personal finance

Throwback Thursday Classic Post – Asset Location

Here’s a tip on asset location from one of my favorite blogs and authors, Jonathan Clements from Humble Dollar:

After deciding what investments to buy, we should consider asset location. What’s that? It involves divvying up investments between taxable and retirement accounts. If investments generate large annual tax bills—think taxable bonds and actively managed funds—we’ll typically want to hold them in a retirement account.

Jonathan’s advice is the traditional advice. Put your taxable bonds, like the Thrift Savings Plan (TSP) F and G funds, into your retirement accounts. This is what I do. My F and G funds are in the TSP, clearly a retirement account.

I don’t own actively managed funds, and I also don’t invest in real estate investment trusts (REITs), although I have in the past and I think about it pretty frequently.

There is another school of thought, though. The White Coat Investor has a different take. You can read about them in his posts entitled My Two Asset Location Pet Peeves and Bonds Go in Taxable!

Of note, just about everyone says to put actively managed funds or REITs in a retirement account, so you won’t find any arguments there.

If you’re really interested in this concept/discussion, the Bogleheads Wiki on tax efficient fund placement is a great read as well.

Finance Friday Articles

- 5 Ways to Invest in Real Estate Without Being a Landlord

- 10 Tax-Free Investments to Consider

- Five Lessons from the Pandemic

- How to Feel Better About Your Financial Situation

- It’s All in the Mix of Assets

- Owning Assets Beats Having a Job

- Should You Have a Tech Stock Allocation in Your Portfolio?

- Spend $200K in Retirement and Pay $0 Income Tax

- What is a robo-advisor?

- Why bonds still matter in a low-yield world

- Why This is Not Another Housing Bubble

Throwback Thursday Classic Post – Will the Government Ever Get Rid of the “Free Lunch” of the TSP G Fund?

They say there’s no free lunch, but in the Thrift Savings Plan there is a free lunch, and it’s called the G Fund. Will the government get rid of this free lunch?

The G Fund Free Lunch

What is this free lunch? You can read about it on this page in the Fees & More Info section:

The G Fund Yield Advantage—The G Fund rate calculation results in a long-term rate being earned on short-term securities. Because long-term interest rates are generally higher than short-term rates, G Fund securities usually earn a higher rate of return than do short-term marketable Treasury securities.

The government is paying you a higher interest rate than it should. That is the G Fund free lunch.

Why is the Free Lunch at Risk?

The government periodically considers getting rid of it. For example, you can read about it in this article, which is discussing the President’s FY19 budget plan/request. Here’s the relevant portion:

The plan also proposes reducing the statutorily mandated rate of return for the government securities (G) fund to be based on either the three-month or four-week Treasury bill, at a projected savings of $8.9 billion over 10 years.

“G Fund investors benefit from receiving a medium-term Treasury Bond rate of return on what is essentially a short-term security,” the White House wrote. “The budget would instead base the G-fund yield on a short-term T-bill rate.”

TSP spokeswoman Kim Weaver said changing the G Fund’s yield, which is currently 2.75 percent annually, would have a disastrous effect on participants’ ability to save for retirement. If Congress changed the G Fund to track the three-month Treasury bill, the yield would decrease to 1.46 percent, and for the four-week bill it would drop to 1.43 percent.

“Such a change would make the G Fund inadequate and ineffective from an investment standpoint for TSP participants who are saving for retirement,” Weaver said in an email. “More than 3.6 million TSP participants (69 percent) have all or some of their account balance invested in the G Fund. Of those with money in the G Fund, 2 million (39 percent) hold the G Fund as their sole investment choice.”

For a TSP participant who has just retired and is invested entirely in the L Income Fund, which is designed for people who have begun taking annuity payments, they would run out of money at age 84 instead of the current projected age of 92, Weaver said.

Jessica Klement, staff vice president for advocacy at the National Active and Retired Federal Employees Association, said the change would make G Fund investments “useless” and likely force TSP administrators to divest from it entirely.

“[The new rate] would not even keep up with inflation,” she said. “So if you wanted to keep your money in a mostly secure fund, you would not be getting any return, and you’d actually be losing money. And if you took your money out, there would be no other safe, secure investment for those nearing or in retirement.”

What Does This Mean For You?

Right now, it means nothing. This is all just discussion about something that might happen in the future.

