personal finance

Check Your Fund Expenses

Jonathan Clements was a longtime personal finance columnist for The Wall Street Journal, and he offers great advice at the best price you can get (free) on his blog Humble Dollar. Here is one piece of advice from his site:

CHECK YOUR FUND EXPENSES. If you own index funds, aim for weighted average annual expenses below 0.2%. If you own actively managed funds, you’ll pay more—but allocate enough of your portfolio to index funds to keep your average below 0.4%. By holding down costs, you’ll keep more of what you make, plus low-cost funds typically outperform high-cost competitors.

In the military, we’re blessed with the Thrift Savings Plan (TSP) and its industry leading low expenses. Outside of the TSP, if you want to keep your costs down you should just invest with Vanguard. Their unique structure makes them a non-profit, unlike their competitors, so no matter what you invest in you know it will be among the lowest cost investments available. Admittedly, though, there is a price war and you can find the same funds for even lower costs at Schwab and Fidelity.

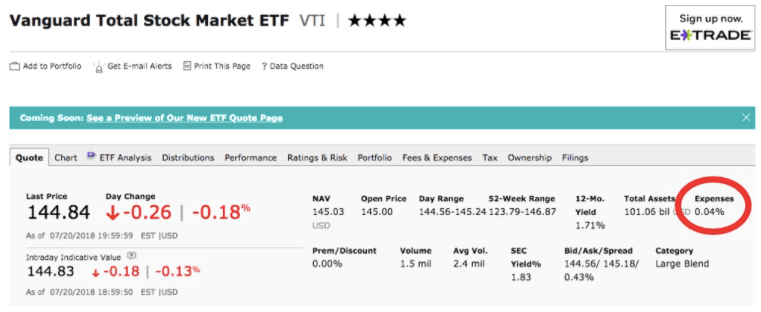

Whatever you invest in, take the time to look up the investments at Morningstar. Just type your investment in the search bar at the top and check the expense ratio. As an example, I typed in VTI, which is the Vanguard Total Stock Market Exchange Traded Fund (ETF). The expense ratio of 0.04% is circled in red:

As Mr. Clements mentions, if the expense ratios for index funds are more than 0.2% then you are paying too much. You should try to keep the total expense ratio of all your investments less than 0.4%.

Finance Friday Articles

Here are my favorites:

- 6 Fixed-Income Options for a Low-Yield Environment

- Anchoring & Adjustment in the Stock Market

- Seems So Easy

- True Wealth

Here are the rest of the articles:

- Analyzing Winning Mutual Funds

- Buy One Property a Year and Retire Early

- Can I Employ My Spouse?

- Five Reasons I Like Hanging Out with Millionaires

- How to Buy a Second Home that Pays for Itself

- How to Deal with High Anxiety Due to the Election

- How to Find an Emerging Real Estate Market

- International Stocks & Asset Location: Is Taxable or Tax-Advantaged Best?

- Is Refinancing Your Student Loans the Right Move?

- Low Income Doctor in a High Cost of Living Area

- Not Exactly True

- Student Loan Advice: 7 Rules of Thumb

- The Arrival Fallacy

- The Coming Psychological Revolution in the Housing Market

- The Importance of Automating Your Real Estate Investments

- Wanting a tax deferral opt-out a ‘reasonable issue,’ says Trump official

- What to Do with Suboptimal Assets in Your Portfolio

- What You Need to Know About Ground-Up Multifamily Development

Throwback Thursday Classic Post – Step 6 to Crush the TSP – Rebalance Annually

We’ve talked about steps 1-5 to crush the Thrift Savings Plan (TSP). Now we move on to the final step (unless I think of more), step 6 – rebalance annually.

What is Rebalancing?

Let’s say that your desired TSP asset allocation is 70% stocks and 30% bonds. After the last year, though, stocks earned more than bonds and now you’re sitting at 85% stocks and 15% bonds. In order to rebalance back to your desired asset allocation, you’d sell approximately 15% of your stocks and buy bonds, restoring your desired asset allocation. It’s that simple.

