Retirement

Save Some for Your Future Self

Jonathan Clements was a longtime personal finance columnist for The Wall Street Journal, and he offers great advice at the best price you can get (free) on his blog Humble Dollar. Here is one piece of advice from his site:

“SAVE SOME FOR YOUR FUTURE SELF. Looking to lose weight? At restaurants, transfer half your serving to a second plate and ask the waiter to box it up. If the food will make good leftovers, it’s easy to do, because you know you’ll have a treat tomorrow. Want to save more? Think about it the same way—and set aside some of today’s spending money for tomorrow.”

If you are wondering how much to save for your future self, here are a few ways to figure that out.

To start, you have to figure out your gross (pre-tax) income. Include every dollar you get, even the non-taxable allowances. If you’re not sure exactly, take your best guess.

The Minimum

In my opinion, the absolute bare minimum you need to save for retirement is 10% of your gross income. You can include all of your employee contributions in this, like the DoD match in the Blended Retirement System. This doesn’t have to all be your money.

That said, 10% is the minimum. You’ll likely work into your 60s unless you stay in long enough to have a pension.

The Most Common Recommendation

Most commonly people recommend you save 12-15% of your gross income for retirement. If you read this article from Vanguard about how much to save, you’ll see:

If retirement is decades away, setting a specific goal amount is probably unnecessary. For now, focus on:

1. Immediately saving at least enough to get the full match offered by your employer plan, if you have one. This is free money—don’t let it pass you by.

2. Working your way up to 12%–15% of your pay, including any employer match. For example, you could increase your savings rate 1% every year until you reach your target rate. This should get you in the ballpark of what you’ll need.

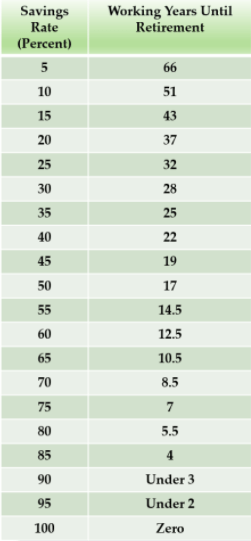

The Early Retirement Recommendation

If you want to achieve financial independence or have the option of retiring early, you probably need to save more than 15%. Mr. Money Mustache’s amazing post about the shockingly simple match of early retirement has this table that shows you how long you’ll need to work based on your savings rate:

The Bottom Line

Start with your gross pay. You need to save a minimum of 10% of that, but you should try to save at least 15%. If you want to achieve financial independence and have the option to retire early or go to part-time work, you need to save more than 15%. I’d recommend 20% or more. I’ve done 30% my whole career.

If you want out help saving for retirement, start here where we discuss it in more depth.

The Basics of Saving for Retirement

Here is a review of the basic principles of investing for retirement:

- Start saving as early as possible because to get rich slowly you need to take advantage of compound interest. Albert Einstein (might have) said, “Compound interest is the eighth wonder of the world. He who understands it, earns it…he who doesn’t pays it.” Compound interest is earning an investment return not just on your initial investment or principle, but also on your previous return. In other words, if you invest $1,000 and earn a 10% return yearly, after the first year you’ll have $1,100. The second year you’ll earn 10% on your initial $1,000, but also on the $100 you earned during the first year, leaving you with $110 of earnings during the second year instead of $100 like the first year. Over a long period of time, this phenomenon greatly increases the amount of money you can accumulate with your investments. Because of this, time spent in the market is much more important than trying to time the market by buying and selling at the right times. The long-term return of the stock market is approximately 9.5% per year. Adjusting for 3% inflation, $1 invested grows to: (Ref: Bogle)

- $1.88 in 10 years

- $3.52 in 20 years

- $6.61 in 30 years

- $12.42 in 40 years

- $23.31 in 50 years

- If you find it difficult to save, set up an automatic investment plan so that the money is automatically removed from your pay and you never get a chance to spend it.

- Investment costs and taxes matter in the long run and will never end; therefore both must be minimized as much as possible. You can minimize both by investing in low-cost stock and bond index funds and maximizing your contributions to tax-preferred retirement accounts.

