personal finance

Asset Location

Here’s a tip on asset location from one of my favorite blogs and authors, Jonathan Clements from Humble Dollar:

After deciding what investments to buy, we should consider asset location. What’s that? It involves divvying up investments between taxable and retirement accounts. If investments generate large annual tax bills—think taxable bonds and actively managed funds—we’ll typically want to hold them in a retirement account.

Jonathan’s advice is the traditional advice. Put your taxable bonds, like the Thrift Savings Plan (TSP) F and G funds, into your retirement accounts. This is what I do. My F and G funds are in the TSP, clearly a retirement account, and my international bonds (which they don’t have in the TSP) are in an individual retirement account (IRA).

I don’t own actively managed funds, and I also don’t invest in real estate investment trusts (REITs), although I have in the past and I think about it pretty frequently.

There is another school of thought, though. The White Coat Investor has a different take. You can read about them in his posts entitled My Two Asset Location Pet Peeves and Bonds Go in Taxable!

Of note, just about everyone says to put actively managed funds or REITs in a retirement account, so you won’t find any arguments there.

If you’re really interested in this concept/discussion, the Bogleheads Wiki on tax efficient fund placement is a great read as well.

Will the Government Ever Get Rid of the “Free Lunch” of the TSP G Fund?

They say there’s no free lunch, but in the Thrift Savings Plan there is a free lunch, and it’s called the G Fund. Will the government get rid of this free lunch?

The G Fund Free Lunch

What is this free lunch? You can read about it on this page in the Rewards section:

The G Fund interest rate calculation is based on the weighted average yield of all outstanding Treasury notes and bonds with 4 or more years to maturity. As a result, participants who invest in the G Fund are rewarded with a long-term rate on what is essentially a short-term security. Generally, long-term interest rates are higher than short-term rates.

The government is paying you a higher interest rate than it should. That is the G Fund free lunch.

Why is the Free Lunch at Risk?

The government periodically considers getting rid of it. For example, you can read about it in this article, which is discussing the President’s FY19 budget plan/request. Here’s the relevant portion:

The plan also proposes reducing the statutorily mandated rate of return for the government securities (G) fund to be based on either the three-month or four-week Treasury bill, at a projected savings of $8.9 billion over 10 years.

“G Fund investors benefit from receiving a medium-term Treasury Bond rate of return on what is essentially a short-term security,” the White House wrote. “The budget would instead base the G-fund yield on a short-term T-bill rate.”

TSP spokeswoman Kim Weaver said changing the G Fund’s yield, which is currently 2.75 percent annually, would have a disastrous effect on participants’ ability to save for retirement. If Congress changed the G Fund to track the three-month Treasury bill, the yield would decrease to 1.46 percent, and for the four-week bill it would drop to 1.43 percent.

“Such a change would make the G Fund inadequate and ineffective from an investment standpoint for TSP participants who are saving for retirement,” Weaver said in an email. “More than 3.6 million TSP participants (69 percent) have all or some of their account balance invested in the G Fund. Of those with money in the G Fund, 2 million (39 percent) hold the G Fund as their sole investment choice.”

For a TSP participant who has just retired and is invested entirely in the L Income Fund, which is designed for people who have begun taking annuity payments, they would run out of money at age 84 instead of the current projected age of 92, Weaver said.

Jessica Klement, staff vice president for advocacy at the National Active and Retired Federal Employees Association, said the change would make G Fund investments “useless” and likely force TSP administrators to divest from it entirely.

“[The new rate] would not even keep up with inflation,” she said. “So if you wanted to keep your money in a mostly secure fund, you would not be getting any return, and you’d actually be losing money. And if you took your money out, there would be no other safe, secure investment for those nearing or in retirement.”

What Does This Mean For You?

Right now, it means nothing. This is all just discussion about something that might happen in the future.

What you do need to understand, though, is that the G Fund serves a specific purpose in your portfolio. As the TSP site says:

Consider investing in the G Fund if you would like to have all or a portion of your TSP account completely protected from loss. If you choose to invest in the G Fund, you are placing a higher priority on the stability and preservation of your money than on the opportunity to potentially achieve greater long-term growth in your account through investment in the other TSP funds.

It is alarming that Ms. Weaver from the TSP said, “Of those with money in the G Fund, 2 million (39 percent) hold the G Fund as their sole investment choice.” Those 2 millions people are sacrificing long-term growth for the safest and most conservative investment available in the TSP.

