personal finance

Guest Post – Military Physician Disability Insurance Enhancements

The only insurance company, Massachusetts Mutual, that will provide active duty military physicians and dentists individual specialty specific, non-cancellable, guaranteed renewable disability insurance coverage has announced some policy and underwriting enhancements to take effect at the end of April. Military physicians/dentists will be able to protect a larger amount of future income utilizing the Future Insurability Option (FIO) Rider. This Rider guarantees the ability to increase coverage in the future based on income regardless of health. This protects against adverse health changes being excluded from coverage. For policies with the Benefit increase Rider (BIR), instead of being limited to increasing coverage only every three years, “off anniversary” increases are allowed under certain circumstances. For example, when military service completes, or income increases significantly (30% or more).

The 24 month mental/nervous disorder maximum benefit period can be extended to age 65 or 67 for an additional 15% premium for all specialties except Anesthesiology, Pain Management and Emergency Medicine. These enhancements are available to new policies only. This is consistent with the discount for military physicians and dentists that Massachusetts Mutual announced last year and will remain in effect.

Disability insurance continues to be a foundational solution to protect military physicians, dentists, and their families by providing financial security not available elsewhere. One key factor to remember, the coverage CANNOT BE ESTABLISHED WHILE ON OVERSEAS DEPLOYMENT OR AFTER RECEIVING ORDERS TO DEPLOY OVERSEAS. For that reason, it is critical to contact us before you expect to receive orders.

*not available in California, District of Columbia, New York

Andy G Borgia CLU

D.K.Unger

Finance Friday Articles

- 4 Malpractice Insurance Pitfalls to Avoid

- Blowing Bubbles

- CAPE Fear

- Do Healthy Young Docs Really Need Life Insurance?

- FIRE & Real Food: Losing 90 Pounds While Adding a Net Worth Comma

- Retirement Planning in the Post-4% World

- Reverse Wealth Transfer on Steroids

- Rising Risk in Bond Funds

- Started From the Bottom

- The False Promise of U.S. Historical Returns

- Time for Gold?

Throwback Thursday Classic Post – Should You Invest in Real Estate?

Just about everyone who invests does so in major asset classes including stocks, bonds, and cash equivalents. When it comes to real estate, though, you’ll find widely divergent opinions about its importance in an investment portfolio. There are some well-respected people and institutions who say that real estate investing is unnecessary, and there are others who will tell you it should be your primary asset class. I’ve recently debated whether I should start investing more heavily in real estate, so I wanted to lay out the basic arguments for and against real estate investing.

What is Real Estate?

The answer to this question is not simple because real estate investing comes in many forms. There are relatively passive ways of investing in real estate, such as Real Estate Investment Trusts (REITs). According to Investopedia, a REIT is “a type of security that invests in real estate through property or mortgages and often trades on major exchanges like a stock.” In other words, you can simply invest in a REIT like you do any other stock, mutual fund, or exchange-traded fund (ETF). Just send your money to your investment company, and you own a little slice of passive real estate.

There are more active methods of investing in real estate, such as fixing and flipping. You purchase a property, you make improvements to it, and then you sell it to someone, hopefully for a profit. As you can imagine, this would take quite a bit more work than investing in a REIT.

There are probably over 100 other ways you can invest in real estate. If you’re interested, I’d check out an article on Bigger Pockets, one of the largest websites about real estate investing, entitled “The Top 100 Ways to Make Money in Real Estate.”

Arguments Against Investing in Real Estate

Regular readers know that Vanguard is my go-to source for both advice and my own investments. Vanguard considers real estate an alternative investment, and according to them “alternatives usually come with more risks and higher costs.” They believe that a diversified portfolio of stocks and bonds provides enough diversification and that alternative investments are unnecessary. Only “sophisticated investors” should consider alternatives, and they see direct real estate investment as “expensive and time-consuming.” Most people have exposure to real estate in the equity in their house and diversified stock/bond funds that often include REITs, real estate companies, and mortgage-backed securities. For these reasons, Vanguard doesn’t think additional investment in real estate is necessary.