- Long-term investment in the stock market is the surest way to make your investment grow over time and beat inflation. By owning stocks you own businesses, and the long-term return of these businesses is what will increase your investments and net worth. Trading stocks is not the goal…owning them is.

- As you progress toward retirement, you will decrease your investment risk by decreasing the amount you invest in stocks and increasing the amount you invest in bonds.

- The optimal allocation of investments depends on your age, financial situation, risk tolerance, and how soon you will need to utilize the investment. If you are young, you have longer to ride out the inevitable market swings. The more financially secure you are, the better you can deal with the swings as well. Your asset allocation should also reflect the amount of risk tolerance you have. My opinion is that early in your career you should take as much risk as you can tolerate. If you can’t sleep at night because you are worried about your investments, it is time to dial down the risk, but you should take as much risk as you can up to that point. More risk yields a higher return over the long-term.

- You should utilize dollar cost averaging to decrease your investment risk. Dollar cost averaging is when you purchase the same dollar amount of investments periodically over a long period of time. It provides time diversification, ensuring that you don’t buy all of your investment during a time of temporarily inflated prices. In volatile markets that are going up and down, it will actually increase your investment return because it ensures that you purchase less shares when the investment is expensive, and more when it is cheaper.

- The market will go down, and when it does you need to resist the temptation to sell investments or stop investing. The best time to buy an investment is when it is cheap and you can get the best deal. When the market recovers, which it will, you will reap the rewards. Focus on the long-term and just keep investing.

- Every time you get a raise, bonus, or income tax refund, use it to increase the amount you invest for retirement. You should save at least 15% of your gross or pre-tax income for retirement, but if you want to be rich or retire early you’ll need to save 20-30%.

- How much money will you need to retire? Most retirement planners state that you’ll need approximately 70% of your pre-retirement income to maintain your current standard of living once you retire. This number, though, is heavily dependent on what you consider to be a “good retirement” and what type of a lifestyle you intend to lead. For example, since I save 30% of my gross income for retirement, I’m already living on only 70%, so I highly doubt I’ll need that much when I retire. If you are frugal and pay off your mortgage, you may find that you need as low as 25% of your pre-retirement income to retire comfortably. You won’t be staying in the Ritz Carlton, but there’s nothing wrong with the Hampton Inn.

- There is a lot of uncertainty in life, but the 4% rule is a nice rule of thumb to use when assessing how much money you’ll need to accumulate before you can retire. The 4% rules says that you can take 4% from your retirement savings annually, adjust for inflation each year, and never run out of money. The devil is in the details, but use the 4% rule and assume that you can get approximately $40,000 per year of retirement income from every $1 million you have saved.

- Saving for retirement is your top savings priority, even over funding the college education of your children. You can borrow money to pay for college, but you can’t borrow money to retire.

- You must maximize your contributions to tax-preferred retirement accounts, such as 401(k), 403(b), Simplified Employee Pensions (SEPs), or Individual Retirement Accounts (IRAs) every year. The tax benefits of these plans are staggering over the long-term: (Ref: Malkiel and Ellis)

- If you invest $5,000 per year over 45 years and earn an 8% return with no taxes paid until withdrawal during retirement, you will have a final portfolio value of over $2 million. If you pay 28% taxes at withdrawal, you’d have almost $1.5 million.

- The same savings without the benefit of tax deferral will top out at about $750,000.

- If you work as an independent contractor you have more options than a physician who works as an employee, so hire an experienced tax or health care attorney, accountant, or fee-only financial planner to set up the best options for retirement investments if you are uncomfortable doing this on your own. It is probably going to be easy, though, and you just need to open of a solo/individual 401k with an investment company.

- NEVER use retirement savings for anything other than retirement unless it is absolutely unavoidable. Again…you can’t borrow money for retirement.

References

Bogle, John C. The Little Book of Common Sense Investing: The Only Way to Guarantee Your Fair Share of Stock Market Returns. Hoboken: John Wiley & Sons, Inc., 2007.