There’s nothing wrong with that if you’re doing it because you are very conservative, near retirement, or the G Fund serves as the bond portion of a larger, more diversified portfolio that has more risky assets like stocks or real estate.

The sad reality is that most who are solely invested in the G Fund are that way because it used to be the default option for those starting a TSP account, and they never switched it to a more aggressive investment option. Under the new Blended Retirement System, the default investment switched from the G Fund to an age-appropriate Lifecycle fund.

What’s the Bottom Line?

The G Fund gives you a free lunch, paying you a higher long-term interest rate while you are investing in short-term securities. The government periodically talks about getting rid of that free lunch.

If you are invested in the G Fund, make sure you are doing it purposely and are aware of its conservative nature. Its emphasis is on preserving wealth rather than growing wealth.

Check Your Beneficiary Designations

Here’s a tip from one of my favorite blogs and authors, Jonathan Clements from Humble Dollar:

CHECK YOUR BENEFICIARY DESIGNATIONS. Your retirement accounts and life insurance will typically pass to the beneficiaries specified on those accounts, not the people named in your will. If your family situation has changed, or you simply don’t remember who you listed, take a moment to review your beneficiary designations.

Don’t let the ex-spouse get your money when you die! Update your beneficiaries.

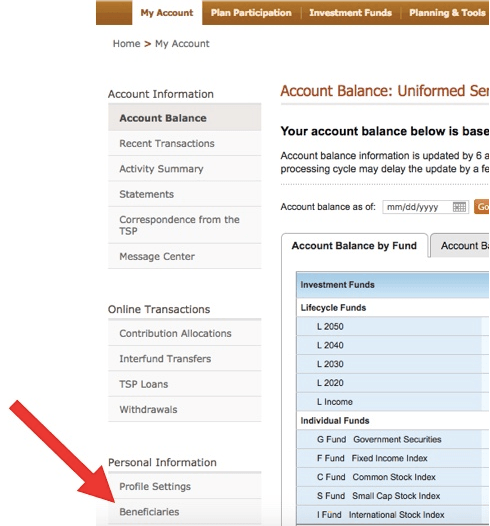

How to See Your Beneficiaries for the Thrift Savings Plan (TSP)

If you log on to the TSP page, you need to click on the link along the lower left, marked by the large red arrow:

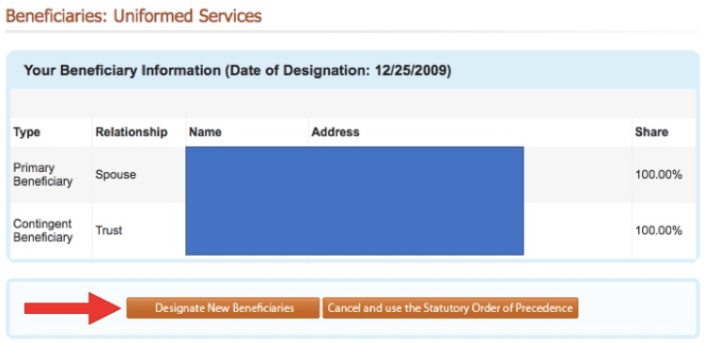

Then you’ll see this, and you can change them at the bottom:

Then you’ll see this, and you can change them at the bottom:

Invest in Your Taxable Account Thoughtfully

Here’s a tip on investing in your taxable account from one of my favorite blogs and authors, Jonathan Clements from Humble Dollar:

INVEST YOUR TAXABLE ACCOUNT THOUGHTFULLY. If you purchase the wrong investments in your taxable account, you may be reluctant to sell, because you’ll trigger capital gains taxes. A good choice: low-cost U.S. and international total stock market index funds, which should be tax-efficient—and which shouldn’t ever lag far behind the market averages.

For those of us in the military, investing in a taxable account comes into play in a few scenarios…

Scenario #1 – You and your spouse (if you have one) have filled your Thrift Savings Plan (TSP) and all other retirement accounts available including IRAs, yet you want to save more for retirement. In this case, you put the rest in a taxable account with the investment company of your choice (Vanguard, Fidelity, Schwab, etc.). This is what I do when all of my retirement accounts are full, and just like Jonathan mentions I invest purely in broad, low-cost index funds at Vanguard. The only taxable holdings I have are the Vanguard U.S. and international total stock market index funds.

Scenario #2 – You are saving for a financial goal that is not related to retirement, such as a downpayment on a home or for a new car. If you’re saving for college, you’d use a 529 plan, but for just about anything else you could use a taxable account. For example, I have my emergency money and extra spending money in a money market fund among my taxable accounts. The alternative to this is to use a bank and invest in a high-yield savings account, a certificate of deposit (CD), or a money market account. Bankrate.com will show you the best rates for each of these reasonable alternatives.

If you are using a taxable account, there are a few things to consider. If you are investing in bonds, you may want to invest in municipal bonds in your taxable account due to the tax benefits. If you are a fan of target date funds, you may not want to use them in a taxable account because the bond portion will kick off income that is taxed at your full marginal tax rate. Most feel that bonds are better placed in a tax-advantaged retirement account unless you are using municipal bonds.

Finance Friday Articles

Here are my favorites this week:

10 Things That Matter Most In Personal Finance

End of the Year Financial Checklist for High Earners

Here are the rest of this week’s articles:

7 Things to Learn From the Periodic Table of Investment Returns

Creating a Personal Finance Curriculum: 5 Questions

Big overhaul set for IRAs could be more or less taxing

Explaining the Different Types of Real Estate Crowdfunding Platforms

Eyes Forward – Saving vs Spending

How Did These Physicians Create Passive Income?

Joining a Cult: The Financial Independence Counterculture

Military spouses will get reimbursed up to $1,000 for professional relicensing costs

Real Estate Investing for Doctors

Retirement and 529 Changes from the SECURE Act

Six Months of Part-Time Work. Or How to Save $60,000 on Taxes.

Should You Invest in Real Estate?

Just about everyone who invests does so in major asset classes including stocks, bonds, and cash equivalents. When it comes to real estate, though, you’ll find widely divergent opinions about its importance in an investment portfolio. There are some well-respected people and institutions who say that real estate investing is unnecessary, and there are others who will tell you it should be your primary asset class. I’ve recently debated whether I should start investing more heavily in real estate, so I wanted to lay out the basic arguments for and against real estate investing.

What is Real Estate?

The answer to this question is not simple because real estate investing comes in many forms. There are relatively passive ways of investing in real estate, such as Real Estate Investment Trusts (REITs). According to Investopedia, a REIT is “a type of security that invests in real estate through property or mortgages and often trades on major exchanges like a stock.” In other words, you can simply invest in a REIT like you do any other stock, mutual fund, or exchange-traded fund (ETF). Just send your money to your investment company, and you own a little slice of passive real estate.

There are more active methods of investing in real estate, such as fixing and flipping. You purchase a property, you make improvements to it, and then you sell it to someone, hopefully for a profit. As you can imagine, this would take quite a bit more work than investing in a REIT.

There are probably over 100 other ways you can invest in real estate. If you’re interested, I’d check out an article on Bigger Pockets, one of the largest websites about real estate investing, entitled “The Top 100 Ways to Make Money in Real Estate.”

Arguments Against Investing in Real Estate

Regular readers know that Vanguard is my go-to source for both advice and my own investments. Vanguard considers real estate an alternative investment, and according to them “alternatives usually come with more risks and higher costs.” They believe that a diversified portfolio of stocks and bonds provides enough diversification and that alternative investments are unnecessary. Only “sophisticated investors” should consider alternatives, and they see direct real estate investment as “expensive and time-consuming.” Most people have exposure to real estate in the equity in their house and diversified stock/bond funds that often include REITs, real estate companies, and mortgage-backed securities. For these reasons, Vanguard doesn’t think additional investment in real estate is necessary.

Another argument against real estate investing is that it can quickly become a second job. While you can hire property managers, they are probably not going to provide the level of service that the owner would provide. Most of us are already fully employed and don’t need a second job. In addition, owning investment properties can create additional legal risk.

When you purchase an individual property, it is like buying a single stock. You are taking what is called an uncompensated risk. Larry Swedroe defines an uncompensated risk as, “Risk – that is, the risk of owning single stock or sector of the market – that can be diversified away. Since the risk can be diversified away, investors are not rewarded with a risk premium (higher expected return) for accepting this type of risk.” Essentially, you are putting all your eggs in one basket that is not diversified by location or property type. Investing in real estate via a REIT can avoid this problem because REITs invest in properties that are diversified.

Real estate is an illiquid asset class with high transaction fees. While I can sell my stock or bond mutual funds or ETFs in seconds on-line and pay extremely low expenses to do so, it will take me weeks or months to buy or sell a property. In addition, I’ll likely pay 5-10 percent of the price in transaction costs.

Arguments for Real Estate Investing

Real estate is easily acquired, most often by purchasing your own single family house or condominium. You have to live somewhere, and there are several tax advantages to owning where you live. Interest payments on your mortgage and property taxes are probably tax deductible. If you sell your property, capital gains of up to $250,000 if you’re single or $500,000 for couples are tax-free. In addition, paying a mortgage forces you to save by making regular payments, some of which pay off the principle balance of your loan. That is money you’ll get back when you sell.

When compared to stocks or bonds, which have a global, efficient market, real estate often has a local, inefficient market. This means that if you are willing to look, you can probably find some bargains out there much more easily than you can find a bargain stock. Here’s a review of a good book on real estate investing for physicians.

One of the goals of diversification is to have investments that are not correlated with each other. In other words, when investment A drops in price you have investment B that does not. When compared to stocks and bonds, real estate is not perfectly correlated with other investments and therefore provides diversification. An article about the diversification benefit of REITs makes for an interesting read, if you’re interested, although it is a little old. Vanguard came to the conclusion that over-weighting REITs in a target date fund was not worth it. And this very well regarded guy doesn’t believe in over-weighting REITs either.

You can use leverage or “other people’s money” to increase investment returns. Instead of buying a property for $120,000, you could buy three $160,000 properties with a $40,000 down payment on each. This can increase your returns, but in a down market it can also dramatically increase your losses. As many found out during the housing market crash, leverage is a double-edged sword.

Real estate is an inflation hedge. Burton Malkiel says, “A good house on good land keeps its value no matter what happens to money.” Rents and property values tend to rise as prices rise, preserving your purchasing power. Since your mortgage payment doesn’t change with inflation, while rents are going up your mortgage payment remains the same. Stocks do hedge inflation somewhat, but the companies they represent and the stocks themselves tend to get hurt as the prices of raw materials rise.

The Bottom Line

There are a lot of different ways to invest in real estate, passively investing in REITs, fixing and flipping, owning rental properties, and all sorts of other investment opportunities. Like Vanguard, I don’t think it is necessary to invest in real estate, but it is something to consider if you think you will either enjoy it or believe the value it adds to your investment portfolio is worth the effort.

Finance Friday Articles

Here are my favorite articles this week:

Ask The Experts – Rental Property Q&A with Roofstock

Is Sustainable Investing Good for You?

These Charitable Investment Strategies Deliver a ‘Three-fer’

Here are the rest of this week’s articles:

9 Financial Considerations as You Approach the End of Your Career

Candy Land – Should You Invest in Things Other Than Index Funds

Fellowship Rarely Makes Sense Financially

Going Part-Time: Is It Worth It?

Having the Financial Talk… With Your Parents

Low Blows – Are Investors Benefiting from the Cut in Fund Fees?

Pros and Cons of Target Date Funds

Pulling Your Retirement Levers

Are the Thrift Savings Plan Lifecycle Funds Too Conservative?

We’ve talked a lot about the Thrift Savings Plan and all of its investment options. The easy button is to just use a Lifecycle Fund or L Fund. Pick the approximate year you intend to retire, and use the L Fund with the year in its name that is closest to your retirement year.

For example, if you want to retire in 2038, you’d pick the L 2040 Fund because that is the one closest to 2038. Pretty simple.

Funds like the L Funds are called target date funds. Investopedia defines a target date fund as:

A target-date fund is a fund offered by an investment company that seeks to grow assets over a specified period of time for a targeted goal. Target-date funds are usually named by the year in which the investor plans to begin utilizing the assets. The funds are structured to address a capital need at some date in the future, such as retirement. The asset allocation of a target-date fund is therefore a function of the specified timeframe available to meet the targeted investment objective. A target-date fund’s risk tolerance become more conservative as it approaches its objective target date.

Target date funds have become super popular, but how do the TSP L Funds compare to other target date funds? In particular, how risky or conservative are they when it comes to their asset allocation? Let’s take a look and find out.

More Stocks = More Risk

The TSP L Funds only invest in two broad asset classes, stocks and bonds. The higher percentage of your portfolio you have allocated to stocks, the more risk you are taking.

How does the TSP L Fund stock allocation compare to similar funds at other investment companies? Here are the stock and bond allocation percentages for a few 2040 target date funds (rounded to the nearest whole percentage):

- TSP L 2040 = 72% stocks, 28% bonds

- Fidelity Freedom Fund 2040 (FFFFX) = 93% stocks, 7% bonds

- Schwab Target 2040 Index Fund (SWYGX) = 82% stocks, 18% bonds

- Vanguard Target Retirement 2040 (VFORX) – 83% stocks, 17% bonds

As you can see, the TSP L 2040 is by far the most conservative fund with only 72% stocks. The next closest is the Schwab fund at 82% stocks with Vanguard close behind at 83%. Fidelity wins the aggressiveness award for the 2040 target date.

Just Pick a Different Target Date?

If the conservative nature of the TSP L Funds bothers you, you can always dial up the risk by adjusting the target date you select. Just because you want to retire around the year 2040 doesn’t mean you can’t use the L 2050 fund. By picking it, you’d have a more aggressive asset allocation than the L 2040 but still get the benefits of a target date fund like automatic rebalancing and a gradually more conservative allocation as you age.

But if you look at the L 2050 fund, you’ll find its asset allocation to be 82% stocks and 18% bonds. In other words, the L 2050 is more conservative than two of the three 2040 funds listed above and the same as the one from Schwab. And since it is the most aggressive L Fund available in the TSP, it limits how aggressive you can get while using a Lifecycle Fund.

Why are L Funds so Conservative? Is it Appropriate?

The answer to the first question is because they are based on “based on professionally determined asset allocations.”

The answer to the second question, in my opinion, is probably not. While a conservative investor would have no issues with the L Fund asset allocations, a moderate or aggressive investor would, especially if they are staying in the military long enough to leave with a government guaranteed, inflation adjusted pension.

As we all know around here, that pension is extremely valuable. In addition, when viewed in the context of your entire portfolio, its safety could allow you to take more risk with the rest of your investments.

How Does This Affect You?

If you don’t use a L Fund, it doesn’t.

If you do use them, though, you should use them realizing that:

- Among target date funds, they are conservative.

- Even by picking the L Fund 2050, the most aggressive you can get your asset allocation will be 82% stocks and 18% bonds.

- Despite all of this, they are still the easiest way to invest for retirement in the TSP.

2020 BAH/BAS/Basic Pay Rates and Finance Friday Articles

The DoD released the 2020 pay info:

Here are my favorite articles this week:

9 Practical Tips to Find Contentment

Overweighting REITs: Why Don’t More Experts Recommend It?

Riding Out Private Real Estate Deals

Here are the rest of this week’s articles:

10 Guiding Principles for Physician Debt Management

Durn Furriners – A Discussion of Foreign Stock Allocation

Owning Oddities – Factor Investing

Spend Money On Experiences… And Some Things, Too

Supersavers and the Roth vs Tax-deferred 401(k) Dilemma

WCI vs PoF: A Pro/Con on Donor Advised Funds

What’s the Best Age to Take Social Security?

While On International Travel, Always Transact In Local Currency

Finance Friday Articles

Here are my favorites this week:

Are You Leaving Money On The Table?

Making the Call – Roth vs Traditional

The Ultimate Productivity Hack is Saying No

Here are the rest of this week’s articles:

6 TRICARE Resources You Might Not Know About

All-Time Highs Are Both Scary & Normal

A Primer on Real Estate Professional Status for Physicians

Beyond Fee-Only: 7 Things to Know About the Advice-Only Model

Bull Markets Last Much Longer Than You Think

How to Fast FIRE Your Way to Generational Wealth – Part I

How We Went From Full-Time Physicians to Semi-Retired MDs

How Your TRICARE Costs Will Change in 2020

I Made $15 Million Before I Was 30, And It Wasn’t As Awesome As You’d Think

Make these Five Tax Moves Before December 31st

Six Principles of Asset Location

Smart Career Alternatives and Retirement for Physicians

Strategies To Consider When Building An Effective Retirement Income Plan

Student Loan Advice: 7 Rules of Thumb

The Code, Conflicts, and Client Interest

There’s Always a Bear Market Somewhere

What Causes Physician Burnout? The Medscape Survey

Where Have All The Stock Market Returns Come From This Decade?

Why Opportunity Fund Investors Shouldn’t Settle for High Fees

Why the best person to give you money advice may NOT be an accountant or financial adviser