personal finance

It’s Easy to Get Rich in the Military

The title says it all. Many people would disagree with this statement, but I know it is true. Here are a few ways I know of to get rich in the military:

- Stay in for the pension – Many civilians work 40+ years before they can retire. You only have to stay in for 20 years to retire with an inflation adjusted lifetime pension. It’s even tax free in some states. You might not realize it, but the value of the pension alone can make you rich. According to the Department of Defense, the value of a 20 year pension for an O5 at 20 years, the value is $1.46 million. Combine this pension with regular savings in the Thrift Savings Plan, and you’re automatically a multimillionaire.

- Live frugally and become a super saver – There are a few advantages you’ve got that will allow you to live frugally and sock away more of your income. They include government housing or a tax free housing allowance, government subsidized meals (Basic Allowance for Subsistence), free medical and dental care, on base services (exchanges, commissaries, gyms, auto shops, child care, etc.), uniforms to wear instead of expensive clothes, military discounts, USAA insurance, and no income lapse when you change jobs.

- Purchase houses or condos at each of your duty stations and turn them into rental properties – The details of doing this are complicated, and not everyone wants to be a landlord/real estate investor nor will it make economic sense in all duty stations. You have to purchase your properties as if they are an investment, but if you are motivated and the economics make sense you can turn the downside of frequent moves into an upside. A potentially very lucrative upside.

- Use special programs for veteran entrepreneurs – There are many programs available that help veterans with an entrepreneurial spirit. Own your own business or side hustle and become wealthy.

A few upcoming blog posts will discuss each of these in detail.

Finance Friday Articles

Here are this week’s articles:

- 4 Great Ways to Protect Your Real Estate Assets

- Don’t Buy Stuff You Can’t Afford

- Going Soft

- How to Get Rich Faster

- Long-Term Real Estate Returns

- Marginal Tax Rate or Effective Tax Rate?

- My Favorite Investment Writing of 2020

- Next Year Foretold

- Radiology and the Private Equity Bait and Switch

- Split the Difference

- Top 5 Reasons to Exceed 25 Years of Expenses Before Retiring

- Why Early Retirees Should Max Out Retirement Accounts

Throwback Thursday Classic Post – TSP Fund Deep Dive – The Lifecycle Funds – Hitting the Easy Button

Target date funds are popular. You just pick the approximate year you want to retire, and you invest in the fund that has a year close to that in its name. Nothing could be easier!

Let’s take a look at the Thrift Savings Plan’s (TSP) target date funds – the Lifecycle Funds or L Funds.

Inception Date

1 AUG 2005

Fund Management

The L Funds are invested in the five individual TSP funds based on professionally determined asset allocations.

Investment Strategy

To provide professionally diversified portfolios based on various time horizons, using the G, F, C, S, and I Funds. The objective is to strike an optimal balance between the expected risk and return associated with each fund.

The L Funds’ strategy is to invest in an appropriate mix of the G, F, C, S, and I Funds for a particular time horizon, or target retirement date. The investment mix of each L Fund becomes more conservative as its target date approaches.

The strategy assumes that:

- The greater the number of years you have until retirement, the more willing and able you are to tolerate risk (fluctuation) in your TSP account value to pursue higher rates of return.

- For a given risk level and time horizon, there is an optimal mix of the G, F, C, S, and I Funds that provides the highest expected return.

Each quarter, the L Funds’ target asset allocations change, moving towards a less risky mix of investments as the target date approaches. So if you are invested in one of the L Funds, you will notice that as you get closer to your target date, your allocation to the riskier TSP funds will get smaller while your allocation to the more conservative G Fund gets larger.

The rate of change in the target asset allocation is small when the L Fund target dates are in the distant future. The rate increases as the funds approach their target dates.

When an L Fund has reached its target date, it will be rolled into the L Income Fund. The L Income Fund:

- Is the most conservative of the L Funds.

- Focuses on capital preservation while providing a small exposure to the TSP’s riskier assets (C, S, and I Funds) in order to reduce inflation’s effect on your purchasing power.

- Is designed to produce current income for participants who plan to start withdrawing from their TSP accounts in the near future and for those who are already receiving monthly payments from their accounts.

- Has a set asset allocation that does not change over time.

- The progression from a target date L Fund to the L Income Fund is automatic.

New Lifecycle funds will be added for distant target dates as they are needed.

What is the Risk?

Investors in the L Funds are exposed to all of the types of risk to which the individual TSP funds are exposed. Your account is not guaranteed against loss. The L Funds can have periods of gain and loss, just as the individual TSP funds do.

What is the Benefit?

The L Funds simplify fund selection, and investment risk is reduced through diversification among the five individual TSP funds. You choose the fund that is closest to your target date (or, if your target date falls between the target dates that are offered, you can split your account between the two target date funds closest to your time horizon).

When you invest in the L Funds:

- You can be sure that your TSP account is broadly diversified.

- You don’t have to remember to adjust your investment mix as your target date approaches – it’s done for you.

If you want to see the historical performance of the five L Funds or a visual representation of how the asset allocations change over time, go to this page and click on the funds you want to examine. Here you can see I clicked the L 2030, 2035, and 2040:

Types of Earnings

The L Funds earn the weighted average of the earnings of the underlying G, F, C, S, and I Funds calculated in proportion to their L Fund allocation.

Expenses

The net expenses paid by investors is ridiculously low and is a major benefit of the TSP.

How Should I Use the L Funds in my TSP Account?

Use the L Funds if you are looking for a simple, low maintenance way of investing money in your TSP account. The L Funds make the investing process easy for you because you do not have to figure out how to diversify your account or how and when to rebalance.

The L Funds are designed so that 100% of your TSP account can be invested in the single L Fund that most closely matches your time horizon (or in the two L Funds closest to your time horizon). Any other use of the L Funds may result in a greater amount of risk in your portfolio than is necessary in order to achieve the same expected rate of return.

Determine the date when, after leaving Federal service, you will need the money that is in your TSP account. Then identify the L Fund that most closely matches your target date.

Advice from One of My Favorite Short Investing Books

Here is what one of my favorite investing books, The Little Book of Common Sense Investing: The Only Way to Guarantee Your Fair Share of Stock Market Returns (Little Books. Big Profits), says about target retirement date funds like the L Funds:

Target-date funds can be an excellent choice, not only for investors who are just getting started with their investment programs, but also for investors who decide to adopt a simple strategy for funding their retirement.

Pay Plan Update and Finance Friday Articles

The FY21 pay plan is currently still under review. Our best guess is that it is not signed until early 2021, but that is simply a guess.

As for questions about increases in board certified pay and other physician pays, that language was in NDAA 21 drafts. At this point, what the final NDAA says or when it gets signed is anyone’s guess.

Just to end on a positive note, you all look amazing today!

Here are this week’s articles:

Size Does Matter (For Your Expense Ratio)

Whether you are managing your investments by yourself or getting help, you need to understand one critical concept, the expense ratio of your investments. Every mutual fund and exchange-traded fund (ETF) has an expense ratio, and keeping it as small as possible is key to your long-term financial success. Size does matter.

What is an Expense Ratio?

An expense ratio is the percentage of a fund’s assets that is used for expenses. In other words, if you invest in a mutual fund with a 1% expense ratio and that fund makes 10%, you’ll only get a 9% return on your investment because 1% goes to pay expenses. The less of your return you use to pay expenses, the more you get to keep.

What is an average expense ratio? An average stock mutual fund has an expense ratio of about 0.60%, but the expense ratios for mutual funds that are similar in their composition can vary wildly. For example, if you look at a list of Standard & Poor 500 index funds offered by investment companies, you’d find low expense ratios like 0.03% and as high as 1.36% (or even higher). While 1.33% does not seem like that large of a difference, keep in mind that costs last forever and that small differences compounded over years will cost you a lot of money. That is one of the major benefits of the TSP – its industry leading low cost – where nearly all the funds have expense ratios of 0.04%.

Love Your Grandparents

Let’s pretend that when you are 25 years old your grandparents give you $10,000 to invest in an S&P 500 index fund for 50 years, during which you earn a 9.5% return. If you invested in an index fund with the 1.36% expense ratio, you would have $500,000. That sounds pretty good! However, if you invested in a low cost fund with a 0.03% expense ratio, you would have $921,000.

That 1.33% difference in the expense ratios cost you $421,000!

Small differences in expenses can make huge differences in long-term investment returns, so you need to pay attention to the expense ratios of your investments.

This difference is even more dramatic when you compare actively managed funds to passively managed index funds. Because actively managed funds have higher expense ratios than index funds, it is very difficult for an active manager to beat his/her comparative index over the long-term. This is why I invest 100% in index funds, like they have in the TSP.

Shop Around

When you are picking your investments, keep in mind that you can’t control what happens to the market, but you can control which investments you choose and the expenses that they charge. Any time you are looking to invest in a mutual fund or ETF, you should search for similar funds and compare expense ratios, which you should try to keep below 0.5% (or even 0.25%, if possible).

When investing outside of the TSP, make sure that at a minimum you take a look at the Vanguard version of the investment you are considering since their expense ratios are the lowest in the industry and they never charge extraneous fees, like loads.

There is no reason to pay more expenses for what is essentially the same investment product. The size of your expense ratio matters. It could cost you A TON of money over the long-term.

How Much Do You Get Paid as a Navy Doctor?

I received a few e-mails asking for help figuring out physician pay in the Navy, and this is a long overdue blog post. In the spreadsheet below is the pay info for the various stages as you move throughout your Navy Medical Corps Career. I’m making a few assumptions:

- These are FY20 pay numbers (since the FY21 pay plan is not out yet).

- You promote at the normal times (O4 at 6 years, O5 at 12 years, and O6 at 18 years).

- Basic Allowance for Housing is with dependents in San Diego. You can personalize this here.

- The specialty is Emergency Medicine. You can look at the different amounts for other specialties here.

- You pass your boards and become board-certified after residency.

For those who don’t want to look at the spreadsheet, here are the bottom line annual salaries:

- New O3 intern – $95,976

- O3 GMO – $121,803

- Mid-grade O3 EM Resident – $120,348

- New O4 EM Attending – $180,249

- O5 EM Attending on a 6-Year Retention Bonus – $264,665

- O6 EM Attending on a 6-Year Retention Bonus – $287,878

Here’s the spreadsheet with hyperlinks:

Winning the Game

By all accounts, I’ve won the game. I know the income my family needs to live our desired lifestyle. I have an inflation-adjusted Navy pension in my future. I have two children and two GI Bills, one for each child. My house is paid off and I’m debt-free. Combine all of this with the 4% rule, and it seems I have enough to produce our desired income for the rest of my life. I have “won the game.”

Noted investment manager, neurologist, and author Bill Bernstein recommends that—once you’ve won the game—you should stop playing. What exactly does that mean? Bernstein suggests you dramatically reduce the risk you are taking with your retirement portfolio. To him, there’s no sense in taking risk you don’t need to take.

Although his advice makes sense, I find it hard to implement. First, I won the game by playing. I’m used to playing. I like playing. I want to play more. I’m only 45 and too young to stop playing. If I stop playing, I’ll be bored. As I mentioned, I have an inflation-adjusted military pension coming my way. The pension has no principal left over after my wife and I die, but it is a government guaranteed, inflation-adjusted source of income. What exactly does Bernstein mean when he says “stop playing”?

In a 2015 article that Bernstein wrote for The Wall Street Journal, he said, “You’ve won when you’ve acquired enough assets to provide your basic living expenses for the rest of your life.” Simple enough. My military pension, investments, and Social Security seem to meet this requirement. I guess I’ve won.

To stop playing, you reduce the risk you’re taking with your retirement portfolio. Once you’ve accumulated enough to support your retirement, Bernstein suggests you purchase a TIPS ladder. TIPS are Treasury Inflation Protected Securities, government-issued bonds that increase in value along with inflation, while also paying a little interest on top of that (although currently TIPS yields are negative). You can create a TIPS ladder by buying individual bonds at TreasuryDirect.gov.

For example, if you needed $60,000 per year for your basic expenses, you might take five years of required spending—or $300,000—and buy five $60,000 TIPS, with one maturing in each of the next five years. When one matured, you’d use that money for your expenses for the next year. At the same time, you’d purchase another $60,000 bond that matures five years from now. Rinse, wash and repeat.

If you didn’t want to buy individual bonds and were okay with the small fees they charge, you could likely get the same effect by investing $300,000 in the Vanguard Short-Term Inflation-Protected Securities Index Fund Admiral Shares (VTAPX) or a similar low-cost offering at another investment firm. Bernstein doesn’t recommend this, because of the fees.

I’ve decided my inflation-adjusted military pension is the equivalent of a TIPS ladder, which means that according to Dr. Bernstein I’m no longer playing.

Are you staying in long enough to get the pension? Maybe you’ve won the game too.

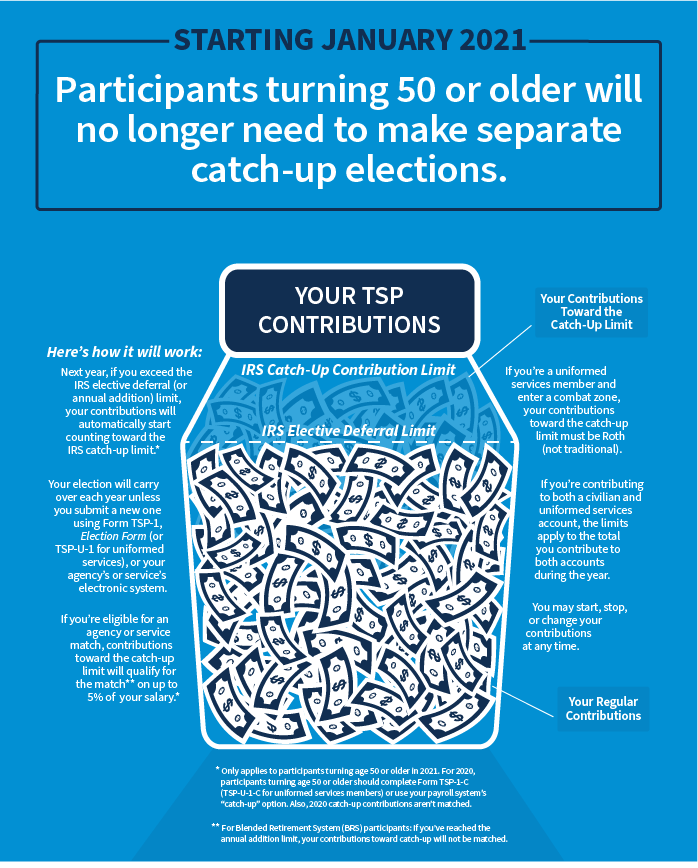

Change to TSP Catch-Up Contributions and Finance Friday Articles

Catch-up contributions are changing — Starting in January 2021, the process for catch-up contributions will be easier for TSP participants. If you’re turning age 50 or older, you’ll no longer need to make separate catch-up elections to your TSP account to contribute toward the catch-up limit.

Here’s how it will work:

- If you reach the IRS elective deferral or annual addition limit before the end of the year and keep saving, your contributions will automatically continue toward the catch-up limit.

- Contributions spilling over toward the catch-up limit will qualify for the match on up to 5% of salary.

- The contribution amount you choose will continue each year unless you change it.

Learn how to make catch-up contributions next year.

Also, there is an image at the end of the post to help.

Here are this week’s articles:

- 5 Reasons I Prefer Real Estate Over Stocks

- 10 Ways to Pay Off a Mortgage Quickly

- For Goodness Sake

- How To Become a Successful Landlord as a Physician

- How to Score Cheap Flights

- The Most Important Assumption

- Trends That End

- What’s wrong with Target Date Funds?

Throwback Thursday Classic Post: TSP Fund Deep Dive – The G Fund – Free Lunches Do Exist

There are only five investments available in the Thrift Savings Plan (TSP), so let’s take a detailed look at them one at a time. In this post we’ll cover the G Fund.

The G Fund is proof that free lunches do actually exist because in the G Fund the government is paying you more interest than they actually should. Read on to find out how and why.

Inception Date

1 APR 1987

Fund Management

Unlike the other TSP funds that are managed by Blackrock, the G Fund is managed internally by the Federal Retirement Thrift Investment Board. The G Fund buys a non-marketable U.S. Treasury security that is guaranteed by the U.S. Government. This means that the G Fund will not lose money.

Investment Strategy

The G Fund invests exclusively in a non-marketable short-term U.S. Treasury security that is specially issued to the TSP. The earnings consist entirely of interest income on the security.

The G Fund’s investment objective is to produce a rate of return that is higher than inflation while avoiding exposure to credit (default) risk and market price fluctuations. It is designed to provide investors with interest income without risk of loss of principal.

What is the Risk?

Your investment in the G Fund is subject to inflation risk, meaning your G Fund investment may not grow enough to offset the reduction in purchasing power that results from inflation.

What is the Benefit?

The payment of G Fund principal and interest is guaranteed by the U.S. Government. This means that the U.S. Government will always make the required payments. In other words, your G Fund investment is not subject to credit (default) risk.

The G Fund interest rate calculation is based on the weighted average yield of all outstanding Treasury notes and bonds with 4 or more years to maturity. As a result, participants who invest in the G Fund are rewarded with a long-term rate on what is essentially a short-term security. Generally, long-term interest rates are higher than short-term rates. This is the free lunch that the government periodically talks about getting rid of.

The G Fund is the lowest risk fund in the TSP and will have the lowest volatility, as you can see below. The major benefit is that you are guaranteed not to lose money. In trade for this you are receiving lower returns. Here is all the performance data as of 21 NOV 2020:

Types of Earnings

The G Fund makes money for its investors with interest paid by the U.S. Government.

Expenses

The net expenses paid by investors is 0.043% or 4.3 basis points, which like all the TSP funds is ridiculously low and is a major benefit of the TSP. It costs $0.43 for each $1,000 invested. You won’t find a lower cost U.S. government bond fund anywhere.

How Should I Use the G Fund in my TSP Account?

Consider investing in the G Fund if you would like to have all or a portion of your TSP account completely protected from loss. If you choose to invest in the G Fund, you are placing a higher priority on the stability and preservation of your money than on the opportunity to potentially achieve greater long-term growth in your account through investment in the other TSP funds.

It is the TSP equivalent of a U.S. Treasury bond fund you’d find at Vanguard or other investing firms.

Advice from My Favorite Short Investing Book

Here is what my favorite investing book, The Elements of Investing: Easy Lessons for Every Investor, says about U.S. government bond index funds like the G Fund:

The U.S. Treasury issues large amounts of bonds. These issues are considered the safest of all and these bonds are the one type of security where diversification is not essential…High quality bonds can moderate the risk of a common stock portfolio by providing offsetting variations to the inevitable ups and downs or the stock market.

If you want to know how to integrate the G fund into your own TSP investments, read the Crush the TSP series. In particular, step 3 tells you how to figure out how much of your portfolio to devote toward bonds.

Invest Your Taxable Account Thoughtfully

Jonathan Clements was a longtime personal finance columnist for The Wall Street Journal, and he offers great advice at the best price you can get (free) on his blog Humble Dollar. Here is one piece of advice from his site:

“INVEST YOUR TAXABLE ACCOUNT THOUGHTFULLY. If you purchase the wrong investments in your taxable account, you may be reluctant to sell, because you’ll trigger capital gains taxes. A good choice: low-cost U.S. and international total stock market index funds, which should be tax-efficient—and which shouldn’t ever lag far behind the market averages.”

For those of us in the military, investing in a taxable account comes into play in a few scenarios…

Scenario #1 – You and your spouse (if you have one) have filled your Thrift Savings Plan (TSP) and all other retirement accounts available including IRAs, yet you want to save more for retirement. In this case, you put the rest in a taxable account with the investment company of your choice (Vanguard, Fidelity, Schwab, etc.). This is what I do when all of my retirement accounts are full, and just like Jonathan mentions I invest purely in broad, low-cost index funds at Vanguard. The only taxable holdings I have are the Vanguard U.S. and international total stock market index funds.

Scenario #2 – You are saving for a financial goal that is not related to retirement, such as a downpayment on a home or for a new car. If you’re saving for college, you’d use a 529 plan, but for just about anything else you could use a taxable account. For example, you could put your emergency money and extra spending money in a money market fund among your taxable accounts. The alternative to this is to use a bank and invest in a high-yield savings account (which is what I do), a certificate of deposit (CD), or a money market account. Bankrate.com will show you the best rates for each of these reasonable alternatives.

If you are using a taxable account, there are a few things to consider. If you are investing in bonds, you may want to invest in municipal bonds in your taxable account due to the tax benefits. If you are a fan of target date funds, you may not want to use them in a taxable account because the bond portion will kick off income that is taxed at your full marginal tax rate. This is less of an issue with bond yields being low right now, but most experts feel that bonds are better placed in a tax-advantaged retirement account unless you are using municipal bonds.