMART Financial Goals for Your New Year’s Resolutions

An Unkind Act – The SECURE Act

Donating to a Vanguard Charitable Donor Advised Fund from a Vanguard Brokerage Account

How The SECURE Act Changes Your Retirement Planning

Investing in a Three Fund Portfolio Across Numerous Accounts. Get the Spreadsheet!

Is Buying Stocks at an All-Time High a Good Idea?

It’s So Important to Diversify Your Real Estate Portfolio

Risk Management in Private Real Estate: 3 Types of Uncertainty

SECURE Act And Tax Extenders Creates Retirement Planning Opportunities And Challenges

Thanks for Nothing, Financial Advisor

There are two versions of the S&P 500 index — this is the better investment

The Keys to Financial Success Are Incredibly Mundane (Sorry!)

The SECURE Act: What You Should Know About Retirement Account Reforms

Throwback Thursday Classic Post – Do You Still Need to Send the Above Zone Letter?

The standard advice has always gone something like this:

If you are above zone, you need to send a letter to the promotion board so that they know you are still trying to promote. Otherwise they won’t pick you.

Now that they no longer stamp officer records with “AZ” (above zone) and they look exactly the same as those records that are in zone, do you still need to write a letter to the board? Has the standard advice changed?

Reasons to Send a Letter to a Promotion Board

I addressed this in a post from a few years ago entitled “Should You Send a Letter to the Promotion Board?” I still agree with just about everything in that post, except for this:

“…you should always send a letter to demonstrate interest in getting promoted when you are above zone.”

In my opinion, you no longer need to send a letter just because you are above zone. If you have another reason to send a letter, then please do. If you are just sending one because you think you have to, I think that is no longer necessary.

The O6 promotion board convening orders state:

…in determining which officers are best and fully qualified for promotion, you are required to equally consider both above-zone and in-zone officers.

What if You’re Not Sure?

As you might imagine, I get asked a lot whether someone should send a letter to the promotion board. This is my standard response…

Pretend that you did not send a letter to the board, the board is over, and you were not selected for promotion. Are you going to be kicking yourself for not sending the letter? If the answer is yes or maybe, then send the letter. As long as you keep it short and sweet, there is no real downside.

Frankly, I think that when officers send letters to promotion boards they are often just making themselves feel better, and there is nothing wrong with that. You want to make sure that when the promotion board results come out, no matter what happened, you feel like you did everything you could to get promoted.

The Bottom Line

If you are above zone and want to send the letter just so there is no regret, feel free, but it is definitely not required to be considered for promotion.

2020 State of the Blog, the Facebook Group, and The Book

At the beginning of every year I give a general update on how the blog is doing. Enjoy!

Profit

As during previous years, profit was negative $99. I make no money on this, and it costs me $99/year.

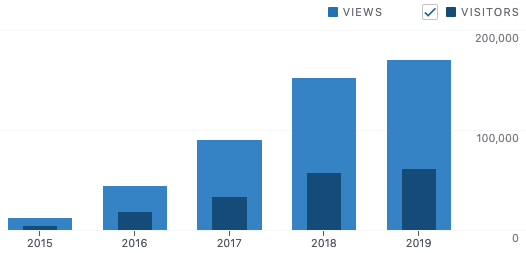

Blog Traffic

Here’s a graph of blog traffic since the blog was started in mid-2015:

The lighter color is page views and the darker color is visitors:

- 2015 – 3,705 visitors viewed 10,870 pages with 66 posts published

- 2016 – 18,373 visitors viewed 43,673 pages with 133 posts published

- 2017 – 32,569 visitors viewed 88,263 pages with 194 posts published

- 2018 – 56,674 visitors viewed 151,044 pages with 212 posts published

- 2019 – 60,771 visitors viewed 169,684 pages with 371 posts published

10 Most Popular Blog Posts and Pages in 2019

Here are the 10 most popular pages and posts in 2019:

- Joel Schofer’s Promo Prep – 4,065 views

- LCDR Fitreps – Language for Writing Your Block 41 – 3,682 views

- Joel Schofer’s Fitrep Prep – 3,035 views

- Useful Documents – 2,791 views

- POM20 Navy Medicine Billet Reduction – 2,556 views

- CV, Military Bio, and Letter of Intent Templates – 2,367 views

- Useful Links – 1,989 views

- Personal Finance – 1,407 views

- What are AQDs and How Do You Get Them? – 1,223 views

- About Me – 1,083 views

MCCareer.org Private Facebook Group

Some of the blogs I read have vibrant forums and Facebook groups where members interact and ask each other questions. I once started a forum on MCCareer.org, but no one used it so I folded it up. I still have a private Facebook group, though, with over 260 members.

