personal finance

Finance Friday Articles

Here are my favorites this week:

Are You Leaving Money On The Table?

Making the Call – Roth vs Traditional

The Ultimate Productivity Hack is Saying No

Here are the rest of this week’s articles:

6 TRICARE Resources You Might Not Know About

All-Time Highs Are Both Scary & Normal

A Primer on Real Estate Professional Status for Physicians

Beyond Fee-Only: 7 Things to Know About the Advice-Only Model

Bull Markets Last Much Longer Than You Think

How to Fast FIRE Your Way to Generational Wealth – Part I

How We Went From Full-Time Physicians to Semi-Retired MDs

How Your TRICARE Costs Will Change in 2020

I Made $15 Million Before I Was 30, And It Wasn’t As Awesome As You’d Think

Make these Five Tax Moves Before December 31st

Six Principles of Asset Location

Smart Career Alternatives and Retirement for Physicians

Strategies To Consider When Building An Effective Retirement Income Plan

Student Loan Advice: 7 Rules of Thumb

The Code, Conflicts, and Client Interest

There’s Always a Bear Market Somewhere

What Causes Physician Burnout? The Medscape Survey

Where Have All The Stock Market Returns Come From This Decade?

Why Opportunity Fund Investors Shouldn’t Settle for High Fees

Why the best person to give you money advice may NOT be an accountant or financial adviser

A Simple and Military Specific Summary of How to Save for Retirement

I’m a huge fam of Jim Lange. He’s a noted expert in financial management, saving for retirement, and estate planning. He’s written a number of books, some of which you can get for free on this page. If I ever move back to Pennsylvania, I’ll probably have him do my estate planning so that I don’t have to worry about anything in retirement.

He sends out a monthly newsletter that I get via snail mail, and it usually has a useful article in it. If you want it, you can get it here.

A previous edition had a section called “Jim’s Point-by-Point Summary of the Whole Retirement & Estate Planning Process.” It was simple but extremely useful. Below in bold are each of the points he lists for people who are still working, which is most of my readership. Let’s take each bolded point and militarize it for you so it is specific to those of us in the military.

Contribute at least the amount to your retirement plan that your employer is willing to match or partially match.

For those under the legacy retirement plan, this is not an option. For those under the new Blended Retirement System (BRS), you need to contribute 5% of your basic pay to the Thrift Savings Plan (TSP) to get the pull 5% DoD match:

You also need to make sure you contribute 5% every month and don’t fill the TSP too early. If you max it out in October, you won’t get a match in November or December.

If you can afford to, contribute the maximum allowed to your retirement plan even if your employer does not match.

This is $19,500 in 2020. You can do an extra $6,500 if you are 50 or over. You can even do more if you are in a combat zone.

Once you have maximized contributions to your plan at work, contribute the maximum you can to an IRA, even if you cannot take a tax deduction on it.

If you are able to fill your TSP account, next you’ll need to open an IRA at an investment firm. Vanguard is the obvious choice due to their across the board low investment fees and unique non-profit structure, but you can do this anywhere (Schwab, Fidelity, etc.).

If you make too much to contribute to a Roth IRA, you just use the back door Roth IRA option.

Consider your personal tax bracket when trying to decide if you should contribute to a Roth or a traditional IRA/retirement plan.

With a traditional plan, you take a tax deduction now and pay taxes later when you take the money out. With a Roth plan you pay the taxes now and the withdrawals are completely tax free.

The general principle is that if you are in a lower tax bracket now than when you are retired, you do the Roth. If you are in a higher tax bracket now, you use the traditional.

No one really knows what the future holds, though, making this decision tough. Here are some resources for you to check out when making this decision:

Traditional/Roth TSP Comparison Matrix

Roth vs. Traditional IRAs: A Comparison

Do not take loans against your retirement plan. Allow the tax-deferred or tax-free status of the account to maximize the growth of your money.

While the TSP allows loans, I refuse to link to any information about it. Once you put money away for retirement, you don’t borrow from it unless it is an ABSOLUTE EMERGENCY.