Another argument against real estate investing is that it can quickly become a second job. While you can hire property managers, they are probably not going to provide the level of service that the owner would provide. Most of us are already fully employed and don’t need a second job. In addition, owning investment properties can create additional legal risk.

When you purchase an individual property, it is like buying a single stock. You are taking what is called an uncompensated risk. Larry Swedroe defines an uncompensated risk as, “Risk – that is, the risk of owning single stock or sector of the market – that can be diversified away. Since the risk can be diversified away, investors are not rewarded with a risk premium (higher expected return) for accepting this type of risk.” Essentially, you are putting all your eggs in one basket that is not diversified by location or property type. Investing in real estate via a REIT can avoid this problem because REITs invest in properties that are diversified.

Real estate is an illiquid asset class with high transaction fees. While I can sell my stock or bond mutual funds or ETFs in seconds on-line and pay extremely low expenses to do so, it will take me weeks or months to buy or sell a property. In addition, I’ll likely pay 5-10 percent of the price in transaction costs.

Arguments for Real Estate Investing

Real estate is easily acquired, most often by purchasing your own single family house or condominium. You have to live somewhere, and there are several tax advantages to owning where you live. Interest payments on your mortgage and property taxes are probably tax deductible. If you sell your property, capital gains of up to $250,000 if you’re single or $500,000 for couples are tax-free. In addition, paying a mortgage forces you to save by making regular payments, some of which pay off the principle balance of your loan. That is money you’ll get back when you sell.

When compared to stocks or bonds, which have a global, efficient market, real estate often has a local, inefficient market. This means that if you are willing to look, you can probably find some bargains out there much more easily than you can find a bargain stock. Here’s a review of a good book on real estate investing for physicians.

One of the goals of diversification is to have investments that are not correlated with each other. In other words, when investment A drops in price you have investment B that does not. When compared to stocks and bonds, real estate is not perfectly correlated with other investments and therefore provides diversification. An article about the diversification benefit of REITs makes for an interesting read, if you’re interested, although it is a little old. Vanguard came to the conclusion that over-weighting REITs in a target date fund was not worth it. And this very well regarded guy doesn’t believe in over-weighting REITs either.

You can use leverage or “other people’s money” to increase investment returns. Instead of buying a property for $120,000, you could buy three $160,000 properties with a $40,000 down payment on each. This can increase your returns, but in a down market it can also dramatically increase your losses. As many found out during the housing market crash, leverage is a double-edged sword.

Real estate is an inflation hedge. Burton Malkiel says, “A good house on good land keeps its value no matter what happens to money.” Rents and property values tend to rise as prices rise, preserving your purchasing power. Since your mortgage payment doesn’t change with inflation, while rents are going up your mortgage payment remains the same. Stocks do hedge inflation somewhat, but the companies they represent and the stocks themselves tend to get hurt as the prices of raw materials rise.

The Bottom Line

There are a lot of different ways to invest in real estate, passively investing in REITs, fixing and flipping, owning rental properties, and all sorts of other investment opportunities. Like Vanguard, I don’t think it is necessary to invest in real estate, but it is something to consider if you think you will either enjoy it or believe the value it adds to your investment portfolio is worth the effort.

Save Some for Your Future Self

Jonathan Clements was a longtime personal finance columnist for The Wall Street Journal, and he offers great advice at the best price you can get (free) on his blog Humble Dollar. Here is one piece of advice from his site:

“SAVE SOME FOR YOUR FUTURE SELF. Looking to lose weight? At restaurants, transfer half your serving to a second plate and ask the waiter to box it up. If the food will make good leftovers, it’s easy to do, because you know you’ll have a treat tomorrow. Want to save more? Think about it the same way—and set aside some of today’s spending money for tomorrow.”