Despite people joining the Facebook group, no one ever posts comments or questions to it. I think there’s only been one in two years. Plenty of people contact me individually to ask questions, so I know there are a lot of questions out there. In 2020, I’d encourage readers to use the Facebook group to get opinions and answers from people other than me.

MCCareer.org “The Book”

Very slowly we’ve been posting “chapters” to the MCCareer.org “book.” Book is in quotes because it really isn’t a book, but more of a collection of on-line posts or chapters. Interest in writing “chapters” has been low so far, although a few authors other than me have pitched in. Most chapters thus far have been written by me.

I’ve begun the process of adding all of my posts to the book page, as you’ll see if you take a look. Slowly but surely I’ll fill out the content outline with what I’ve already written, and if there are holes I’ll write content to fill it in.

I considered creating a wiki page instead, but I’m not willing to give up editorial control. Occasionally someone will post something inappropriate to the blog, and I need to make sure nothing gets posted that would derail my Naval career.

Check out “The Book” when you get a chance and see if there is something you’d be interested in contributing. If there is, contact me.

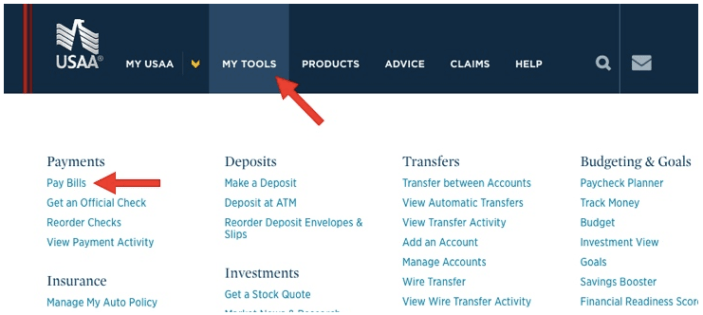

Automate Your Bill Paying

Here’s a tip from one of my favorite blogs and authors, Jonathan Clements from Humble Dollar:

AUTOMATE YOUR BILL PAYING. That way, you’ll avoid late payments—crucial to maintaining a good credit score. The downside: You need to be vigilant about keeping enough in your bank account, so you don’t trigger fees for overdrafts or insufficient funds. This is a particular concern with credit card bills, which can vary so much from one month to the next.

How do you do this with USAA, which is where I do my banking?

To sign up with USAA, go here:

Authorship and Academic Careers in the Navy

I recently gave a talk to the Emergency Medicine residents at NMC Portsmouth about authorship and academic careers in the Navy. Here is the outline of the talk and some tips…

Academic Career Options

There are a number of options for those who are interested in establishing an academic career in Navy Medicine. Here are the ones I know of:

- Residency programs at a medical center – Serving as teaching faculty at a residency program at Walter Reed, San Diego, or Portsmouth.

- Family Medicine (FM) teaching hospitals – Serving as faculty at the FM residency programs in Ft. Belvoir, Lejeune, Camp Pendleton, and Jacksonville. This opportunity is not just for FM physicians, but for Internists, Pediatricians, subspecialists, etc. as the FM programs need all of those people to support the education of their residents.

- Japanese internships – Both Yokosuka and Okinawa have internships that are structured like Transitional Internships and allow Japanese physicians to learn how American medicine is conducted. Most graduates try to obtain letters of recommendation and apply for graduate medical education (GME) in the US. Taking a leadership role in these programs can prepare you to lead GME programs when you PCS back to the US.

- Transitional internship programs – Leadership opportunities in Transitional Internships are open to just about every specialty, and many physicians have used Transitional Internship Program Director as the stepping stone to O6.

- Uniformed Services University of the Health Sciences (USUHS) billets – Many specialties have billets at USUHS that allow you to take a leadership role in the departments and teach medical students.

Authorship Options

The opportunities to publish have increased dramatically during my 18.5 year career. For example, you’re reading this blog and that didn’t exist when I started. Here are the opportunities to publish that currently exist with some tips listed after each:

- Apps – This is the only thing on this list I haven’t tried, but there are articles that explain how to do it and tell stories of physicians who made money doing it.