Malkiel, Burton and Charles Ellis. The Elements of Investing: Easy Lessons for Every Investor. Hoboken: John Wiley & Sons, Inc., 2013.

Throwback Thursday Classic Post – A Simple and Military Specific Summary of How to Save for Retirement

I’m a huge fam of Jim Lange. He’s a noted expert in financial management, saving for retirement, and estate planning. He’s written a number of books, some of which you can get for free on this page. If I ever move back to Pennsylvania, I’ll probably have him do my estate planning so that I don’t have to worry about anything in retirement.

He sends out a monthly newsletter that I get via snail mail, and it usually has a useful article in it. If you want it, you can get it here.

A previous edition had a section called “Jim’s Point-by-Point Summary of the Whole Retirement & Estate Planning Process.” It was simple but extremely useful. Below in bold are each of the points he lists for people who are still working, which is most of my readership. Let’s take each bolded point and militarize it for you so it is specific to those of us in the military.

Contribute at least the amount to your retirement plan that your employer is willing to match or partially match.

For those under the legacy retirement plan, this is not an option. For those under the new Blended Retirement System (BRS), you need to contribute 5% of your basic pay to the Thrift Savings Plan (TSP) to get the pull 5% DoD match:

You also need to make sure you contribute 5% every month and don’t fill the TSP too early. If you max it out in October, you won’t get a match in November or December.

If you can afford to, contribute the maximum allowed to your retirement plan even if your employer does not match.

This is $19,500 in 2021. You can do an extra $6,500 if you are 50 or over. You can even do more if you are in a combat zone.

Once you have maximized contributions to your plan at work, contribute the maximum you can to an IRA, even if you cannot take a tax deduction on it.

If you are able to fill your TSP account, next you’ll need to open an IRA at an investment firm. Vanguard is the obvious choice due to their across the board low investment fees and unique non-profit structure, but you can do this anywhere (Schwab, Fidelity, etc.).

If you make too much to contribute to a Roth IRA, you just use the back door Roth IRA option.

Consider your personal tax bracket when trying to decide if you should contribute to a Roth or a traditional IRA/retirement plan.

With a traditional plan, you take a tax deduction now and pay taxes later when you take the money out. With a Roth plan you pay the taxes now and the withdrawals are completely tax free.

The general principle is that if you are in a lower tax bracket now than when you are retired, you do the Roth. If you are in a higher tax bracket now, you use the traditional.

No one really knows what the future holds, though, making this decision tough. Here are some resources for you to check out when making this decision:

Traditional and Roth TSP Contributions

Roth vs. Traditional IRAs: A Comparison

Do not take loans against your retirement plan. Allow the tax-deferred or tax-free status of the account to maximize the growth of your money.

While the TSP allows loans, I refuse to link to any information about it. Once you put money away for retirement, you don’t borrow from it unless it is an ABSOLUTE EMERGENCY.

Period.

The Bottom Line

Here are the point-by-point summary of steps Jim Lange suggests you take if you are saving for retirement:

- Contribute at least the amount to your retirement plan that your employer is willing to match or partially match, which is 5% of basic pay in the BRS.

- If you can afford to, contribute the maximum allowed to your retirement plan even if your employer does not match, which is $19,500 in the TSP ($26,000 if you’re 50+).

- Once you have maximized contributions to your plan at work, contribute the maximum you can to an IRA, even if you cannot take a tax deduction on it. Use a back door Roth IRA if you need to.

- Consider your personal tax bracket when trying to decide if you should contribute to a Roth or a traditional IRA/retirement plan.

- Do not take loans against your retirement plan. Allow the tax-deferred or tax-free status of the account to maximize the growth of your money.

3 Things Every Young Medical Student and Physician Needs to Know

I gave this talk at a national meeting in 2017, but here is a written summary of the three things every young medical student and physician needs to know.

1. You can’t control the investment markets, so focus on the two things you can control – investment costs and your asset allocation.

No one, and I mean no one, knows what is going to happen in the investment markets. Study after study have shown that the overwhelming majority of people who try to beat the markets fail. Because of this, you should forget about trying to predict the markets, and focus on things you can control – investment costs and your asset allocation.

All investments have costs, and the impact of these costs on your investment return compounds over time, taking a larger and larger bite out of your investment returns. If you invest $100K for 25 years and earn 6% per year, without costs you’d have $430K. With just a 2% annual cost you wind up with only $260K. That 2% annual cost consumed $170K, almost 40% of your potential investment! (Source: Vanguard.com)

In addition, because they have to overcome higher costs, investments with higher costs lag the performance of similar investments with lower costs. If you look at stock and bond mutual funds in the highest and lowest cost quartiles, you’ll see what I mean:

| Type of Fund | Highest Quartile of Cost | Lowest Quartile of Cost |

| Stock | 6.9% | 7.8% |

| Bond | 4.0% | 4.4% |

If you want to take one step that will guarantee that your costs are among the lowest in the industry no matter what you invest it, you should invest with Vanguard. Vanguard is actually owned by its own investors (you), and they leverage this corporate structure to provide the lowest investment costs across the board. With over $5 trillion (yes, trillion) under management, you can’t go wrong by just investing in Vanguard.

If you can’t invest with Vanguard, perhaps because your retirement plan doesn’t offer Vanguard investments, then you need to get into the weeds on your investment costs. While there are many different potential investment costs, the easiest one to look at is the expense ratio of your potential investments. According to Morningstar.com, the expense ratio is “the annual fee that all funds or ETFs charge their shareholders. It expresses the percentage of assets deducted each fiscal year for fund expenses, including 12b-1 fees, management fees, administrative fees, operating costs, and all other asset-based costs incurred by the fund.”

Wow. That was a mouthful. Bottom line…high expense ratio bad, low expense ratio good. You should be able to find your investments’ expense ratios on your investment website or Morningstar.com.

In addition to investment costs, the other things that you can control is your asset allocation. While there are many asset classes you can invest in, the two most basic are stocks and bonds. Here are some of the returns for stocks and bonds from 1926-2013 in commonly utilized portfolios:

| Annual Return | 50% Stocks & 50% Bonds | 60% Stocks & 40% Bonds | 80% Stocks & 20% Bonds | 100% Stocks & 0% Bonds |

| Highest | 32.3% | 36.7% | 45.4% | 54.2% |

| Average | 8.3% | 8.8% | 9.6% | 10.2% |

| Lowest | -22.5% | -26.6% | -34.9% | -43.1% |

As you can see, the higher your allocation to stocks over bonds, the more risk you are taking and the bumpier the ride. Along the way, though, you have historically been rewarded for this bumpy ride with a higher average annual return. Just like the extra 2% cost that was previously discussed compounds to make a huge difference, so will a small difference in your returns. In other words, the more risk you can take, the more money you will probably end up with.

The application of these principles is that you should take as much risk as you can. In other words, you should invest as much of your portfolio in stocks as you can while still sleeping at night and not lying awake worrying about the stock market’s ups and downs. There will be another market downturn, and when that occurs you need to keep buying stocks because they are on sale, not sell out because you can’t handle seeing your net worth and portfolio value decrease.

Invest as high a percentage of stocks as you can without making the critical mistake of selling stocks during the next market downturn. For me, that has been 100% stocks for the majority of my career, but for some people they’ll panic even at a much lower percentage of stocks. If a 50% stock and 50% bond portfolio is the only one that will keep you from selling during the next market downturn, then that is the right portfolio for you.

If you have been investing for long enough, look at your actual behavior during the 2007-2008 or early 2020 market downturn and what your asset allocation was at the time. In 2007-2008, mine was 100% stocks and I kept on buying. Your allocation and actions will tell you a lot about your own risk tolerance.

In summary, you can’t control the market, so focus on controlling investment costs and your asset allocation.

2. Your savings rate is the most important factor determining your eventual net worth, and it should be at least 20-30% of your gross income.

The most common recommendation you’ll find or hear when it comes to saving for retirement is to save 15% of your gross or pre-tax income for retirement. There is nothing wrong with this recommendation, but built into it is the standard mentality of working until age 65 and then retiring. If you want the freedom to retire early, work as much or as little as you want, and achieve financial freedom/independence, then you will need to save much more than 15%. I’ve saved 30% over most of my adult life, and that’s why I’m writing about personal finance.

If you want to take a look at various saving rates and how they impact your financial life, you’ll want to read the blog post “The Shockingly Simple Math Behind Early Retirement” at MrMoneyMustache.com. There you will find a chart that shows you how many years you will have to work until you can retire based on your savings rate. If you go with the standard 15% savings rate, you’ll have to work 43 years before you can retire. If you go with my 30% rate, you’ll work 28 years. If you manage to save 50%, you can retire in 17 years! The more you save, the earlier you reach financial independence and can work as much or as little as you want. And having a military pension will reduce this even further.

The other standard advice you’ll hear and read is that you’ll spend approximately 80% of your pre-retirement income during retirement. For a physician with a typical high income, that can be a lot of money! You have to realize that 80% is probably high for a physician because after you retire you’ll have greatly reduced expenses. This is because:

- You’ll be in a lower tax bracket.

- You’re no longer saving for retirement.

- You no longer need life or disability insurance.

- You’ve hopefully paid off your mortgage.

- Your kids are out of the house (if you had any).

- You have no more job-related expenses.

- You can give less to charity if you need to.

In the end, you can probably live off of 25-50% of your pre-retirement income, not the standard 80%. This fact can multiply the effect of a higher than normal savings rate.

3. You are your own financial worst enemy.

Unfortunately for us, we engage in self-defeating behaviors all the time, including:

- Assuming too much debt.

- Living above our means in order to keep up with the doctor lifestyle.

- Purchasing too large and expensive a house.

- Purchasing too expensive a car.

- Not maxing out our tax-advantaged retirement account contributions.

Luckily there are some simple rules that, if followed, can keep young physicians and medical students out of trouble. First, realize that anytime you assume debt you are simply borrowing from your future self for current gain. Sometimes that is a good idea, like when you borrow to pay for medical school, but pausing before you assume debt to purchase something can help you out greatly. Getting down to brass tacks, no one really cares what medical school you went to, so you should probably go to the cheapest one you can get into. In addition, no one really cares how large your house is or what kind of car you drive. You think they care, but they really don’t. Don’t try to impress other people.

If you have student debt, you need to get smart about ways to refinance it or get it forgiven with the Public Service Loan Forgiveness Program. Thanks to the Navy and your tax dollars, I never had student debt, so I’m not going to pretend to be the expert on it. If you have student debt, go to WhiteCoatInvestor.com and learn about options to refinance or get your loans forgiven.

When it comes to houses and cars, if you can’t afford the house you are purchasing on a 15-year fixed mortgage then you are probably buying too expensive of a house. Rent until you can put down a larger down payment or look at less expensive houses.

When it comes to cars, you should realize that you can buy a very reasonable used car that is 5-10 years old, plenty nice, and very reliable for much less than a new car will cost. You should make it your goal to pay cash for cars. If you can’t pay cash, then you should purchase a cheaper car. Low or no interest loans are tempting because people think they are getting “free money,” but using “free money” to pay for a depreciating asset (one that declines in value) is not a smart financial move. Your goal should be only to borrow money for appreciating assets (ones that increase in value), like businesses or real estate.

Finally, make sure you maximize your tax advantaged retirement contributions every year. It is one of the few legal ways to hide money from the IRS, and the compound growth year after year is an opportunity you don’t want to miss.

In summary, here are the three things every young physician or medical student needs to know:

1. You can’t control the investment markets, so focus on the two things you can control – investment costs and your asset allocation.

2. Your savings rate is the most important factor determining your eventual net worth, and it should be at least 20-30% of your gross income.

3. You are your own financial worst enemy.

Somebody out there is going to take this advice to heart and get rich. Is it going to be you?

The Military Pension and Retirement Asset Allocation

Jonathan Clements is one of my favorite authors. As a prior financial columnist for the Wall Street Journal and current author of the Humble Dollar blog and money guide, he doles out common sense advice on a regular basis. One of his tenets of personal finance is to take a holistic approach to your financial life and include everything you’ve got and will receive when deciding on your asset allocation and risk tolerance.

In 2017, he published a blog post discussing how he values future income, Social Security, and pensions. If you stick around the military long enough to get an inflation-adjusted pension, his approach and the security of the pension would allow you to take on a lot of additional risk, more than many traditionalists would recommend. He and I discussed this very issue in the comments section, so do me a favor and read the post.

My comments to him were:

I am a huge fan of your writing AND the beneficiary of an inflation adjusted pensions if I stay in for 20 years, which is quite valuable. You advocate for including the value of social security (SS) and pensions in your overall asset allocation, but the other side of the camp would argue you should not because you can’t rebalance with SS or pensions. The present value of SS and an inflation adjusted military pension can be quite large, and with your approach would likely represent all of a person’s “bond holdings” unless they were very wealthy or extremely conservative.

For example, if a retired military member wanted to generate $75K in annual income, and was going to get $15K/year from SS and $35K/year from his/her military pension, that would leave $25K/year they need to generate income from. Using the 4% rule, they would need about $625K in investments.

If they wanted a 50/50 stock/bond portfolio, using your approach they might own all $625K in stocks. They’d have nothing to rebalance with when the stock market soared.

Using the argument of those who don’t agree with your way of allocating assets and don’t include SS/pensions as bond-like, they’d own $312.5K of bonds and $312.5K of stocks. They could easily rebalance.

Does the case of someone with a very large, inflation adjusted military pension change they way you’d approach retirement asset allocation?

His reply:

What you describe falls firmly into the category of “nice problems to have.” If I had $50k guaranteed every year and needed another $25k from investments, I’d set aside $125k of my $625k portfolio in cash and short-term bonds, to cover the next five years of required portfolio withdrawals. And then I’d probably put much or all of the remaining $500k in stocks.

How to Easily Figure Out the Dollar Value of Staying In vs Getting Out of the Military

Here is a table from the 2019 Statistical Report on the Military Retirement System:

Just by looking at this table, you can very easily learn a few things including:

- The dollar value of staying in for 20+ years and receiving a retirement pension.

- The incremental value of staying on active duty for additional years once you are retirement eligible.

The Dollar Value of a Military Pension

Let’s say you are an O-4 who has the option of resigning/separating at the 12 year mark. You think if you stayed in until 20 years you could make O-5, but you’re not sure just how valuable that military pension really is. You can figure that out by looking at the table above, and you can see that a 20 year O-5 pension has a dollar value of $1,458,837. You can reduce this value by about 20% ($1,167,070) if your are in the Blended Retirement System and would only get 80% of the full pension. That is what you’d be giving up by getting out at the 12 year mark as an O-4 and not staying in long enough to get the pension.

The Value of Staying Additional Years Once You are Retirement Eligible

Let’s say you are a 20 year O-5 who is weighing an extra 4 year commitment, and you think you could make it to O-6 if you stayed until 24. What is the dollar value of sticking around when it comes to your retirement pension?

We already mentioned that a 20 year O-5 pension was worth $1,458,837. If you stayed in another 4 years and made O-6 the value of your pension would have increased by $526,879 to $1,985,716, an average of $131,720 per extra year you stuck it out.

The Bottom Line

There are a lot of factors to consider when you are making the decision to stay in or get out, but by looking at the table above you can pretty easily quantify dollars values associated with:

- Staying in for 20+ years and receiving a retirement pension.

- The incremental value of staying on active duty for additional years once you are retirement eligible.

The Easiest Way to Get Rich in the Military – Take the Leap and Just Stay In

Because of the value of the government pension, staying in is the easiest way to get rich. And when I say “staying in” I’m not talking about becoming the Surgeon General of the Navy. I’m talking about doing a reasonable job as an officer for at least 20 years. Let’s look at the most common scenario.

A 20-Year O5

Let’s assume that an officer was commissioned in 1999 at the age of 22, and stayed in 20 years until 2019, making it to O-5. According to the DoD actuarial tables, the value of a 20-year O-5 pension is $1,458,837.

Yes, just by staying in for 20 years you are already a millionaire and you’re only 42 years old. Depending on how much you saved in the TSP, you could be a multi-millionaire or darn close to it.

You Can’t Screw It Up

People try to time the stock market, wind up buying and selling investments at the wrong time, take loans from their retirement accounts, don’t save/invest enough, and find all manner of ways to screw their finances up. But when it comes to the military pension and the value it provides, the best thing about it is that you can’t screw it up.

Stay in for 20+ years…do a reasonable job and promote at the normal times…you’re rich. It’s that easy.

Throwback Thursday Classic Post – What is the Obligation for Accepting Promotion? What if You Don’t Want the Promotion?

Question: What is the obligation for accepting promotion?

Answer: There is no obligation if you end up resigning. If you want to retire, though, the additional obligation is:

- 2 years for LCDR

- 3 years for CDR and CAPT

This can all be found on page 5 of OPNAVINST 1811.3A. Or you can read one of my other posts called “You were accepted for promotion to O5 or O6 – should you accept it?” where I break it all down for you.

Question: What if you want to decline the promotion? The promotion NAVADMIN that comes out every month tells you how to decline it in paragraph 2:

2. If a selected officer does not decline promotion in writing prior to the

projected date of rank (noted above in paragraph 1), that officer is

considered to have accepted the promotion on the date indicated. An officer

who chooses to decline promotion must submit the declination in writing to

COMNAVPERSCOM (PERS-806) within 30 days of the release of this

NAVADMIN. Limited duty officers declining appointment to lieutenant will be

reverted to enlisted status within 90 days of projected promotion date.

Skillbridge Program for Separating Service Members

The DoD SkillBridge program provides an opportunity for Service members to gain valuable civilian work experience through specific industry training, apprenticeships, or internships during the last 180 days of service. SkillBridge connects Service members with industry partners in real-world job experiences.

For Service members SkillBridge provides an invaluable chance to work and learn in civilian career areas. For industry partners SkillBridge is an opportunity to access and leverage the world’s most highly trained and motivated workforce at no cost. Service members participating in SkillBridge receive their military compensation and benefits, and industry partners provide the training and work experience.

SkillBridge is an excellent benefit for installation and Unit Commanders who have members nearing military separation. SkillBridge can help Service members bridge the gap between the end of service and the beginning of their civilian careers. Commanders can greatly ease this transition to civilian life by supporting their reports’ interest in SkillBridge. When mission permits, Commanders who support SkillBridge participation are helping their personnel transition more seamlessly from service to a civilian career with a trusted employer.

Separating Service members can be granted up to 180 days of permissive duty to focus solely on training full-time with approved industry partners after unit commander (first O-4/Field Grade commander in chain of command) provides written authorization and approval. These industry partners offer real-world training and work experience in in-demand fields of work while having the opportunity to evaluate the Service member’s suitability for the work.

The link below will take you directly to the DOD SkillBridge webpage, which will provide you with additional information:

https://dodskillbridge.usalearning.gov/program-overview.htm

**NEW** Amazon is now officially a DoD SkillBridge provider, meaning they can take in active duty military members into Amazon for internship opportunities and upon successful completion they can extend them full time offers to become Amazonians! Military Affairs is launching internship opportunities this year in select operation sites. Service members can apply now for these opportunities by typing in “Amazon Military SkillBridge” on amazon.jobs and they are hosting a webinar today with more information about this cohort (flyer attached). Please spread the word to your active duty friends and family members. If they have any more questions about Amazon Military SkillBridge (AMSB), feel free to direct them to militaryskillbridge@amazon.com.

A short video about this cohort:

Military Times 2020 Guide to Military Benefits

Here’s a link to this on-line guide that covers Basic Pay, BAH, retirement, family support, VA loans, TRICARE, and educational benefits. It is a great resource if you have questions about how something works:

{kind=link}