If you are wondering how much to save for your future self, here are a few ways to figure that out.

To start, you have to figure out your gross (pre-tax) income. Include every dollar you get, even the non-taxable allowances. If you’re not sure exactly, take your best guess.

The Minimum

In my opinion, the absolute bare minimum you need to save for retirement is 10% of your gross income. You can include all of your employee contributions in this, like the DoD match in the Blended Retirement System. This doesn’t have to all be your money.

That said, 10% is the minimum. You’ll likely work into your 60s unless you stay in long enough to have a pension.

The Most Common Recommendation

Most commonly people recommend you save 12-15% of your gross income for retirement. If you read this article from Vanguard about how much to save, you’ll see:

If retirement is decades away, setting a specific goal amount is probably unnecessary. For now, focus on:

1. Immediately saving at least enough to get the full match offered by your employer plan, if you have one. This is free money—don’t let it pass you by.

2. Working your way up to 12%–15% of your pay, including any employer match. For example, you could increase your savings rate 1% every year until you reach your target rate. This should get you in the ballpark of what you’ll need.

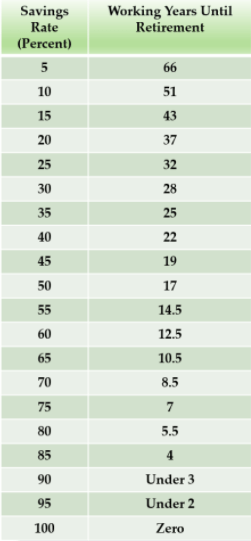

The Early Retirement Recommendation

If you want to achieve financial independence or have the option of retiring early, you probably need to save more than 15%. Mr. Money Mustache’s amazing post about the shockingly simple match of early retirement has this table that shows you how long you’ll need to work based on your savings rate:

The Bottom Line

Start with your gross pay. You need to save a minimum of 10% of that, but you should try to save at least 15%. If you want to achieve financial independence and have the option to retire early or go to part-time work, you need to save more than 15%. I’d recommend 20% or more. I’ve done 30% my whole career.

If you want out help saving for retirement, start here where we discuss it in more depth.

Finance Friday Articles

- 7 Truths From a Gut-Wrenching Stock Market Crash, One Year Later

- 12 Things to Know About Choosing a Financial Advisor

- Everyone is Using The 4% Rule Wrong

- Retirement Checklist for Physicians

- Second TSP investment manager to be added

- The Simplest Asset to Hedge Against Inflation

- Top 10 Ways to Lower Your Taxes

- We’re All Active Investors

- You have an extra month to file your federal tax returns

Estimate Your Retirement Income Needs

Jonathan Clements was a longtime personal finance columnist for The Wall Street Journal, and he offers great advice at the best price you can get (free) on his blog Humble Dollar. Here is one piece of advice from his site:

“ESTIMATE YOUR RETIREMENT INCOME NEEDS. Take your annual salary. Subtract how much you save each year and pay in Social Security payroll taxes. Also subtract your annual debt payments, including your mortgage—assuming these debts will be paid off by retirement. Result: You’ll know roughly how much you will need each year for a comfortable retirement.”

I’ll take this action one step further. Once you have the rough estimate of how much annual retirement income you need, go to this calculator and figure out how much your military pension will be worth. Then go to this calculator and figure out how much Social Security you’ll get. What is left is what you need to generate with the rest of your investments. Now take that number and divide it by 0.04. That is approximately how much you need to accumulate in your investment accounts to be able to retire.

For example, let’s say you use Mr. Clements’ method and get a number of $120,000/year for a comfortable retirement. The calculators tell you that you will get about a $42,000/year military pension and $18,000/year from Social Security. That leaves $60,000/year you need to generate from your investments. Divide that by 0.04 and you get $1,500,000, which is how much you’d need in your investment accounts to retire.