- Blogs – This isn’t hard to do, so there’s nothing but time and effort preventing you from putting your opinion out there for others to read. Don’t underestimate how much time this takes, though, so know what you are getting into. I have literally spent thousands of hours on this blog.

- Books and book chapters – I’ve published 4 books (you can see 3 of them on Amazon here) by working with my specialty society, so that is one opportunity to pursue when it comes to books. The easiest way to start writing books chapters is to find someone you know that is senior to you who already writes chapters and offer to be a co-author for the next edition. If you go to your department head/chair or residency director, they should be able to tell you who writes book chapters in the department.

- Case reports – This is the entry path to publishing and where I made most of my initial academic bones. Frankly, publishing case reports gotten me a lot of my academic reputation, fitrep impact in block 41, and subsequent promotion to O4 and O5. Nowadays, there are a lot of journals and it is easier than ever to get something accepted, especially if you are open to publishing cases on blogs or in newsletters.

- Humanities – Many journals regularly publish 1-2 page articles about the experience of being a physician, ethics, military medicine, and other related topics. A common way to get one of these published would be to deploy and then write a humanities piece while deployed or upon returning about your experience.

- Newsletters – I wrote a personal finance column in one of our specialty society newsletters for 7 years. If you can get a regular gig like this, it will force you to write on a regular basis and really build your CV and academic reputation. Every specialty has newsletters and “throw away” journals that arrive in the mail. Contact the editors, offer to write something, and see if this is something you enjoy.

- Podcasts – Similar to blogs, this is fairly easy to do with some free software (Audacity), a $50 USB microphone headset, a podcast host (I host on this blog’s WordPress site but here are other hosts out there), and the time to figure out how to post your content on the Apple store. Like blogging, it is very time consuming. Personally, it is not my favorite thing to do (which is why my podcast has lagged way behind) because I have zero interest in learning how to properly edit recordings, but there is nothing preventing you from getting your voice out there.

- Research manuscripts – If you want to do research, you should start with the Institutional Review Board (IRB) that your command is subject to. There will be resources available to help you, but in my experience it is a pull system (you have to inquire and go get them) and they are not pushed to you. Typically, you’ll find grant writers, statisticians, and sources of money to do research. You’ll also find additional military rules and regulations heaped on top of all of the already existing IRB rules and regulations. This latter fact is what dissuaded me from doing a lot of research in my academic career.

- Review articles – Most journals solicit authors to write review articles, so it is hard to get one accepted if it is unsolicited. That said, if you shorten it a bit by focusing on a more narrow topic and build it around a case presentation, you can get them accepted as case reports.

How to Build Your Academic Career in the Navy

What is the easiest way to build an academic career? It is simple but not easy. Not that many people follow through on it. Here are the steps:

- Obtain a USUHS faculty appointment – This blog post tells you how to do it.

- Progress toward promotion

This 2nd step is the step that most people fail to follow through on. They get appointed as an Assistant Professor, and then they stop working toward promotion to Associate Professor or full Professor.

In general, an Assistant Professor is a local/regional expert, an Associate Professor has established themself as a regional/national expert, and a full Professor has reached national or international acclaim. If you touch base with your USUHS department once a year and get their assessment about what steps you need to take to get promoted, you will be forcing yourself to progress in your academic career.

For example, I’m an Associate Professor of Military & Emergency Medicine and recently applied to be a full Professor. The feedback I was given was that I needed 3-4 more peer-reviewed publications as the first author. I may or may not choose to try and get them, but at least they gave me an honest assessment of what I needed to do. If you do this annually, you’ll get actionable feedback that you can address as you build your academic chops.

Asset Location

Here’s a tip on asset location from one of my favorite blogs and authors, Jonathan Clements from Humble Dollar:

After deciding what investments to buy, we should consider asset location. What’s that? It involves divvying up investments between taxable and retirement accounts. If investments generate large annual tax bills—think taxable bonds and actively managed funds—we’ll typically want to hold them in a retirement account.

Jonathan’s advice is the traditional advice. Put your taxable bonds, like the Thrift Savings Plan (TSP) F and G funds, into your retirement accounts. This is what I do. My F and G funds are in the TSP, clearly a retirement account, and my international bonds (which they don’t have in the TSP) are in an individual retirement account (IRA).

I don’t own actively managed funds, and I also don’t invest in real estate investment trusts (REITs), although I have in the past and I think about it pretty frequently.

There is another school of thought, though. The White Coat Investor has a different take. You can read about them in his posts entitled My Two Asset Location Pet Peeves and Bonds Go in Taxable!

