personal finance

Free Tax Software and Finance Friday Articles

Here’s a blurb about the free military tax software:

MilTax Preparation and e-Filing Software will be available starting Jan. 22 through mid-October. Powered by an industry-leading tax service provider, it’s designed to address situations specific to the military. This easy-to-use, self-paced tax software walks you through a series of questions to help you complete and electronically file your federal return and up to three state tax forms. Calculations are 100 percent accurate – guaranteed by the software provider.

Here is the link to begin preparations:

https://www.militaryonesource.mil/financial-legal/tax-resource-center/miltax-military-tax-services

Here’s an article for military members:

Here are my favorites this week:

Investing Basics for Physicians With Little Time or Experience

Here are the rest of this week’s articles:

2018 vs. 2019 in the Stock Market

7 Paradoxes in Investment Decision Making

Can I Change the Beneficiary of My 529 Plan/Account?

Do Bonds Belong in Your Portfolio?

How to Pay Off Medical School Loans In Less Than 2 Years

Life Goes By Quick: Money Thoughts From A Boomer Retiree With Cancer

Finance Friday Articles

Here are my favorites this week:

Confessions of an Ex-AUM Financial Advisor

The Relationship Between War & The Stock Market

What The White Coat Investor Really Thinks

Here are the rest of the articles this week:

5 Ways Investing Is Like Weight Loss

Achieving Financial Freedom as a Physician is Simple, but Not Easy

A Real Estate Investor’s Guide to the Equity Waterfall

Backdoor Roth IRA 2020: Step by Step Guide with Vanguard

Before Hopping on the BRRRR Bandwagon, Consider This

Determining How Much To Contribute To A 529 Plan: Too Much No Good!

How Do Your Financial Priorities Stack Up With Our Pyramid?

If Only – What a $25 Savings Bond from 1987 is Worth Today

I Own 24 Units But Choose to Rent—Here’s Why

Mr. Money Mustache on Purposeful Work & Life After Financial Independence

Opening the Spigot: Learning to Spend After Decades of Saving

Physician Lifestyle Inflation After The First Big Paycheck

Read the Fine Print (this is particularly relevant to anyone in the BRS…if you fill the TSP too early, you lose out on the monthly 5% match, leaving free money on the table)

Should You Invest in a Roth or Traditional 401(k)?

Top 5 Ways a Virtual Assistant Improves My Life

Updating My Favorite Performance Chart For 2019

Finance Friday Articles

Here are this week’s favorites:

10 Things Investors Can Expect in 2020

How a 28-Year-Old Used the GI Bill to Buy Multiple Rental Properties

Saving Money. How Much is Enough? The 30% Rule

Here are the rest of this week’s articles:

6 Life Laws That Will Make You Rich

7 Ways To Get Your Partner On Board Financially

8 Ways to Automate Your Finances

Are you a service member wanting to sock away $1 million for retirement? Here’s how

Episode #1: How Batching Might Save Your Personal Finances

From Residency to Real Money: Making the Transition as a Couple

How Much Money Do Doctors Make & Why It Doesn’t Matter

The Best Way for Millennials to Start Investing in Real Estate in 2020

The Blended Retirement System Lump Sum – Probably Not a Good Idea

Now that the Blended Retirement System (BRS) is in full effect, it is time to start digging a little deeper on some of its features, like the lump sum payment. Here is a pocket card put out by the DoD Office of Financial Readiness to explain the lump sum feature of the BRS:

Reading through the card, I think it does the best job I’ve seen so far at explaining how the lump sum option works, especially for those who don’t understand what discounting is:

Discounting is the process of determining the present value of a payment or a stream of payments that is to be received in the future. Given the time value of money, a dollar is worth more today than it would be worth tomorrow. Discounting is the primary factor used in pricing a stream of tomorrow’s cash flows.

When discounting future cash flows to determine the present value, you have to use what is very much like a reverse interest rate, called the discount rate:

The discount rate also refers to the interest rate used in discounted cash flow analysis to determine the present value of future cash flows.

The higher the discount rate, the lower the present value of your future cash flows and the smaller your lump sum would be. Some have criticized the DoD for setting the discount rate too high. While adjusted annually, it is 6.75% for 2020.