What you do need to understand, though, is that the G Fund serves a specific purpose in your portfolio. As the TSP site says:

Consider investing in the G Fund if you would like to have all or a portion of your TSP account completely protected from loss. If you choose to invest in the G Fund, you are placing a higher priority on the stability and preservation of your money than on the opportunity to potentially achieve greater long-term growth in your account through investment in the other TSP funds.

It is alarming that Ms. Weaver from the TSP said, “Of those with money in the G Fund, 2 million (39 percent) hold the G Fund as their sole investment choice.” Those 2 millions people are sacrificing long-term growth for the safest and most conservative investment available in the TSP.

There’s nothing wrong with that if you’re doing it because you are very conservative, near retirement, or the G Fund serves as the bond portion of a larger, more diversified portfolio that has more risky assets like stocks or real estate.

The sad reality is that most who are solely invested in the G Fund are that way because it used to be the default option for those starting a TSP account, and they never switched it to a more aggressive investment option. Under the new Blended Retirement System, the default investment switched from the G Fund to an age-appropriate Lifecycle fund.

What’s the Bottom Line?

The G Fund gives you a free lunch, paying you a higher long-term interest rate while you are investing in short-term securities. The government periodically talks about getting rid of that free lunch.

If you are invested in the G Fund, make sure you are doing it purposely and are aware of its conservative nature. Its emphasis is on preserving wealth rather than growing wealth.

Finance Friday Articles

- 10 Errors to Avoid When Refinancing

- Charitable Giving Strategies

- From SPACs to Space

- How Many Months’ Worth of Spending Do You Need in Your Emergency Fund?

- Oops. I Did It Again. The Latest Scam I Fell Victim To.

- Risk Less Make More

- The Problem With Optimizers – Backward-looking Data Can Lead to Distorted Results

- The Risks in Buying Individual Stocks

- TSP Opposes Creating Fossil Fuel-Free Fund

- When You Invest, Start with the Right Questions (Hint: They’re Pretty Simple)

- Why Hospital Administrators Should Eat Last

- Why You Shouldn’t Pick Individual Stocks

Throwback Thursday Classic Post – Check Your Beneficiary Designations

Here’s a tip from one of my favorite blogs and authors, Jonathan Clements from Humble Dollar:

CHECK YOUR BENEFICIARY DESIGNATIONS. Your retirement accounts and life insurance will typically pass to the beneficiaries specified on those accounts, not the people named in your will. If your family situation has changed, or you simply don’t remember who you listed, take a moment to review your beneficiary designations.

Don’t let the ex-spouse get your money when you die! Update your beneficiaries.

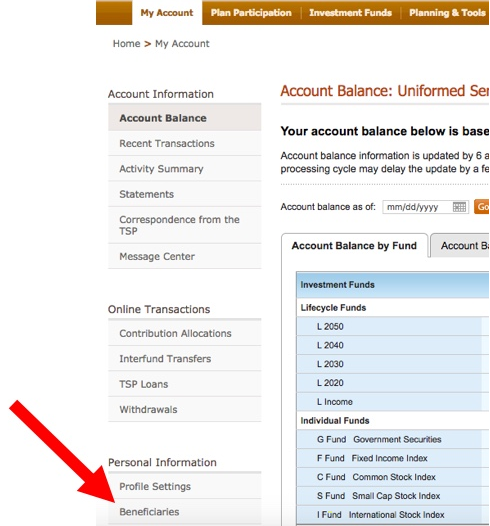

How to See Your Beneficiaries for the Thrift Savings Plan (TSP)

If you log on to the TSP page, you need to click on the link along the lower left, marked by the large red arrow:

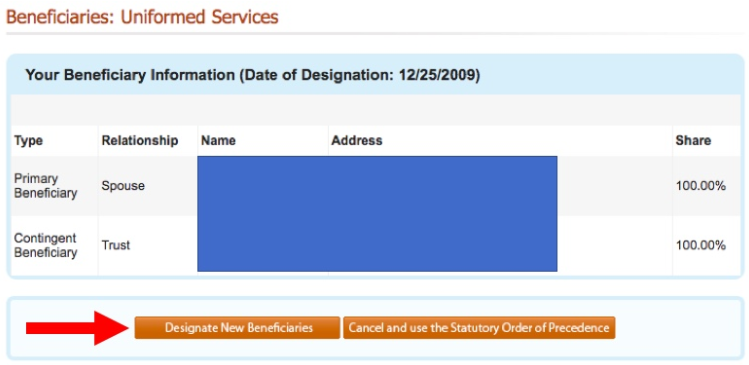

Then you’ll see this, and you can change them at the bottom:

Then you’ll see this, and you can change them at the bottom:

Disability Insurance for Reservists

Here’s a link to this White Coat Investor article:

Throwback Thursday Classic Post – Invest in Your Taxable Account Thoughtfully

Here’s a tip on investing in your taxable account from one of my favorite blogs and authors, Jonathan Clements from Humble Dollar:

INVEST YOUR TAXABLE ACCOUNT THOUGHTFULLY. If you purchase the wrong investments in your taxable account, you may be reluctant to sell, because you’ll trigger capital gains taxes. A good choice: low-cost U.S. and international total stock market index funds, which should be tax-efficient—and which shouldn’t ever lag far behind the market averages.

For those of us in the military, investing in a taxable account comes into play in a few scenarios…

Scenario #1 – You and your spouse (if you have one) have filled your Thrift Savings Plan (TSP) and all other retirement accounts available including IRAs, yet you want to save more for retirement. In this case, you put the rest in a taxable account with the investment company of your choice (Vanguard, Fidelity, Schwab, etc.). This is what I do when all of my retirement accounts are full, and just like Jonathan mentions I invest purely in broad, low-cost index funds at Vanguard. The only taxable holdings I have are the Vanguard U.S. and international total stock market index funds.

Scenario #2 – You are saving for a financial goal that is not related to retirement, such as a downpayment on a home or for a new car. If you’re saving for college, you’d use a 529 plan, but for just about anything else you could use a taxable account. For example, I used to have my emergency money and extra spending money in a money market fund among my taxable accounts. The alternative to this is to use a bank and invest in a high-yield savings account (which is what I do now), a certificate of deposit (CD), or a money market account. Bankrate.com will show you the best rates for each of these reasonable alternatives.

If you are using a taxable account, there are a few things to consider. If you are investing in bonds, you may want to invest in municipal bonds in your taxable account due to the tax benefits. If you are a fan of target date funds, you may not want to use them in a taxable account because the bond portion will kick off income that is taxed at your full marginal tax rate. Most feel that bonds are better placed in a tax-advantaged retirement account unless you are using municipal bonds.

Guest Post – Military Physician Disability Insurance Enhancements

The only insurance company, Massachusetts Mutual, that will provide active duty military physicians and dentists individual specialty specific, non-cancellable, guaranteed renewable disability insurance coverage has announced some policy and underwriting enhancements to take effect at the end of April. Military physicians/dentists will be able to protect a larger amount of future income utilizing the Future Insurability Option (FIO) Rider. This Rider guarantees the ability to increase coverage in the future based on income regardless of health. This protects against adverse health changes being excluded from coverage. For policies with the Benefit increase Rider (BIR), instead of being limited to increasing coverage only every three years, “off anniversary” increases are allowed under certain circumstances. For example, when military service completes, or income increases significantly (30% or more).

The 24 month mental/nervous disorder maximum benefit period can be extended to age 65 or 67 for an additional 15% premium for all specialties except Anesthesiology, Pain Management and Emergency Medicine. These enhancements are available to new policies only. This is consistent with the discount for military physicians and dentists that Massachusetts Mutual announced last year and will remain in effect.

Disability insurance continues to be a foundational solution to protect military physicians, dentists, and their families by providing financial security not available elsewhere. One key factor to remember, the coverage CANNOT BE ESTABLISHED WHILE ON OVERSEAS DEPLOYMENT OR AFTER RECEIVING ORDERS TO DEPLOY OVERSEAS. For that reason, it is critical to contact us before you expect to receive orders.

*not available in California, District of Columbia, New York

Andy G Borgia CLU

D.K.Unger

Finance Friday Articles

- 4 Malpractice Insurance Pitfalls to Avoid

- Blowing Bubbles

- CAPE Fear

- Do Healthy Young Docs Really Need Life Insurance?

- FIRE & Real Food: Losing 90 Pounds While Adding a Net Worth Comma

- Retirement Planning in the Post-4% World

- Reverse Wealth Transfer on Steroids

- Rising Risk in Bond Funds

- Started From the Bottom

- The False Promise of U.S. Historical Returns

- Time for Gold?