Of note, just about everyone says to put actively managed funds or REITs in a retirement account, so you won’t find any arguments there.

If you’re really interested in this concept/discussion, the Bogleheads Wiki on tax efficient fund placement is a great read as well.

Military Health System Achievements in 2019 Provide Strong Foundation for Year Ahead

Here’s a link to this article from the Defense Health Agency:

Military Health System Achievements in 2019 Provide Strong Foundation for Year Ahead

Will the Government Ever Get Rid of the “Free Lunch” of the TSP G Fund?

They say there’s no free lunch, but in the Thrift Savings Plan there is a free lunch, and it’s called the G Fund. Will the government get rid of this free lunch?

The G Fund Free Lunch

What is this free lunch? You can read about it on this page in the Rewards section:

The G Fund interest rate calculation is based on the weighted average yield of all outstanding Treasury notes and bonds with 4 or more years to maturity. As a result, participants who invest in the G Fund are rewarded with a long-term rate on what is essentially a short-term security. Generally, long-term interest rates are higher than short-term rates.

The government is paying you a higher interest rate than it should. That is the G Fund free lunch.

Why is the Free Lunch at Risk?

The government periodically considers getting rid of it. For example, you can read about it in this article, which is discussing the President’s FY19 budget plan/request. Here’s the relevant portion:

The plan also proposes reducing the statutorily mandated rate of return for the government securities (G) fund to be based on either the three-month or four-week Treasury bill, at a projected savings of $8.9 billion over 10 years.

“G Fund investors benefit from receiving a medium-term Treasury Bond rate of return on what is essentially a short-term security,” the White House wrote. “The budget would instead base the G-fund yield on a short-term T-bill rate.”

TSP spokeswoman Kim Weaver said changing the G Fund’s yield, which is currently 2.75 percent annually, would have a disastrous effect on participants’ ability to save for retirement. If Congress changed the G Fund to track the three-month Treasury bill, the yield would decrease to 1.46 percent, and for the four-week bill it would drop to 1.43 percent.

“Such a change would make the G Fund inadequate and ineffective from an investment standpoint for TSP participants who are saving for retirement,” Weaver said in an email. “More than 3.6 million TSP participants (69 percent) have all or some of their account balance invested in the G Fund. Of those with money in the G Fund, 2 million (39 percent) hold the G Fund as their sole investment choice.”

For a TSP participant who has just retired and is invested entirely in the L Income Fund, which is designed for people who have begun taking annuity payments, they would run out of money at age 84 instead of the current projected age of 92, Weaver said.

Jessica Klement, staff vice president for advocacy at the National Active and Retired Federal Employees Association, said the change would make G Fund investments “useless” and likely force TSP administrators to divest from it entirely.

“[The new rate] would not even keep up with inflation,” she said. “So if you wanted to keep your money in a mostly secure fund, you would not be getting any return, and you’d actually be losing money. And if you took your money out, there would be no other safe, secure investment for those nearing or in retirement.”

What Does This Mean For You?

Right now, it means nothing. This is all just discussion about something that might happen in the future.

What you do need to understand, though, is that the G Fund serves a specific purpose in your portfolio. As the TSP site says:

Consider investing in the G Fund if you would like to have all or a portion of your TSP account completely protected from loss. If you choose to invest in the G Fund, you are placing a higher priority on the stability and preservation of your money than on the opportunity to potentially achieve greater long-term growth in your account through investment in the other TSP funds.

It is alarming that Ms. Weaver from the TSP said, “Of those with money in the G Fund, 2 million (39 percent) hold the G Fund as their sole investment choice.” Those 2 millions people are sacrificing long-term growth for the safest and most conservative investment available in the TSP.

There’s nothing wrong with that if you’re doing it because you are very conservative, near retirement, or the G Fund serves as the bond portion of a larger, more diversified portfolio that has more risky assets like stocks or real estate.

The sad reality is that most who are solely invested in the G Fund are that way because it used to be the default option for those starting a TSP account, and they never switched it to a more aggressive investment option. Under the new Blended Retirement System, the default investment switched from the G Fund to an age-appropriate Lifecycle fund.

What’s the Bottom Line?

The G Fund gives you a free lunch, paying you a higher long-term interest rate while you are investing in short-term securities. The government periodically talks about getting rid of that free lunch.

If you are invested in the G Fund, make sure you are doing it purposely and are aware of its conservative nature. Its emphasis is on preserving wealth rather than growing wealth.

