Author: Joel Schofer, MD, MBA, CPE

Asset Allocation

Jonathan Clements was a longtime personal finance columnist for The Wall Street Journal, and he offers great advice at the best price you can get (free) on his blog Humble Dollar. Here is one piece of advice from his site:

“ASSET ALLOCATION. This is a portfolio’s split between the four asset classes: stocks, bonds, cash investments like savings accounts and money market funds, and alternative investments like gold, real estate and hedge funds. It’s arguably the most important decision an investor makes. The more a portfolio has in stocks, the greater its volatility—but the higher its expected return.”

Like Jonathan mentions above, this is arguably the most important decision you make. Once you make the decision, it solves many of your investing dilemmas.

For example, many people think that the stock market is an overvalued bubble about to burst. What do you do at the end of this month when you are looking to invest some money? You look at your desired asset allocation and invest in whatever is underweighted. If nothing is underweighted, you invest in them proportionally and consistent with your asset allocation. If your desired allocation is 80% stocks and 20% bonds, you invest 80% in stocks and 20% in bonds.

The bubble bursts tomorrow and it’s the end of the month. What do you do? Again, you look at your desired asset allocation and invest in whatever is underweighted (likely stocks).

Picking an appropriate asset allocation and sticking to it simplifies your financial life and solves mental dilemmas.

If you want some help, here’s my take on how to select an appropriate asset allocation. You can also find a discussion about it in our 6th step to financial security – Invest in Stock and Bond Index Funds or ETFs.

Multiple Leadership Positions at Walter Reed

Walter Reed has three board positions available in the summer of 2021.

PDs are here:

Anyone who applies need PERS clearance to do so from their Detailer.

Navy Times – Sailors Will Now Have an Alternative Rank Insignia Option for Navy Woodland Cammies

Here’s a link to this article:

Sailors Will Now Have an Alternative Rank Insignia Option for Navy Woodland Cammies

Here’s a link to the NAVADMIN:

https://www.public.navy.mil/bupers-npc/reference/messages/Documents/NAVADMINS/NAV2020/NAV20292.txt

2021 TSP Contribution Limits Unchanged and Finance Friday Articles

Here’s a link to the TSP article:

TSP Investment Limits to Be Unchanged for 2021

Here are this week’s articles:

- 7 Reasons Not to Use a 100% Stock Portfolio

- Are We Trading Our Happiness for Modern Comforts? As society gets richer, people chase the wrong things.

- Doing Good

- Look Under the Hood (note that Tesla is included in the TSP S fund)

- The Importance of Diversification in Achieving Long-Term Goals

- The Taxman Cometh

- Why You Shouldn’t Max Out Your 401(k)

Throwback Thursday Classic Post – Thrift Savings Plan Fund Deep Dive – The S Fund

There are only five investments available in the Thrift Savings Plan (TSP), so let’s take a detailed look at them one at a time. In this post we’ll cover the S Fund. You can combine the S Fund with the C Fund to invest in the entire US stock market.

Inception Date

1 MAY 2001

Fund Management

The Federal Retirement Thrift Investment Board currently contracts BlackRock Institutional Trust Company, N.A. (BlackRock) to manage the S Fund assets. The S Fund remains invested regardless of the performance of the securities markets or the overall economy.

Investment Strategy

The S Fund is invested in a stock index fund that invests in small to medium-sized U.S. companies that are not included in the C Fund. The S Fund’s objective is to match the performance of the Dow Jones U.S. Completion TSM Index, which means that when you combine the S Fund and C Fund you are investing in the entire US stock market. Also, some of the money in the S Fund is temporarily invested in the G Fund and earns the G Fund return.

The S Fund is a passively managed fund that remains invested according to its indexed investment strategy regardless of stock market movements or general economic conditions.

What is the Risk?

Your investment in the S Fund is subject to market risk because the prices of the stocks it invests in rise and fall. You are also exposed to inflation risk, meaning your S Fund investment may not grow enough to offset inflation.

What is the Benefit?