Period.

The Bottom Line

Here are the point-by-point summary of steps Jim Lange suggests you take if you are saving for retirement:

- Contribute at least the amount to your retirement plan that your employer is willing to match or partially match, which is 5% of basic pay in the BRS.

- If you can afford to, contribute the maximum allowed to your retirement plan even if your employer does not match, which is $19,500 in the TSP ($26,000 if you’re 50+).

- Once you have maximized contributions to your plan at work, contribute the maximum you can to an IRA, even if you cannot take a tax deduction on it. Use a back door Roth IRA if you need to.

- Consider your personal tax bracket when trying to decide if you should contribute to a Roth or a traditional IRA/retirement plan.

- Do not take loans against your retirement plan. Allow the tax-deferred or tax-free status of the account to maximize the growth of your money.

Finance Friday Articles

Here’s an article about the upcoming change in the TSP I Fund. They are adding emerging markets like China to the I Fund’s international stock holdings:

Viewpoint: Let’s Keep a Level Playing Field for TSP Investors

Here are my favorite articles of the week:

Step By Step Guide to Opening a Brokerage Account

The 1% Rule and How It Can Save You Time When Evaluating Rental Properties

Here are the rest of this week’s articles:

10 Questions to Ask Yourself About Your Investments

Conflicts of Interest: Are You Getting Good Advice?

Creating a Dynasty: Building Family Wealth Across Generations

How much can we earn in retirement without paying federal income taxes?

If It Doesn’t Cash Flow, Don’t Buy It

Missing the Target with Target Date Funds

Monte Carlo Analysis: Understanding What You’re Dealing With

Oldies But Goodies – Financial Books You Should Read

The End of the Year Unwanted Payday

This Anesthesiologist Retired At 43 By Avoiding The Normal Traps That Trip-Up Doctors’ Savings

This Law Lowers Interest Rates for Active Duty Servicemembers

Throwback Thursday Classic Post – The $121,500+ Guest Room

(This is one of the most popular articles I’ve ever written, and I’m on my 3rd exchange student, so this room has cost me way more than indicated in the title.)

I have a wife, two children, two dogs and the need for three bedrooms and two bathrooms. In March 2015 I purchased what I consider to be a modest 4 bedroom, 3.5 bath, 3000 square foot house in a nice neighborhood with quality public schools. The 4th bedroom is largely unnecessary, but like many people we occasionally have visitors and feel that it is nice to offer them a bedroom as opposed to a hotel. This is the story of how that 4th bedroom cost me over $100,000, far more than it would cost to provide our visitors with a hotel room…a REALLY NICE hotel room.

The Guest Room

The guest room and its accompanying full bathroom are approximately 600 square feet. The house sold for $140/square foot, meaning that this extra room and bathroom cost me $84,000. Where I live, you can get a decent hotel room for $100/night. In other words, I could have purchased 840 nights in a hotel room for any guests we have and I don’t think we’ll ever have 840 guest-nights unless we stay in this house for a very, very, long time. In addition, we have a quite comfortable queen size Lazy Boy sleeper couch that could have substituted for the guest room.

Running total: $84,000

The HVAC Incident

“The way they installed this, I don’t even think I can fix it.” That is not what I wanted my HVAC repair man to say, but that is what he said. The guest room did not have its own HVAC zone and because it is above the garage and the insulation is not what it could be, the guest room is always too hot or too cold. And what’s the point of a nice guestroom if it’s not comfortable? After spending $5,000, the guest room had its own wall mounted HVAC unit and zone.

Running total: $89,000

The Exchange Student

Since we have an $89,000 extra room with a bathroom and its own HVAC, we are hosting a Spanish exchange student during the upcoming school year. Hosting an exchange student will likely be a great experience for us all, as I assume it will expand our horizons and hopefully forge a lasting relationship with someone for us to visit in Spain.

I suspect this student, like most humans, will eat and drink and cost some money, so I’m adding that to the running total.