What I really found interesting about this pocket card I had found, and what caused me to write this blog post, was this part of it:

Note that the DoD Office of Financial Readiness is admitting, “For most Service members, a guaranteed stream of income for life is likely better than a lump sum.”

Yes! One of my biggest beefs against the BRS is that it gives you options like this and the chance to make a mistake. You can’t screw up the guaranteed stream of inflation-adjusted income that comes with the legacy retirement system.

You can screw up a lump sum, reduced by a high discount rate, by blowing it on an expensive car, too large of a house, a weekend in Vegas, or whatever else people like to waste money on. Yes, you could use it productively, perhaps to start a business, buy a franchise, or acquire high-paying skills with further education. But you could just as easily buy one of these:

Do yourself a favor. If you are in the BRS, when the time comes think long and hard before you reduce your future income streams and take a lump sum payment. As the DoD itself admits, “For most Service members, a guaranteed stream of income for life is likely better than a lump sum.”

Make Sure You Snatch the Blended Retirement System Match

Here’s a tip from one of my favorite blogs and authors, Jonathan Clements from Humble Dollar:

SNATCH THE MATCH. Are you on track to contribute enough to your 401(k) to get this year’s full matching employer contribution? If not, crank up your contribution now, so you can spread the required sum over this year’s remaining paychecks. In 2020, the maximum 401(k) contribution is $19,500, or $26,000 if you’re age 50 or older.

For nearly my entire career this wasn’t an issue for those in the military, but it is now due to the new Blended Retirement System (BRS) and its matching Thrift Savings Plan (TSP) contributions. To refresh your memory, if you contribute 5% of your pay to the TSP you get up to a 5% match. If you are in the BRS and you don’t contribute at least 5% every month, you are leaving free money on the table:

Also, you want to make sure you don’t fill up your TSP too early. While many service members will find it hard to get to the 2020 annual limit of $19,500, for those that do they want to space it out over the whole year. If you fill up your TSP in October and can no longer contribute for November or December, you won’t a get a match that month and will lose out on that money.

While I’m not in the BRS, I do a few things with my TSP contributions that I’d recommend everyone do:

- Contribute from your basic pay and not from bonuses or other variable or one-time pays. Your basic pay is the most consistent so use that.

- Spread it out over the whole year. For 2020, I’m contributing about $1625/month so that I come in just at the $19,500 limit in December.

- I see how much of my TSP is left after the November LES is released, and adjust December to get as close to the limit as possible.

Finance Friday Articles

Here is an article about the pay raise we just got:

Biggest military pay raise in years takes effect Jan. 1; check out the complete chart

Here are my favorites this week:

3 Examples of Why Workaholic Real Estate Investors Have It All Wrong

6 Subjects That Should Have Sparked Your Curiosity in 2019

SECURE Act — 8 Things You Need to Know

Here are the rest of the articles:

7 Financial Planning Tips for Locums Docs

11 SMART Financial Goals for Your New Year’s Resolutions

An Unkind Act – The SECURE Act

Donating to a Vanguard Charitable Donor Advised Fund from a Vanguard Brokerage Account

How The SECURE Act Changes Your Retirement Planning

Investing in a Three Fund Portfolio Across Numerous Accounts. Get the Spreadsheet!

Is Buying Stocks at an All-Time High a Good Idea?

It’s So Important to Diversify Your Real Estate Portfolio

Risk Management in Private Real Estate: 3 Types of Uncertainty

SECURE Act And Tax Extenders Creates Retirement Planning Opportunities And Challenges

Thanks for Nothing, Financial Advisor

There are two versions of the S&P 500 index — this is the better investment

The Keys to Financial Success Are Incredibly Mundane (Sorry!)

The SECURE Act: What You Should Know About Retirement Account Reforms

Automate Your Bill Paying

Here’s a tip from one of my favorite blogs and authors, Jonathan Clements from Humble Dollar:

AUTOMATE YOUR BILL PAYING. That way, you’ll avoid late payments—crucial to maintaining a good credit score. The downside: You need to be vigilant about keeping enough in your bank account, so you don’t trigger fees for overdrafts or insufficient funds. This is a particular concern with credit card bills, which can vary so much from one month to the next.