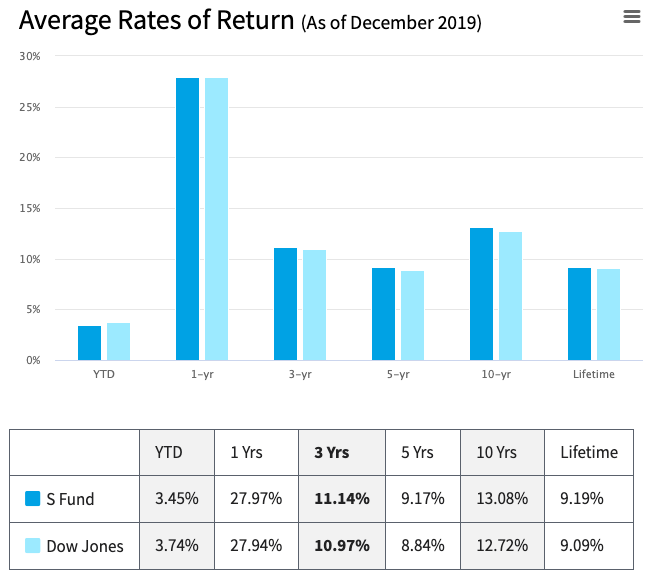

Historically, this increased risk has been rewarded with an increased return. It offers the opportunity to experience gains from equity ownership of small and medium-sized US company stocks. Here is all the performance data as of 24 OCT 2020:

Types of Earnings

The S Fund changes in value as the market price of its stocks change. In addition, the S Fund makes money for its investors when those stocks pay dividends. Unlike a traditional mutual fund, though, income from dividends is included in the share price calculation. It is not paid directly to participants’ accounts.

It also makes some money on interest on short-term investments and securities lending income.

BlackRock credits interest and dividend income each business day. This income is then reflected in the TSP share prices.

Share Price Calculations

The value of your account is determined each business day based on the daily share price and the number of shares you hold. At the end of each business day, after the stock and bond markets have closed, the total value of the funds’ holdings (net of accrued administrative expenses) is divided by the total number of shares outstanding to determine the share price for that day. The daily change in TSP share prices reflects all investment income (interest on short-term investments, dividends, capital gains or losses, and securities lending income) net of TSP administrative expenses.

Expenses

The net expenses paid by investors is 0.042% or 4.2 basis points, which like all the TSP funds is ridiculously low and is a major benefit of the TSP. It cost $0.42 for each $1,000 invested.

How Should I Use the S Fund in my TSP Account?

The S Fund can be useful in a portfolio that also contains stock funds that track other indexes such as the C Fund (which tracks an index of large U.S. company stocks) and the I Fund (which tracks an index of international stocks). The C, S, and I Funds track different segments of the overall stock market without overlapping. This is important because the prices of stocks in each market segment don’t always move in the same direction or by the same amount at the same time. By investing in all segments of the stock market (as opposed to just one), you reduce your exposure to market risk.

The S Fund can also be useful in a portfolio that contains bonds. Again, it is because the prices of stocks and bonds don’t always move in the same direction or by the same amount at the same time. So a retirement portfolio that contains a bond fund like the F Fund, along with other stock funds, like the C and I Funds, will tend to be less volatile than one that contains stock funds alone.

Advice from My Favorite Short Investing Book

Here is what my favorite investing book, The Elements of Investing: Easy Lessons for Every Investor, says about small and mid-cap funds like the S Fund:

The S&P 500 [C Fund in the TSP] represents only about 70 percent of the total value of all stocks traded in the United States. It excludes the 30 percent made up of smaller companies [which are in the S Fund], many of which are the most entrepreneurial and capable of the fastest future growth.

If you want to invest in the entire US stock market, you just combine the C Fund with the S Fund in a 3:1 ratio. To see how I use the S Fund, read the Crush the TSP series.

One Navy Medicine – SG’s Message from Tidewater

Esteemed Colleagues,

Last week I had the pleasure of visiting our One Navy Medicine Team in the Tidewater area and it is very rewarding and encouraging to see the Fleet side, NMRTC/NMC Portsmouth and Navy and Marine Corps Public Health Center all working together as One Navy Medicine to ensure the readiness of our warfighters. Take a look at the attached short video for a look at an example of our new Platforms headed to the fleet in the next few years!

MilSuite Link (Gov Computers)– https://www.milsuite.mil/video/36662

YouTube Link – https://youtu.be/5kKt2_aY_9A

Transcript here (If you don’t have the bandwidth for video):

SG Sends

V/r,

Bruce L. Gillingham, MD, CPE, AOA

RADM, MC, USN

Surgeon General, U.S. Navy

Chief, Bureau of Medicine and Surgery

Fidelity’s Free Mutual Funds

If you read financial blogs or follow the financial news, you’ve probably read multiple articles about Fidelity’s free index mutual funds. Yes…completely free with a 0% expense ratio.

What does this mean for the military investor? Let’s take a look…

What Happened?

All of the major investment companies – Fidelity, Schwab, and Vanguard – are competing for your business by lowering their investment fees. Vanguard has been the low cost leader and used that focus and their unique non-profit structure to become the largest investment company, managing over $5 trillion. For comparison, Fidelity oversees $2.5 trillion. Yes, TRILLION.