Check Your Beneficiary Designations

Here’s a tip from one of my favorite blogs and authors, Jonathan Clements from Humble Dollar:

CHECK YOUR BENEFICIARY DESIGNATIONS. Your retirement accounts and life insurance will typically pass to the beneficiaries specified on those accounts, not the people named in your will. If your family situation has changed, or you simply don’t remember who you listed, take a moment to review your beneficiary designations.

Don’t let the ex-spouse get your money when you die! Update your beneficiaries.

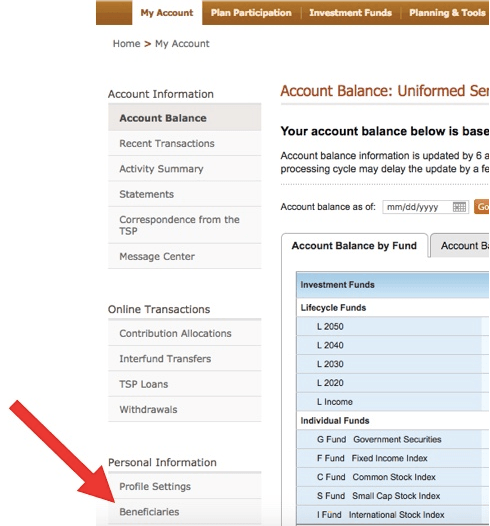

How to See Your Beneficiaries for the Thrift Savings Plan (TSP)

If you log on to the TSP page, you need to click on the link along the lower left, marked by the large red arrow:

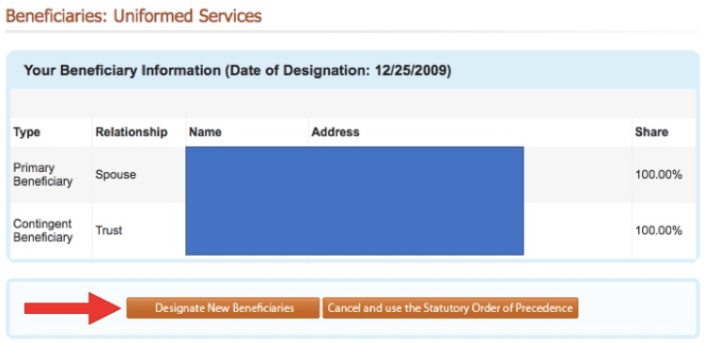

Then you’ll see this, and you can change them at the bottom:

Then you’ll see this, and you can change them at the bottom:

Invest in Your Taxable Account Thoughtfully

Here’s a tip on investing in your taxable account from one of my favorite blogs and authors, Jonathan Clements from Humble Dollar:

INVEST YOUR TAXABLE ACCOUNT THOUGHTFULLY. If you purchase the wrong investments in your taxable account, you may be reluctant to sell, because you’ll trigger capital gains taxes. A good choice: low-cost U.S. and international total stock market index funds, which should be tax-efficient—and which shouldn’t ever lag far behind the market averages.

For those of us in the military, investing in a taxable account comes into play in a few scenarios…

Scenario #1 – You and your spouse (if you have one) have filled your Thrift Savings Plan (TSP) and all other retirement accounts available including IRAs, yet you want to save more for retirement. In this case, you put the rest in a taxable account with the investment company of your choice (Vanguard, Fidelity, Schwab, etc.). This is what I do when all of my retirement accounts are full, and just like Jonathan mentions I invest purely in broad, low-cost index funds at Vanguard. The only taxable holdings I have are the Vanguard U.S. and international total stock market index funds.

Scenario #2 – You are saving for a financial goal that is not related to retirement, such as a downpayment on a home or for a new car. If you’re saving for college, you’d use a 529 plan, but for just about anything else you could use a taxable account. For example, I have my emergency money and extra spending money in a money market fund among my taxable accounts. The alternative to this is to use a bank and invest in a high-yield savings account, a certificate of deposit (CD), or a money market account. Bankrate.com will show you the best rates for each of these reasonable alternatives.

If you are using a taxable account, there are a few things to consider. If you are investing in bonds, you may want to invest in municipal bonds in your taxable account due to the tax benefits. If you are a fan of target date funds, you may not want to use them in a taxable account because the bond portion will kick off income that is taxed at your full marginal tax rate. Most feel that bonds are better placed in a tax-advantaged retirement account unless you are using municipal bonds.