Finance Friday Articles

- Coping With a Crazy Market

- How Do Women Really Invest?

- Is Diversification Finally Working?

- Mortgage Financing Guide for Doctors

- Nine Roads to Ruin

- Owning Individual Stocks vs. Owning the Stock Market

- ‘This Is Unprecedented’: Why America’s Housing Market Has Never Been Weirder

- Two Worlds: So Much Prosperity, So Much Skepticism

- What? Spend It? A Discussion about Bitcoin

- Will the Real Retirement Income Number Please Stand Up?

The Basics of Saving for Retirement

Here is a review of the basic principles of investing for retirement:

- Start saving as early as possible because to get rich slowly you need to take advantage of compound interest. Albert Einstein (might have) said, “Compound interest is the eighth wonder of the world. He who understands it, earns it…he who doesn’t pays it.” Compound interest is earning an investment return not just on your initial investment or principle, but also on your previous return. In other words, if you invest $1,000 and earn a 10% return yearly, after the first year you’ll have $1,100. The second year you’ll earn 10% on your initial $1,000, but also on the $100 you earned during the first year, leaving you with $110 of earnings during the second year instead of $100 like the first year. Over a long period of time, this phenomenon greatly increases the amount of money you can accumulate with your investments. Because of this, time spent in the market is much more important than trying to time the market by buying and selling at the right times. The long-term return of the stock market is approximately 9.5% per year. Adjusting for 3% inflation, $1 invested grows to: (Ref: Bogle)

- $1.88 in 10 years

- $3.52 in 20 years

- $6.61 in 30 years

- $12.42 in 40 years

- $23.31 in 50 years

- If you find it difficult to save, set up an automatic investment plan so that the money is automatically removed from your pay and you never get a chance to spend it.

- Investment costs and taxes matter in the long run and will never end; therefore both must be minimized as much as possible. You can minimize both by investing in low-cost stock and bond index funds and maximizing your contributions to tax-preferred retirement accounts.

- Long-term investment in the stock market is the surest way to make your investment grow over time and beat inflation. By owning stocks you own businesses, and the long-term return of these businesses is what will increase your investments and net worth. Trading stocks is not the goal…owning them is.

- As you progress toward retirement, you will decrease your investment risk by decreasing the amount you invest in stocks and increasing the amount you invest in bonds.

- The optimal allocation of investments depends on your age, financial situation, risk tolerance, and how soon you will need to utilize the investment. If you are young, you have longer to ride out the inevitable market swings. The more financially secure you are, the better you can deal with the swings as well. Your asset allocation should also reflect the amount of risk tolerance you have. My opinion is that early in your career you should take as much risk as you can tolerate. If you can’t sleep at night because you are worried about your investments, it is time to dial down the risk, but you should take as much risk as you can up to that point. More risk yields a higher return over the long-term.

- You should utilize dollar cost averaging to decrease your investment risk. Dollar cost averaging is when you purchase the same dollar amount of investments periodically over a long period of time. It provides time diversification, ensuring that you don’t buy all of your investment during a time of temporarily inflated prices. In volatile markets that are going up and down, it will actually increase your investment return because it ensures that you purchase less shares when the investment is expensive, and more when it is cheaper.

- The market will go down, and when it does you need to resist the temptation to sell investments or stop investing. The best time to buy an investment is when it is cheap and you can get the best deal. When the market recovers, which it will, you will reap the rewards. Focus on the long-term and just keep investing.

- Every time you get a raise, bonus, or income tax refund, use it to increase the amount you invest for retirement. You should save at least 15% of your gross or pre-tax income for retirement, but if you want to be rich or retire early you’ll need to save 20-30%.