Running total: $89,000 plus whatever a 16-year-old boy eats and drinks during a school year.

Despite the fact that he is of driving age, he is not allowed to drive in the US. This, of course, led to…

The Manny Van

Sometime in August, I will have a wife, two kids, two dogs, and an exchange student. It is (was) going to be tough to get around and do the traveling we’d like to do in our Toyota Prius and Ford Fusion Hybrid. Having a 12, 15, and 16-year-old in the back seat, while technically feasible, was not going to be fun for anything other than the shortest of trips. Plus, we like to bring the dogs.

Enter the $32,500 2015 Toyota Sienna minivan, which I like to call the “manny van” when I’m driving it. I can now haul all living beings for whom I am responsible in the manliest of vans.

Running total: $121,500 plus whatever a 16-year-old boy eats and drinks in a school year

The Moral of the Story

One of the classic financial mistakes that almost all physicians make (including me apparently) is that they spend too much money, buying too expensive a car and too large of a house. Sometimes something as simple as wanting a guest room can lead to unintended and expensive consequences. If we didn’t have a guest room, I would probably have an extra $100,000 and I wouldn’t be driving a “manny van”.

Do the TSP Target Date Funds Miss the Mark?

Blooom is an on-line financial advisory service that will manage your Thrift Savings Plan (TSP) and other retirement accounts for only $10/month. On another blog I wrote an article about them and some readers got into a Twitter dialogue with them. During this dialogue it was suggested that an investor doesn’t need to pay $10/month for an advisor because you can always just use target date funds if you don’t want to manage your investments yourself. Blooom’s response pointed to a blog post of theirs about target date funds and all the problems associated with them. Let’s take a look at their post and see if the points they raise are valid when compared to the TSP’s target date funds, the Lifecycle Funds.

What’s a Target Date Fund?

According to Investopedia, a target date fund is:

A fund offered by an investment company that seeks to grow assets over a specified period of time for a targeted goal. Target-date funds are usually named by the year in which the investor plans to begin utilizing the assets. The funds are structured to address a capital need at some date in the future, such as retirement. The asset allocation of a target-date fund is therefore a function of the specified timeframe available to meet the targeted investment objective. A target-date fund’s risk tolerance become more conservative as it approaches its objective target date.

The Lifecycle or L Funds are the TSP’s version of target date funds. You can read my deep dive on them if you like for more information.

Are the Lifecycle Funds Too Conservative?

Yes, in my opinion, the L Funds are too conservative when compared to other target date funds and the fact that many of us will have an inflation-adjusted pension. To compensate you can always just pick a L fund that targets a later year. When I used the L funds in my TSP, that is what I did.

For example, if you want to retire in or around 2030 you would normally pick the L 2030. Instead you could pick the L 2040 or L 2050 to get more aggressive. That said, the most aggressive you can get with the L Funds right now is the L 2050, which is 82% stocks and 18% bonds. If you want less than 18% bonds, you can’t do that with any of the current L funds.

Do the Lifecycle Funds have High Expense Ratios?

This is a definitive no. While other target date funds can have high expenses, the L funds are composed of funds with the lowest expenses you will find anywhere. You probably cannot find a target date fund with lower expenses than the TSP L Funds.

Do the Lifecycle Funds Lack Personalization?

Yes, they do. There’s no way around this one. You can personalize them a little bit by adjusting the target date you invest in, as described above, but they are by definition standard for all investors.

I would argue that these standard asset allocations are good enough for just about everyone to come up with a reasonable investment plan. If you want a personalized plan, though, you may have to get some help or use a financial advisor.

The Bottom Line – Do the L Funds Miss the Mark?

I think it depends. They are definitely low cost, so they hit the target there. I do think that they are too conservative, but as long as you are OK with a minimum bond allocation of 18% you can just adjust that by using a fund with a target date that is further off. They are definitely not personalized, but I don’t think they need to be. The asset allocations they use would do for 99% of the people investing, including myself.