Why Should You Rebalance?

If you don’t, you may be assuming more or less risk than you desire.

Also, by rebalancing you force yourself to sell what has overperformed and buy what has underperformed. Although this seems counter-intuitive because you are selling what has given you the largest return, by doing this you are systematically selling high and buying low. When left to themselves, investors typically buy high and sell low, the opposite of what you want to do. Rebalancing forces you to do it right.

How Often Should You Rebalance?

Vanguard has researched this, and you can read their full report here:

Best Practices for Portfolio Rebalancing

Their conclusion is:

We conclude that for most broadly diversified stock and bond fund portfolios (assuming reasonable expectations regarding return patterns, average returns, and risk), annual or semiannual monitoring, with rebalancing at 5% thresholds, is likely to produce a reasonable balance between risk control and cost minimization for most investors.

In other words, you rebalance annually or semiannually (twice per year) whenever your current asset allocations are off by 5% or more from your desired allocations. If the current and desired allocations are within 5% of each other, you do nothing.

How Do You Rebalance in the TSP?

You just log on and do what they call an “interfund transfer” or IFT. You can read all about it on this page from the TSP website.

Because you are doing it in a tax-advantaged retirement account, there are no expenses, fees, or taxes associated with rebalancing (unlike if you were rebalancing a taxable account).

You can only do it twice per month without restrictions, but since you are smart you are only doing it once per year anyway.

Do You Need to Rebalance With Lifecycle Funds?

No, you don’t. This is one of the major advantages of the L funds. If you are hitting the easy button on your TSP and just using a Lifecycle fund, you don’t need to rebalance…EVER!

That’s It. Crush the TSP!

That’s the final step to crush it in your TSP account. Read the whole series, maximize your TSP contributions, and get rich in the military.

Finance Friday Articles

Here are some more articles on the social security withholding change:

- More Guidance Released on Social Security Withholding Change

- Some Light Shed on Repayment of Social Security Tax Suspension

Here are my favorites this week:

- 5 Reasons to Pay Off Debt (Instead of Investing)

- Staying in Bounds

- The Power of Financial Freedom

- There is No Such Thing as “Good” Debt

Here are the rest of the articles:

- Achieve Better Cash Flow Diversification

- Coming Up With a TSP Withdrawal Strategy

- Early Retirement Checklist Part One

- Exclusive: The Billionaire Who Wanted To Die Broke . . . Is Now Officially Broke

- Guide to Financial Wellness for the Academic Physician

- How Much Lifestyle Creep is Okay?

- Medical Degree to Financially Free Course Review

- My Recent State Tax Audit

- Negativity Is Not an Investment Strategy

- Our 2019 Tax Return Revealed: Total Income $522,662, Taxable Income $253,906

- Positive Cash Flow: Open Secret In Early Retirement

- Saved by a Crash

- The Disability Insurance Process

- The Ultimate Passive Income

- The Vanishing Difference Between ESG and Conventional Funds

- When to Change

Throwback Thursday Classic Post – Step 5 to Crush the TSP – Roth vs Traditional

We’ve talked about steps 1-4 to crush the Thrift Savings Plan (TSP). Now we’re on to step 5, deciding between the Roth vs traditional TSP. Let’s take a look at the difference between the two and help you to decide which is the right choice for you.

The Traditional TSP

The traditional TSP is the first of two potential tax treatments for your TSP contributions. If you elect it, you defer paying taxes on your contributions and their earnings until you withdraw them. This is the only option for any money you get as a result of the 5% government match in the new Blended Retirement System (BRS).

If you are in a combat zone making tax-free contributions, your contributions will be tax-free at withdrawal but your earnings will be subject to tax.

The Roth TSP

The Roth TSP is the second of two potential tax treatments for your TSP contributions. If you contribute to it, you pay taxes on your contributions now and your earnings are tax-free at withdrawal.

The Roth TSP is similar to a Roth 401(k) that a civilian would have, not a Roth IRA. There are no income limits for Roth TSP contributions. You can contribute to both your Roth TSP and a Roth IRA without contributions to one affecting how much you can contribute to the other. For example, in 2019 you can contribute the full $19,000 to your Roth TSP and $6,000 to your Roth IRA.

Which One is Best for You?

Here’s a table that compares the two options from the TSP website:

| The Treatment of… | Traditional TSP | Roth TSP |

|---|---|---|

| Contributions | Pre-tax | After-tax1 |

| Your Paycheck | Taxes are deferred*, so less money is taken out of your paycheck. | Taxes are paid up front*, so more money comes out of your paycheck. |

| Transfers In | Transfers allowed from eligible employer plans and traditional IRAs | Transfers allowed from Roth 401(k)s, Roth 403(b)s, and Roth 457(b)s |

| Transfers Out | Transfers allowed to eligible employer plans, traditional IRAs, and Roth IRAs2 | Transfers allowed to Roth 401(k)s, Roth 403(b)s, Roth 457(b)s, and Roth IRAs3 |

| Withdrawals | Taxable when withdrawn | Tax-free earnings if five years have passed since January 1 of the year you made your first Roth contribution, AND you are age 59½ or older, permanently disabled, or deceased |

* If you are a member of the uniformed services receiving tax-exempt pay (i.e., pay that is subject to the combat zone tax exclusion), your contributions from that pay will also be tax-exempt.

1. Roth contributions are subject to Federal (and, where applicable, state and local) income taxes, while traditional contributions are not taxed until withdrawn. However, both Roth contributions and traditional contributions are included in the amount of wages used to calculate payroll taxes (e.g., Social Security taxes).

2. You would have to pay taxes on any pre-tax amount transferred to a Roth IRA.

3. Transfers to a Roth IRA from a Roth TSP are not subject to the income restrictions that apply to Roth IRA contributions.

The issue of whether Roth is a good option for you was discussed in this TSP Highlights called Is Roth For You?

If you like interactive calculators, this one from Betterment is pretty good.

If you don’t trust anything I say and want to read what someone else thinks, I don’t blame you. Here’s a good article from Money.

The decision really boils down to whether you’d like to pay taxes now (Roth) or later (traditional) and how your current tax rate compares to your likely future tax rate during retirement. While predicting the future is not easy, if you are young or early in your career, your earnings and tax rate are likely to rise in the future, so you should probably lean toward the Roth option. If you are in your peak earning years and you expect your tax rate to fall in retirement, you should probably lean toward the traditional and defer taxes to a future date.

If you are not sure which option to choose, many people recommend you diversify your retirement accounts and simply split the Roth and traditional 50/50. That way in the future you’ll have options depending on how future tax rates and your financial situation changes.

What do I do? I can afford the taxes now and want as much tax-free money available to me as I can get, so I put all the money in the Roth TSP that I can. That said, the first part of my career I didn’t have a Roth option, so a large percentage of my TSP balance is in the traditional TSP as well, so I’m about 50/50 split between the two options.

Some Rules to Be Aware Of

The TSP keeps your traditional and Roth money in separate “buckets” in your TSP account.

You cannot convert any portion of your existing traditional TSP balance to a Roth balance.

You can make both traditional and Roth contributions if you want. You can contribute in any percentages or amounts you choose and can change your election at any time.

If you are getting government contributions (perhaps because you are in the Blended Retirement System), they are deposited into your traditional TSP. You can put your portion in the Roth, but the government’s portion must go in the traditional.

The Bottom Line

Use the resources above to decide if you want to invest in the traditional TSP, the Roth TSP, or some combination of the two. If you’re not sure what to do, I’d just split it 50/50 so you have options in the future.

Keep your eye out for the last step to crush the TSP, rebalancing.

Finance Friday Articles

Here are my favorites this week:

A Dozen Dumb Money Mistakes Doctors Make

Asset Allocation: Designing Your Portfolio Pt 5

Just Say No to Private Equity Funds

The 9 Best Income Producing Assets to Grow Your Wealth

Here are the rest of the articles:

5 Reasons I’m Not Joining the Dropout Club

5 Things You Can Do With an Old 401(k)

Buying a Turnkey Property Out of State

Depreciation: My Favorite Tax Break Is Now Even Better

Helping Others During the Pandemic

How to Get a Mortgage With a Great Rate

Online Term Life Insurance Quotes: PolicyGenius Versus Term4Sale

Riders Physicians Need to Review When Choosing a Long-Term Disability Insurance Policy

Should I Invest in Precious Metals and Cryptocurrencies?

The Work From Home Backlash is Upon Us

Throwback Thursday Classic Post – Step 4 to Crush the TSP – Invest

You’ve read steps 1, 2, and 3 to crush the Thrift Savings Plan (TSP), and now you’re ready for step 4 and to start investing. In step 3 you came up with your desired asset allocation, so make sure you have that. You’re going to need it for the rest of the post. Just to make life a little easier, we’re going to use an example asset allocation of 80% stocks and 20% bonds.

Bond…James Bond

For the bond portion of your asset allocation, you only have two investment choices:

- G Fund – US government bonds (specially issued to the TSP)

- F Fund – US government, corporate, and mortgage-backed bonds

Both of these are US bond options, which is just fine. There are no international bonds available in the TSP.

We could have an intellectual discussion about the subtle differences between these two bond funds, but we’re not going to. It isn’t necessary. They’re both fine bond funds, so just split the difference, diversify, and put half of your bond allocation in the G fund and half in the F fund.

To illustrate, in the example allocation of 80% stocks and 20% bonds, we’d put 10% in the G fund and 10% in the F fund.

That’s it. The bonds are done.

The Stock Allocation

This is a little more complicated. The largest decision you have to make is how you’re going to divide your stocks between the three options. Here are your choices:

- C Fund – stocks of large and medium-sized US companies

- S Fund – stocks of small to medium-sized US companies (not included in the C Fund)

- I Fund – international stocks of more than 20 developed countries

The first question is what percentage of your stock allocation should go to the I fund. There are a few schools of thought on this.

John Bogle, the founder of Vanguard, is famous for believing that you don’t need to invest any of your stocks in international stocks. His long held belief was that the US companies are doing business globally, so they are already worldwide diversified. For example, Coca-Cola is clearly selling Coke products all over the globe. He would say you should put 0% of your stocks in the I fund.

At the other end of the spectrum are people who believe that you should invest proportionally. If you look at the worldwide value of stocks, it is about a 50/50 split between the US and the rest of the world. These people would say you should put 50% of your allocation in international stocks.

Both of these opinions are reasonable, so anything between 0% and 50% allocated to the I fund is fine. What do I do?

I rely on the research done by Vanguard, an institution managing over $5 trillion. I figure they have more money and resources to research this stuff than I do. What does Vanguard do?

If you look at their Target Retirement Funds, which are meant to be a “one stop shop” kind of investment fund, you’ll notice that they split their stock allocation so that 60% is US and 40% is international. They used to do it 70% US and 30% international, but their research showed 60/40 to be a better split so they moved to it a few years ago.

You’ll notice that a 40% international allocation is between the 0% Bogle viewpoint and the 50% global weighting viewpoint, so it seems fine to me and that is what I do.

If you want another opinion, you can look at the TSP Lifecycle funds. You’ll notice that they do about a 70% US and 30% international split, like Vanguard used to do. Again, that seems reasonable.

Ultimately, you can pick anywhere from 0% to 50% and find someone really smart who agrees with you. I’d encourage you to have some exposure to international, so I’d say you should pick at least 20%, but it really is up to you.

Not sure what to do? Go with 30% (the TSP Lifecycle approach) or 40% (the Vanguard approach) for the I fund and call it a day.

How to Split the C and S Funds

This is easier, or at least I think it is. The C fund is basically an S&P 500 index fund of large companies, with the S fund having the rest of the small and medium sized companies. If you want to mirror the US stock market, you want to put about 75% of your US stock allocation in the C fund and the other 25% in the S fund. You’ll notice that this is what the TSP Lifecycle funds do, further backing up my assertion.

So, I recommend that you split your C and S fund allocation 75/25, respectively.

Putting the Stock Portion All Together

For the stocks, here’s the math:

- (Your desired international stock %) X (your total stock allocation %) = % that goes in the I fund

- (Your total stock allocation %) – (% you are putting in the I fund) = % you must divide into the C and S funds

- (Your % you must divide into the C and S funds) X 0.75 = % that goes in the C fund

- (Your % you must divide into the C and S funds) X 0.25 = % that goes in the S fund

Let’s use the 80% stock and 20% bond example we started with to illustrate. Let’s assume we’re going with a 40% desired allocation to international (like I personally use):

- (Desired international stock = 40%) X (total stock allocation = 80%) = 32% goes in the I fund

- (Total stock allocation = 80%) – (32% that is going in the I fund) = 48% we must divide into the C and S funds

- (48% we must divide into the C and S funds) X 0.75 = 36% that goes in the C fund

- (48% we must divide into the C and S funds) X 0.25 = 12% that goes in the S fund

That gives us a stock allocation of 32% I fund, 36% C fund, and 12% S fund.

The Bottom Line

We split our bond allocation 50/50 between the G and F funds. We put the desired percentage for international stocks in the I fund. We split the remaining stock allocation 75/25 between the C and S funds, respectively.

For the 80% stock and 20% bond portfolio we are using as an example, this plays out:

- 10% in the G fund

- 10% in the F fund

- 32% in the I fund (based on a hypothetical 60/40 US/international stock split, which can vary as discussed above)

- 36% in the C fund

- 12% in the S fund

This can be tough to grasp in a blog post, so if there are questions or points that need clarification just put them in the comments section and we’ll straighten them out.

The next step you need to crush the TSP is to decide if you’re going to go Roth or traditional.

If You Rent or Live on Base, You Need Renter’s Insurance

“If you rent an apartment or house, the idea of buying renter’s insurance…may not have crossed your mind. But it should have.” – Get a Financial Life: Personal Finance in Your Twenties and Thirties

It makes sense that if you rent you might need renter’s insurance. If you live on base, though, you might need it as well. For example, the Navy changed policy for people who live in Public Private Venture military housing. Renter’s insurance used to be included, but now it is not. The Air Force did the same in 2015. And as you can read in this Navy article, “All Sailors are encouraged to obtain renters insurance, however, regardless of where they choose to live.” The same is probably true for all others in the Department of Defense.

What is renter’s insurance?

Your landlord’s insurance won’t cover your personal belongings like furniture, clothing, and electronics if they are stolen or damaged. For that you need renter’s insurance, which protects your belongings and offers liability protection, similar to homeowner’s insurance used by homeowners.

The liability protection might be needed if someone injures themselves in your apartment and you are held liable. The renter’s insurance could cover their medical bills and any legal costs you have.

In addition, some policies will cover your expenses if something happens to your apartment/home and you cannot live there for a period of time.

What doesn’t renter’s insurance cover?

This will vary from policy to policy, but in general renter’s insurance will not cover flood damage. To find out if you are in a flood zone and need insurance, go to FloodSmart.gov. It might not cover tornado or earthquake damage either, so you’ll need to check. For info on earthquakes, go to EarthquakeAuthority.com.

Are there limits to the coverage?

As you might imagine, yes, there are limits. Your policy will provide insurance up to a certain amount. It could be $50,000 or $75,000 or whatever you pick and are paying the premium for.

In addition, each policy will either provide coverage for the current cash value or replacement costs. For example, assume you have a $2,000 computer that is 3 years old and is damaged in a fire. A replacement cost policy would give you whatever it costs to replace the computer with a new one, somewhere around $2,000. A cash value policy would only give you what the 3-year-old computer is actually worth, which is likely to be significantly less than $2,000.

Certain items, like expensive jewelry, often have a cap on their coverage. For example, if you have $5,000 of jewelry your policy might only cover up to $1,000 of it. If you want coverage for a particularly expensive item or items, you may need to purchase a “rider,” which is an additional coverage on the policy for specific items like jewelry, electronics, or fine art.

How much liability coverage do you need in your policy?

You should have at least as much liability coverage as your net worth. If you have a net worth north of $500K, you would need to purchase additional liability coverage in the form of umbrella liability insurance.

Do you always need renter’s insurance?

“What if you figure your personal possessions aren’t worth that much or replacing them won’t cause that much of a financial burden? If that’s the case, you may want to skip renter’s insurance – unless your landlord insists you get a policy as a condition of renting the apartment.” – Jonathan Clements Money Guide 2016

Even if this is true, though, you may need the liability coverage.

How can you make it less expensive?

There are a few ways you can reduce the cost of your renter’s insurance:

- Have as high a deductible as you can afford. Your deductible is the amount of money that you must pay before an insurance company will pay the rest of the insurance claim. In other words, if you sustain $2,000 of damage and your deductible is $500, then you would have to pay the first $500 and the insurance company would pay the additional $1,500. The higher your deductible, the cheaper your insurance policy is.

- Make sure you shop around, as prices will vary. I’d check out:

- Think before you file a small claim. If you have a $700 loss but a $500 deductible, you could get $200 from the insurance company if you filed, but they would probably see you as a higher-risk customer since you filed a claim and raise your rates, costing you much more than $200 over the long haul. Only file claims that are large losses you can’t afford.

- Ask about special discounts for safety features of your rental property like smoke detectors, fire sprinklers, security alarms, doormen, etc.

- Get multiple insurance policies you need from the same company. If you get your auto and renter’s insurance from the same company, you could get a discount.

Learn About Insurance with My Junk Mail

There are certain things in life that deserve their poor reputation, and one of those things is junk mail. It is called junk mail for a reason, and that reason is because it is junk. Trash it. Shred it. Recycle it. Burn it. Learn from it.

What? Learn from it?

Yes, learn from it.

Let’s learn about insurance by looking at some of my junk mail…

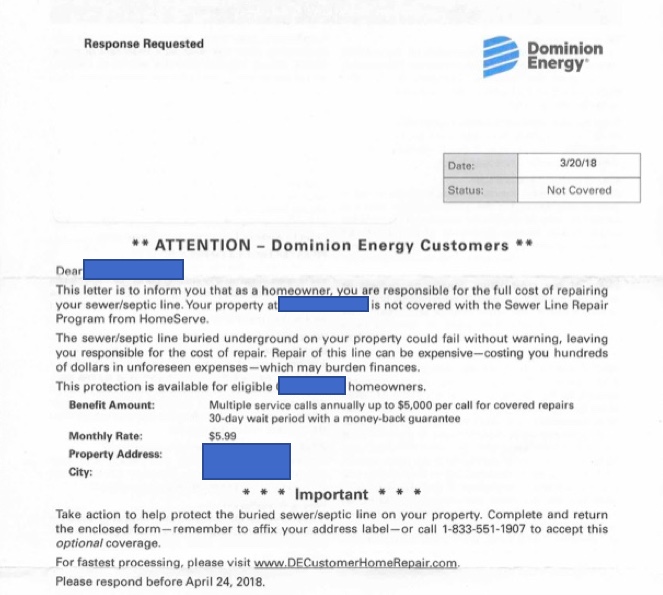

My Energy Company

Two years ago I received this letter from Dominion Energy, my energy company:

They are requesting a response from me, so I figured it had to be important.

I was dismayed to learn that my status was “Not Covered.” Everyone wants to be covered.

I read on to learn that I was fully responsible if my sewer or septic line would need repair and that this repair would cost hundreds of dollars. And that’s when I recycled this letter.

Actually, I didn’t recycle it but saved it for this post, but that is when I normally would have recycled the letter. Why?

The Purpose of Insurance

The purpose of insurance is to pay an insurance company to assume some risk that you cannot individually assume. For example, if I died my family would need a little more money than we currently have. Not much, but a little. I cannot assume this risk myself, so I pay an insurance company to assume this risk for me by buying term life insurance.

In the case of this junk mail, it is describing a risk (my sewer line needs repairs) that I CAN shoulder myself because apparently it only costs “hundreds of dollars.”

They say it “may burden finances.” Not mine.

But they cover up to $5,000 of repairs…that’s a lot!

Not for me. So I’m not buying this insurance.

Central Lesson of This Blog Post – You only buy insurance for risks you cannot personally assume.

Example #2 – Pet Insurance

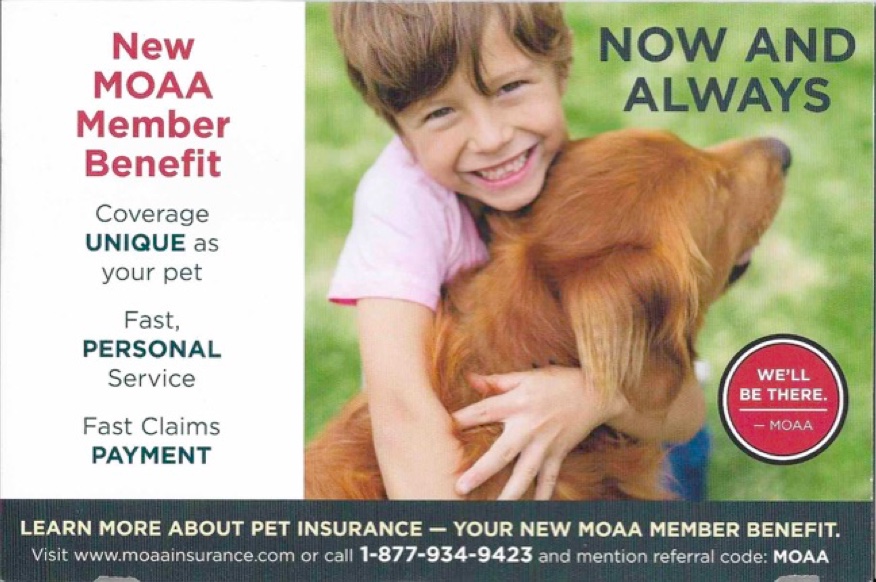

I love the Military Officers Association of America. It is great organization, and I’m a lifetime member. They are looking out for us in Congress, and they provide very thorough updates on what is going on with military and veterans benefits. I’d highly recommend you join if eligible. But they sent me this:

Hey, I’m all about pets. In fact, I have a golden retriever just like in this postcard. But I’m not buying pet insurance. Why?

Because of the…

Central Lesson of This Blog Post – You only buy insurance for risks you cannot personally assume.

Yes, you guessed it. I have pets (two dogs), but if something happens to them I can pay the bills. Therefore, I don’t need pet insurance.

Your Insurance Needs Will Change as You Age

At different times in your life you’ll have different insurance needs. When I was younger and had a lower net worth, there were risks I could not afford to assume. As a result, I had:

- A larger life insurance policy.

- Supplemental disability insurance on top of the military disability system.

- Lower deductibles on my insurance policies.

Now due to my higher net worth, I have:

- Umbrella liability insurance.

- The highest deductibles USAA will allow on all of my insurance policies.

- Much less life insurance.

- Cancelled my supplemental disability insurance.

Here you can read all about getting properly insured.

Regularly Reevaluate Your Insurance Needs

Once a year I call USAA and reevaluate my insurance needs. Because there have probably been changes to the risks I can afford to bear, and I remember the…

Central Lesson of This Blog Post – You only buy insurance for risks you cannot personally assume.

More Articles on the Social Security Tax Deferral

Here are some more articles about the Social Security tax deferral:

Order Gives Employees Social Security Withholding Tax Deferral, Not Forgiveness

Payroll Tax Deferral Takes Effect for Service Members

Troops, DoD Civilians Won’t Be Able to Opt Out of Payroll Tax Deferral Plan

Trump promises to erase troops’ 2021 deferred tax debt, but lawmakers say he can’t