- How much money will you need to retire? Most retirement planners state that you’ll need approximately 70% of your pre-retirement income to maintain your current standard of living once you retire. This number, though, is heavily dependent on what you consider to be a “good retirement” and what type of a lifestyle you intend to lead. For example, since I save 30% of my gross income for retirement, I’m already living on only 70%, so I highly doubt I’ll need that much when I retire. If you are frugal and pay off your mortgage, you may find that you need as low as 25% of your pre-retirement income to retire comfortably. You won’t be staying in the Ritz Carlton, but there’s nothing wrong with the Hampton Inn.

- There is a lot of uncertainty in life, but the 4% rule is a nice rule of thumb to use when assessing how much money you’ll need to accumulate before you can retire. The 4% rules says that you can take 4% from your retirement savings annually, adjust for inflation each year, and never run out of money. The devil is in the details, but use the 4% rule and assume that you can get approximately $40,000 per year of retirement income from every $1 million you have saved.

- Saving for retirement is your top savings priority, even over funding the college education of your children. You can borrow money to pay for college, but you can’t borrow money to retire.

- You must maximize your contributions to tax-preferred retirement accounts, such as 401(k), 403(b), Simplified Employee Pensions (SEPs), or Individual Retirement Accounts (IRAs) every year. The tax benefits of these plans are staggering over the long-term: (Ref: Malkiel and Ellis)

- If you invest $5,000 per year over 45 years and earn an 8% return with no taxes paid until withdrawal during retirement, you will have a final portfolio value of over $2 million. If you pay 28% taxes at withdrawal, you’d have almost $1.5 million.

- The same savings without the benefit of tax deferral will top out at about $750,000.

- If you work as an independent contractor you have more options than a physician who works as an employee, so hire an experienced tax or health care attorney, accountant, or fee-only financial planner to set up the best options for retirement investments if you are uncomfortable doing this on your own. It is probably going to be easy, though, and you just need to open of a solo/individual 401k with an investment company.

- NEVER use retirement savings for anything other than retirement unless it is absolutely unavoidable. Again…you can’t borrow money for retirement.

References

Bogle, John C. The Little Book of Common Sense Investing: The Only Way to Guarantee Your Fair Share of Stock Market Returns. Hoboken: John Wiley & Sons, Inc., 2007.

Malkiel, Burton and Charles Ellis. The Elements of Investing: Easy Lessons for Every Investor. Hoboken: John Wiley & Sons, Inc., 2013.

Put Retirement First

Jonathan Clements was a longtime personal finance columnist for The Wall Street Journal, and he offers great advice at the best price you can get (free) on his blog Humble Dollar. Here is one piece of advice from his site:

“PUT RETIREMENT FIRST. Are you socking away at least 12% of your pretax income toward retirement, including any matching contribution to your employer’s retirement plan? To amass enough for retirement, you may need to throttle back other financial ambitions, including the size of the house you buy and how much you help your kids with college costs.”

This advice is about two things, savings rate and priorities. First, let’s tackle savings rate.

One of the seminal moments in my financial life occurred when I read the book The Automatic Millionaire by David Bach. In that book was a table that said something like this:

- If you want to be poor and work your entire life, save < 10 percent of your gross or pre-tax income.

- If you want to be normal and retire at a traditional age, save 10-20 percent of your gross or pre-tax income.

- If you want to be rich and retire early, save 20 percent or more of your gross or pre-tax income.

You can probably guess how my story ended…I saved 20 percent. Then I increased by 1 percent every 1-3 months until I hit 30 percent, which has been my savings rate ever since. This is probably the #1 reason I am financially independent. The #2 reason is the value of my military pension.

As Mr. Clements discusses, when you put retirement first it isn’t just about your savings rate, though. It is also about priorities.

You can’t borrow money to retire, therefore you need to max out your retirement savings before you start saving money for your kids’ education.

You need to max out your retirement savings before you buy a house that is larger than you really need.

You need to max out your retirement savings before you pay for private school.

You need to max out your retirement savings before you purchase a new car or a used luxury car.

It’s your life and it’s your retirement. Get your priorities straight and make retirement your #1 financial priority.