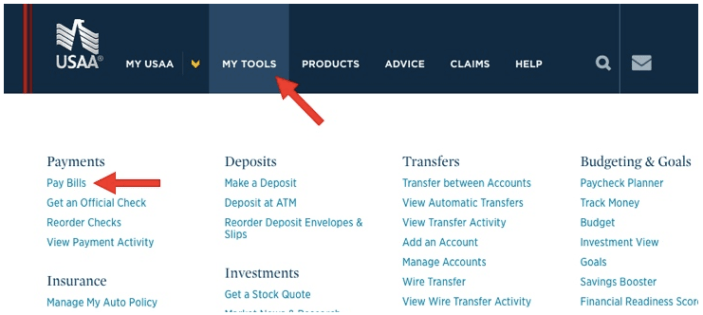

How do you do this with USAA, which is where I do my banking?

To sign up with USAA, go here:

Asset Location

Here’s a tip on asset location from one of my favorite blogs and authors, Jonathan Clements from Humble Dollar:

After deciding what investments to buy, we should consider asset location. What’s that? It involves divvying up investments between taxable and retirement accounts. If investments generate large annual tax bills—think taxable bonds and actively managed funds—we’ll typically want to hold them in a retirement account.

Jonathan’s advice is the traditional advice. Put your taxable bonds, like the Thrift Savings Plan (TSP) F and G funds, into your retirement accounts. This is what I do. My F and G funds are in the TSP, clearly a retirement account, and my international bonds (which they don’t have in the TSP) are in an individual retirement account (IRA).

I don’t own actively managed funds, and I also don’t invest in real estate investment trusts (REITs), although I have in the past and I think about it pretty frequently.

There is another school of thought, though. The White Coat Investor has a different take. You can read about them in his posts entitled My Two Asset Location Pet Peeves and Bonds Go in Taxable!

Of note, just about everyone says to put actively managed funds or REITs in a retirement account, so you won’t find any arguments there.

If you’re really interested in this concept/discussion, the Bogleheads Wiki on tax efficient fund placement is a great read as well.

Will the Government Ever Get Rid of the “Free Lunch” of the TSP G Fund?

They say there’s no free lunch, but in the Thrift Savings Plan there is a free lunch, and it’s called the G Fund. Will the government get rid of this free lunch?

The G Fund Free Lunch

What is this free lunch? You can read about it on this page in the Rewards section:

The G Fund interest rate calculation is based on the weighted average yield of all outstanding Treasury notes and bonds with 4 or more years to maturity. As a result, participants who invest in the G Fund are rewarded with a long-term rate on what is essentially a short-term security. Generally, long-term interest rates are higher than short-term rates.

The government is paying you a higher interest rate than it should. That is the G Fund free lunch.

Why is the Free Lunch at Risk?

The government periodically considers getting rid of it. For example, you can read about it in this article, which is discussing the President’s FY19 budget plan/request. Here’s the relevant portion:

The plan also proposes reducing the statutorily mandated rate of return for the government securities (G) fund to be based on either the three-month or four-week Treasury bill, at a projected savings of $8.9 billion over 10 years.

“G Fund investors benefit from receiving a medium-term Treasury Bond rate of return on what is essentially a short-term security,” the White House wrote. “The budget would instead base the G-fund yield on a short-term T-bill rate.”

TSP spokeswoman Kim Weaver said changing the G Fund’s yield, which is currently 2.75 percent annually, would have a disastrous effect on participants’ ability to save for retirement. If Congress changed the G Fund to track the three-month Treasury bill, the yield would decrease to 1.46 percent, and for the four-week bill it would drop to 1.43 percent.

“Such a change would make the G Fund inadequate and ineffective from an investment standpoint for TSP participants who are saving for retirement,” Weaver said in an email. “More than 3.6 million TSP participants (69 percent) have all or some of their account balance invested in the G Fund. Of those with money in the G Fund, 2 million (39 percent) hold the G Fund as their sole investment choice.”

For a TSP participant who has just retired and is invested entirely in the L Income Fund, which is designed for people who have begun taking annuity payments, they would run out of money at age 84 instead of the current projected age of 92, Weaver said.

Jessica Klement, staff vice president for advocacy at the National Active and Retired Federal Employees Association, said the change would make G Fund investments “useless” and likely force TSP administrators to divest from it entirely.