Finance Friday Articles

My favorite article this week:

Pizza Delivery is for Millionaires

Here are the rest of this week’s articles:

Be Proactive, Not Reactive When It Comes To Creating Passive Income

Don’t Compare Your Finances/Investing to Others

How Much Money Does a Doctor Need to Retire?

Maintaining a Small RV for Retirement Travel

Should You Turn Your Starter-Home into a Rental?

The Value Proposition of a Real Estate Access Fund

Updated Trinity Study Results for 2019 – More Withdrawal Rates!

2 Important TSP Changes and Finance Friday Articles

This week I’d like to highlight the 2020 TSP contribution limits, which will be $19,500 for most of us, as well as the instructions for enabling 2-factor login, which will be required as of 1 DEC:

TSP Contribution Limits for 2020

TSP 2-Factor Login Instructions

Here are the rest of the articles:

2020 Tax Brackets, Standard Deduction, and Other Changes

6 Bare Minimum Tasks to Fix Your Finances

Are Real Estate Investments Resistant to Inflation?

Bernstein Says Stop When You Win The Game

Financial Burdens and Physician Burnout

How to manage money for financial success in the U.S. military

How to Think About Money: A Physician on Fire Review

Into a Cloud – Letters from a Downed World War II Pilot

Lessons Driving an $800 Car Can Teach Your Kid

Non-Intuitive Lessons From the Man Who Solved the Market

Student Loan Planner Reviews: Honest Opinions from Three Former Clients

The 3 benefits of charitable giving

The Price of US Stocks and Signal Failure

Trends That Matter in Asset Management

TURNKEY RENTALS DON’T HELP YOU ACHIEVE FAST FIRE

Using Your Estate Plan to Have a Graceful Exit

What does buying a new car really cost over the years?

Why are Doctors Burning Out? Three Ways FIRE Can Save Us

Why Timing the Market is a Fool’s Errand

My Investment Portfolio

I write a lot about personal finance. If you are wondering what I’m doing for my own finances, here’s a detailed look at my own portfolio. I’m not going to give you dollar amounts, but percentages. If you want to know the dollar amounts, they can be expressed in one word. I have…enough:

At a party given by a billionaire on Shelter Island, Kurt Vonnegut informs his pal, Joseph Heller, that their host, a hedge fund manager, had made more money in a single day than Heller had earned from his wildly popular novel Catch-22 over its whole history. Heller responds,“Yes, but I have something he will never have . . . enough.”

Assets

My financial assets from largest to smallest include: (all percentages are rounded to the nearest whole percentage)

- 24% – My taxable mutual funds, which is where I put our retirement savings when I fill our retirement accounts. It is currently invested in:

- 56% – Vanguard Total Stock Market Index Fund Admiral Shares (VTSAX)

- 37% – Vanguard Total International Stock Index Fund Admiral Shares (VTIAX)

- 7% – Vanguard Prime Money Market Fund Investor Shares (VMMXX)

- 21% – My Thrift Savings Plan (TSP) – Currently invested in this proportion:

- 91% – US stocks

- 75% – C Fund

- 25% – S Fund

- 1% – International stocks (I Fund)

- 9% – US bonds split evenly between the G Fund and F Fund

- 91% – US stocks

- 15% – My paid off house.

- 12% – My wife’s TSP, which is invested 100% in US bonds with a 50/50 split of the G and F Funds.

- 12% – My wife’s Roth IRA, which is invested in:

- 53% – Vanguard Total International Stock Index Fund Admiral Shares (VTIAX)

- 47% – Vanguard Total International Bond Index Fund Admiral Shares (VTABX)

- 9% – We have two 529 plans with Vanguard invested in their aggressive age-based portfolio.

- 6% – My Roth IRA, which is 100% invested in the Vanguard Total International Stock Index Fund Admiral Shares (VTIAX).

- 1% – My wife’s individual 401k, which is 100% invested in the Vanguard Total International Stock Index Fund Admiral Shares (VTIAX).

- 1% – My wife has a 401k that is invested in the Fidelity® 500 Index Fund (FXAIX).

