Learn About Insurance with My Junk Mail

There are certain things in life that deserve their poor reputation, and one of those things is junk mail. It is called junk mail for a reason, and that reason is because it is junk. Trash it. Shred it. Recycle it. Burn it. Learn from it.

What? Learn from it?

Yes, learn from it.

Let’s learn about insurance by looking at some of my junk mail…

My Energy Company

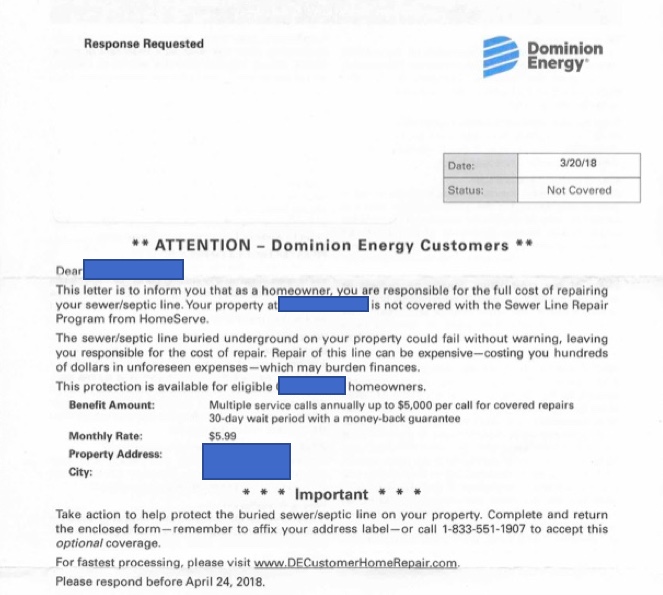

Two years ago I received this letter from Dominion Energy, my energy company:

They are requesting a response from me, so I figured it had to be important.

I was dismayed to learn that my status was “Not Covered.” Everyone wants to be covered.

I read on to learn that I was fully responsible if my sewer or septic line would need repair and that this repair would cost hundreds of dollars. And that’s when I recycled this letter.

Actually, I didn’t recycle it but saved it for this post, but that is when I normally would have recycled the letter. Why?

The Purpose of Insurance

The purpose of insurance is to pay an insurance company to assume some risk that you cannot individually assume. For example, if I died my family would need a little more money than we currently have. Not much, but a little. I cannot assume this risk myself, so I pay an insurance company to assume this risk for me by buying term life insurance.

In the case of this junk mail, it is describing a risk (my sewer line needs repairs) that I CAN shoulder myself because apparently it only costs “hundreds of dollars.”

They say it “may burden finances.” Not mine.

But they cover up to $5,000 of repairs…that’s a lot!

Not for me. So I’m not buying this insurance.

Central Lesson of This Blog Post – You only buy insurance for risks you cannot personally assume.

Example #2 – Pet Insurance

I love the Military Officers Association of America. It is great organization, and I’m a lifetime member. They are looking out for us in Congress, and they provide very thorough updates on what is going on with military and veterans benefits. I’d highly recommend you join if eligible. But they sent me this:

Hey, I’m all about pets. In fact, I have a golden retriever just like in this postcard. But I’m not buying pet insurance. Why?

Because of the…

Central Lesson of This Blog Post – You only buy insurance for risks you cannot personally assume.

Yes, you guessed it. I have pets (two dogs), but if something happens to them I can pay the bills. Therefore, I don’t need pet insurance.

Your Insurance Needs Will Change as You Age

At different times in your life you’ll have different insurance needs. When I was younger and had a lower net worth, there were risks I could not afford to assume. As a result, I had:

- A larger life insurance policy.

- Supplemental disability insurance on top of the military disability system.

- Lower deductibles on my insurance policies.

Now due to my higher net worth, I have:

- Umbrella liability insurance.

- The highest deductibles USAA will allow on all of my insurance policies.

- Much less life insurance.

- Cancelled my supplemental disability insurance.

Here you can read all about getting properly insured.

Regularly Reevaluate Your Insurance Needs

Once a year I call USAA and reevaluate my insurance needs. Because there have probably been changes to the risks I can afford to bear, and I remember the…

Central Lesson of This Blog Post – You only buy insurance for risks you cannot personally assume.