“[The new rate] would not even keep up with inflation,” she said. “So if you wanted to keep your money in a mostly secure fund, you would not be getting any return, and you’d actually be losing money. And if you took your money out, there would be no other safe, secure investment for those nearing or in retirement.”

What Does This Mean For You?

Right now, it means nothing. This is all just discussion about something that might happen in the future.

What you do need to understand, though, is that the G Fund serves a specific purpose in your portfolio. As the TSP site says:

Consider investing in the G Fund if you would like to have all or a portion of your TSP account completely protected from loss. If you choose to invest in the G Fund, you are placing a higher priority on the stability and preservation of your money than on the opportunity to potentially achieve greater long-term growth in your account through investment in the other TSP funds.

It is alarming that Ms. Weaver from the TSP said, “Of those with money in the G Fund, 2 million (39 percent) hold the G Fund as their sole investment choice.” Those 2 millions people are sacrificing long-term growth for the safest and most conservative investment available in the TSP.

There’s nothing wrong with that if you’re doing it because you are very conservative, near retirement, or the G Fund serves as the bond portion of a larger, more diversified portfolio that has more risky assets like stocks or real estate.

The sad reality is that most who are solely invested in the G Fund are that way because it used to be the default option for those starting a TSP account, and they never switched it to a more aggressive investment option. Under the new Blended Retirement System, the default investment switched from the G Fund to an age-appropriate Lifecycle fund.

What’s the Bottom Line?

The G Fund gives you a free lunch, paying you a higher long-term interest rate while you are investing in short-term securities. The government periodically talks about getting rid of that free lunch.

If you are invested in the G Fund, make sure you are doing it purposely and are aware of its conservative nature. Its emphasis is on preserving wealth rather than growing wealth.

Check Your Beneficiary Designations

Here’s a tip from one of my favorite blogs and authors, Jonathan Clements from Humble Dollar:

CHECK YOUR BENEFICIARY DESIGNATIONS. Your retirement accounts and life insurance will typically pass to the beneficiaries specified on those accounts, not the people named in your will. If your family situation has changed, or you simply don’t remember who you listed, take a moment to review your beneficiary designations.

Don’t let the ex-spouse get your money when you die! Update your beneficiaries.

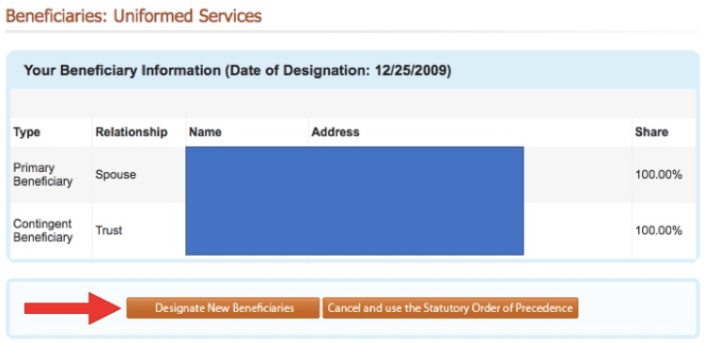

How to See Your Beneficiaries for the Thrift Savings Plan (TSP)

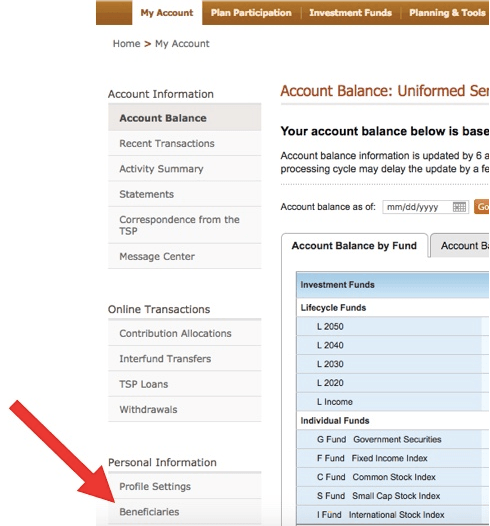

If you log on to the TSP page, you need to click on the link along the lower left, marked by the large red arrow:

Then you’ll see this, and you can change them at the bottom:

Then you’ll see this, and you can change them at the bottom: