Throwback Thursday Classic Post – TSP Fund Deep Dive – The Lifecycle Funds – Hitting the Easy Button

Target date funds are popular. You just pick the approximate year you want to retire, and you invest in the fund that has a year close to that in its name. Nothing could be easier!

Let’s take a look at the Thrift Savings Plan’s (TSP) target date funds – the Lifecycle Funds or L Funds.

Inception Date

1 AUG 2005

Fund Management

The L Funds are invested in the five individual TSP funds based on professionally determined asset allocations.

Investment Strategy

To provide professionally diversified portfolios based on various time horizons, using the G, F, C, S, and I Funds. The objective is to strike an optimal balance between the expected risk and return associated with each fund.

The L Funds’ strategy is to invest in an appropriate mix of the G, F, C, S, and I Funds for a particular time horizon, or target retirement date. The investment mix of each L Fund becomes more conservative as its target date approaches.

The strategy assumes that:

- The greater the number of years you have until retirement, the more willing and able you are to tolerate risk (fluctuation) in your TSP account value to pursue higher rates of return.

- For a given risk level and time horizon, there is an optimal mix of the G, F, C, S, and I Funds that provides the highest expected return.

Each quarter, the L Funds’ target asset allocations change, moving towards a less risky mix of investments as the target date approaches. So if you are invested in one of the L Funds, you will notice that as you get closer to your target date, your allocation to the riskier TSP funds will get smaller while your allocation to the more conservative G Fund gets larger.

The rate of change in the target asset allocation is small when the L Fund target dates are in the distant future. The rate increases as the funds approach their target dates.

When an L Fund has reached its target date, it will be rolled into the L Income Fund. The L Income Fund:

- Is the most conservative of the L Funds.

- Focuses on capital preservation while providing a small exposure to the TSP’s riskier assets (C, S, and I Funds) in order to reduce inflation’s effect on your purchasing power.

- Is designed to produce current income for participants who plan to start withdrawing from their TSP accounts in the near future and for those who are already receiving monthly payments from their accounts.

- Has a set asset allocation that does not change over time.

- The progression from a target date L Fund to the L Income Fund is automatic.

New Lifecycle funds will be added for distant target dates as they are needed.

What is the Risk?

Investors in the L Funds are exposed to all of the types of risk to which the individual TSP funds are exposed. Your account is not guaranteed against loss. The L Funds can have periods of gain and loss, just as the individual TSP funds do.

What is the Benefit?

The L Funds simplify fund selection, and investment risk is reduced through diversification among the five individual TSP funds. You choose the fund that is closest to your target date (or, if your target date falls between the target dates that are offered, you can split your account between the two target date funds closest to your time horizon).

When you invest in the L Funds:

- You can be sure that your TSP account is broadly diversified.

- You don’t have to remember to adjust your investment mix as your target date approaches – it’s done for you.

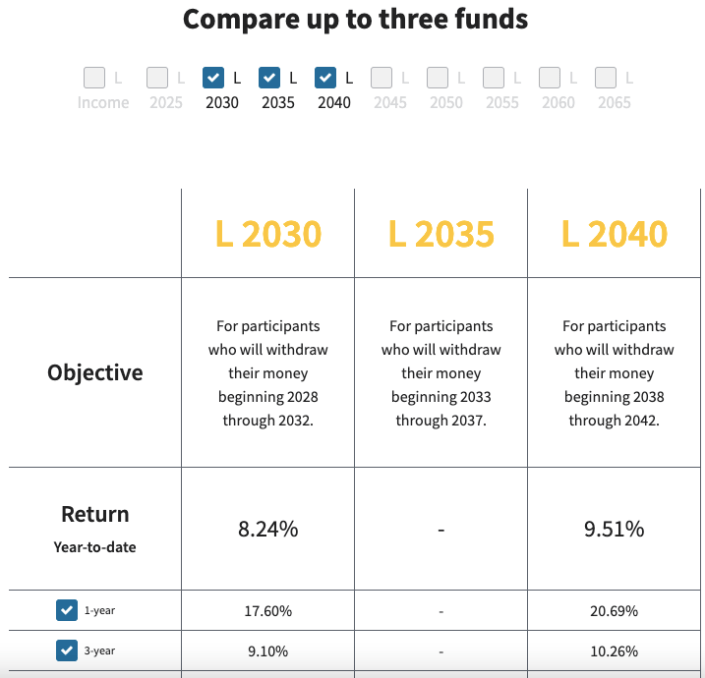

If you want to see the historical performance of the five L Funds or a visual representation of how the asset allocations change over time, go to this page and click on the funds you want to examine. Here you can see I clicked the L 2030, 2035, and 2040:

Types of Earnings

The L Funds earn the weighted average of the earnings of the underlying G, F, C, S, and I Funds calculated in proportion to their L Fund allocation.

Expenses

The net expenses paid by investors is ridiculously low and is a major benefit of the TSP.

How Should I Use the L Funds in my TSP Account?

Use the L Funds if you are looking for a simple, low maintenance way of investing money in your TSP account. The L Funds make the investing process easy for you because you do not have to figure out how to diversify your account or how and when to rebalance.

The L Funds are designed so that 100% of your TSP account can be invested in the single L Fund that most closely matches your time horizon (or in the two L Funds closest to your time horizon). Any other use of the L Funds may result in a greater amount of risk in your portfolio than is necessary in order to achieve the same expected rate of return.

Determine the date when, after leaving Federal service, you will need the money that is in your TSP account. Then identify the L Fund that most closely matches your target date.

Advice from One of My Favorite Short Investing Books

Here is what one of my favorite investing books, The Little Book of Common Sense Investing: The Only Way to Guarantee Your Fair Share of Stock Market Returns (Little Books. Big Profits), says about target retirement date funds like the L Funds:

Target-date funds can be an excellent choice, not only for investors who are just getting started with their investment programs, but also for investors who decide to adopt a simple strategy for funding their retirement.