Liabilities

None. Aside from credit cards we pay off every month, we’re debt free.

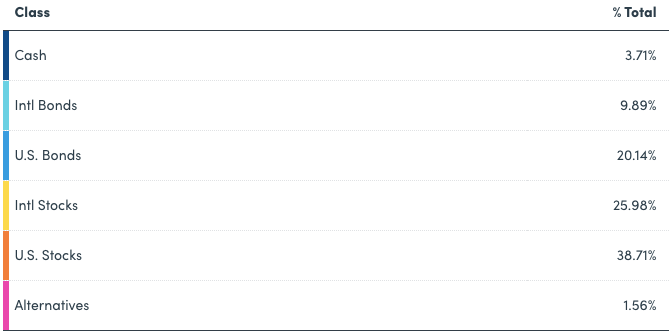

Overall Asset Allocation

Excluding the pension and my house, here’s my overall asset allocation courtesy of our favorite tool that made all of this easy, Personal Capital:

Finance Friday Articles

Here are my favorite articles from this week:

Financial Planning for Early Career Attending Physicians

Following The Stock Market Is Bad For Your Returns

I followed the path to FIRE — and learned that early retirement is the wrong goal

Here are the rest of this week’s articles:

10 Benefits of Keeping Your Credit Score in Good Health

Achieving Work-Life Balance Through Part-Time Work

A Step by Step Guide to Tax Loss Harvesting

Cap Weighted Versus Fundamental Index Funds

How are the 2000 and 2008 retirees doing?

How to Get a Better Deal From a Real Estate Agent

How to Make a Portfolio Rebalancing Spreadsheet

Refinancing Gains in Real Estate

Save first for the kids’ college or for your own retirement?

Top 5 Money Lessons for Physicians

Reader Question – Does the TSP G Fund Count as a Bond or Cash in my Asset Allocation?

A reader wrote in and asked the following question:

Hi there. I thoroughly enjoy your website! When determining what my current asset allocation is, should I consider the TSP’s G Fund as “cash” or as a bond fund? I have a Vanguard account, and their website shows you these great “pie charts” reflecting one’s asset allocation. But what’s the best way to think of the G Fund in this context? Thanks a lot!

The Answer – It’s a Bond Fund

I can see why people might consider the G Fund a cash equivalent in their asset allocation, but I think it is best considered a bond because it is not liquid and is paying intermediate-term interest rates. Plus, Personal Capital agrees with me.

What is a cash equivalent? Here’s what Investopedia says:

Cash equivalents are one of the three main asset classes, along with stocks and bonds. These securities have a low-risk, low-return profile and include U.S. government Treasury bills, bank certificates of deposit, bankers’ acceptances, corporate commercial paper and other money market instruments.

The G Fund invests in “a nonmarketable short-term U.S. Treasury security that is specially issued to the TSP.” That makes it sound like a Treasury bill, which is listed as a cash equivalent above, but remember that the G Fund offers you a free lunch. It is a short term security but the interest rate it pays is:

based on the weighted average yield of all outstanding Treasury notes and bonds with 4 or more years to maturity. As a result, participants who invest in the G Fund are rewarded with a long-term rate on what is essentially a short-term security. Generally, long-term interest rates are higher than short-term rates.

In other words, it is really a hybrid between a short and long-term Treasury.

The other aspect of the G Fund that makes it a bond and not a cash equivalent is that it is not liquid. In other words, because it is in a retirement account you can’t sell it and use the proceeds to buy a car, deal with an emergency, or whatever else you need it for. Cash equivalents like CDs, money market accounts/funds, checking/savings accounts, or cold hard cash are all accessible and could be used for these purposes. Unless you are retirement age and withdrawing from your TSP account, the only way to get to the G Fund would be to take out a TSP loan, which I would not recommend.

Just to double check myself, I went to my favorite tool to automatically track my asset allocation, Personal Capital, to see what they considered my G Fund holdings. Personal Capital is also considering the G Fund a U.S. Bond holding.