Vanguard’s mantra emphasizes the following central tenets of investing:

- The lower your investment fees, the more of the investment return you get to keep.

- Costs last forever.

- You should invest with low cost, broadly diversified index funds.

As you might have guessed, this is what I do at Vanguard and with my Thrift Savings Plan (TSP) accounts.

In 2018, Fidelity announced that they were offering two new mutual funds at no cost – free – to investors with no investment minimums. The funds are the:

- Fidelity ZERO Total Market Index Fund (FZROX) – a diversified US stock index fund

- Fidelity ZERO International Index Fund (FZILX) – a diversified international stock index fund

Everyone was waiting for one of these investment giants to offer free mutual funds. Fidelity became the first.

Fidelity Mania

When this announcement came out, there were countless news articles and blog posts about the free funds. People have been clamoring to switch to Fidelity funds, but a closer look will show you that switching to Fidelity is not guaranteed to be a good move or even what most people trying to minimize their fees should do.

They’re Free! Why Not Switch?

First, Fidelity is not a stupid company. There is no such thing as a free lunch (except for the Thrift Savings Plan G Fund), and they are going to make money from their customers somehow. One way would be by luring you to Fidelity for these free funds, but charging you more on other investments. As the author of this article on Morningstar stated:

But, ultimately, no companies toil for free. What they give away in one place, they recoup in another.

They’ll make up the difference with other funds or brokerage services.

In addition, The White Coat Investor wrote one heck of an article that deep dives on expense ratios and the new Fidelity funds. In it he points out that when you look at equivalent Vanguard, Schwab, and Fidelity funds you’ll see that Vanguard seems to win even with slightly higher expenses and they have a tax efficiency advantage that Schwab and Fidelity don’t have. As he notes:

It just turns out that Vanguard is better at indexing than Fidelity and Schwab. Is that really a surprise to anyone?

I hate to reinvent the wheel, so those interested in the details should really read his article.

What Does This Mean for Investors?

If you are already a Fidelity investor, their drive to compete with Vanguard is going to give you some really useful low cost investment opportunities.

If you are not already a Fidelity investor, realize that if you sell any investments in a regular taxable account (outside of a tax advantaged retirement account like a 401k, IRA, or the TSP), you will have to pay taxes on any capital gains you have. Unless selling won’t generate any taxes (you don’t have any gains) or what you are invested in is an extremely poor choice, I wouldn’t give Uncle Sam some of your money just to save a few hundredths of a percentage point on your expense ratio.

Here’s a good quote from another Morningstar article about the new Fidelity funds that demonstrates how little of a difference these small percentages can have on your bottom line:

To illustrate the modest stakes for your portfolio, let’s look at the growth of a $10,000 investment in Fidelity Total Market Index (FSKAX), Schwab Total Stock Market Index (SWTSX), and Vanguard Total Stock Market Index (VTSAX). Over the years, the three have changed leadership on fees, and investment minimums have changed, too. For the past 10 years, $10,000 in Vanguard Total Stock Market Index would have grown to $28,520, while the Schwab fund would have grown to $28,460 and the Fidelity fund to $28,350. And the differences at times were greater than they are today. So, keep costs low and save as best you can, but don’t worry too much about a couple of basis points.

In addition, you can’t underestimate the benefit of simplicity when it comes to your investment portfolio. I had the TSP and Vanguard. That was it. Then my wife changed employers and now we have a less than optimal 401k with Fidelity that drives me nuts.

While I keep track of everything with a Google spreadsheet and that makes it pretty easy, having yet another website (Fidelity) I have to log in to when I want to make changes is kind of a pain. Don’t underestimate the peace of mind that comes with simplicity, and adding Fidelity to the mix for a few basis points might not be worth the hassle.

If you are just starting out as an investor or you haven’t invested outside of the TSP yet, just realize that you really can’t go wrong with Fidelity, Schwab, or Vanguard as long as you focus on their low cost funds. At Vanguard, all the funds are low cost, so that simplifies your investing life, but Schwab and Fidelity are fine as well.

What’s the Bottom Line?

- If you’re already invested with Fidelity, enjoy the new free funds and use them for your US and international stock investments.

- If you haven’t picked an investment company outside the TSP yet, Fidelity is certainly one to consider but I’d still go with Vanguard if it was up to me.

- You probably should not switch from another company just for free funds, and certainly should not sell anything that would trigger a capital gain just to switch.

The White Coat Investor summarized the strategy you’d employ no matter what company you pick in his article about the Fidelity funds:

There is no new investing strategy going on here. It’s the same old, same old investing strategy – buy all the stocks, hold them, keep your costs and taxes down, and in the long run, your money grows at the same rate as the market and if you save enough, you become financially independent