personal finance

Thowback Thursday Classic Post – TSP Fund Deep Dive – The F Fund

There are only five investments available in the Thrift Savings Plan (TSP), so let’s take a detailed look at them one at a time. In this post we’ll cover the F Fund.

Inception Date

29 JAN 1988

Fund Management

The Federal Retirement Thrift Investment Board currently contracts BlackRock Institutional Trust Company, N.A. (BlackRock) to manage the F Fund assets. The F Fund remains invested regardless of the performance of the securities markets or the overall economy.

Investment Strategy

The F Fund is invested in a bond index fund that invests in government, corporate, and mortgage-backed bonds. The F Fund’s objective is to match the performance of the Bloomberg Barclays U.S. Aggregate Bond Index.

The F Fund is a passively managed fund that remains invested according to its indexed investment strategy regardless of securities market movements or general economic conditions.

What is the Risk?

Your investment in the F Fund is subject to market risk, credit risk, prepayment risk, and inflation risk.

Because the F Fund returns move up and down with the returns in the bond market, your F Fund investment is subject to market risk. For example, when interest rates rise, bond prices (and thus, the returns of the index and the F Fund) fall. Conversely, in an environment of falling interest rates, bond prices, as well as the index and F Fund returns, rise.

As an F Fund investor, you are also exposed to credit (default) risk, or the possibility that principal and interest payments on the bonds that comprise the index will not be paid.

The F Fund is subject to inflation risk, meaning your F Fund investment may not grow enough to offset the reduction in purchasing power that results from inflation.

Your F Fund investment is also exposed to prepayment risk, which is the probability that if interest rates fall, bonds that are represented in the index will be paid back early thus forcing lenders to reinvest at lower rates.

What is the Benefit?

Although there are several types of risks associated with the F Fund, the overall risk is relatively low in comparison to certain other fixed income investments in the market because the F Fund includes only investment-grade securities. As a result, F Fund investors are rewarded with the opportunity to earn higher rates of return over the long term than they would from investments in short-term securities such as the G Fund. Here is all the performance data as of 14 NOV 2020:

Types of Earnings

The F Fund changes in value as the market price of its bond holdings change. In addition, the F Fund makes money for its investors with capital gains (net of trading costs), interest on notes and bonds, interest on short-term investments, and securities lending income.

BlackRock credits interest income each business day. This income is then reflected in the TSP share prices.

Share Price Calculations

The value of your account is determined each business day based on the daily share price and the number of shares you hold. At the end of each business day, after the stock and bond markets have closed, the total value of the funds’ holdings (net of accrued administrative expenses) is divided by the total number of shares outstanding to determine the share price for that day. The daily change in TSP share prices reflects all investment income (interest on short-term investments, dividends, capital gains or losses, and securities lending income) net of TSP administrative expenses.

Expenses

The net expenses paid by investors is 0.042% or 4.2 basis points, which like all the TSP funds is ridiculously low and is a major benefit of the TSP. It cost $0.42 for each $1,000 invested.

How Should I Use the F Fund in my TSP Account?

In periods of falling interest rates, the F Fund will experience gains from the resulting rise in bond prices. So in the long run, you may expect F Fund returns to exceed those of the G Fund; however, you should also expect greater price volatility (up and down movements).

It is also important to know that higher returns are not guaranteed. This is because losses may occur when interest rates are rising, causing bond prices to fall.

The F Fund can be useful in a portfolio that also contains stocks funds. This is because the prices of bonds and stocks don’t always move in the same direction or by the same amount at the same time. So a retirement portfolio that contains stock funds, like the C, S, and I Funds, along with the F Fund, will tend to be less volatile than one that contains stock funds alone.

Advice from My Favorite Short Investing Book

Here is what my favorite investing book, The Elements of Investing: Easy Lessons for Every Investor, says about investment-grade bond index funds like the F Fund:

If indexing has advantages in the stock market, its superiority is even greater in the bond market. You would never want to hold just one bond (such as an IOU from General Motors or Chrysler) in your portfolio – any single bond issuer could get into financial deficiency and be unable to repay you in full. That’s why you need a broadly diversified portfolio of bonds – making a mutual fund essential. And it’s wise to use bond index funds: They have regularly proved superior to actively managed bond funds.

They also say, “Well-diversified portfolios should have holdings of bonds as well as stocks.”

If you want to know how to integrate the F fund into your own TSP investments, read the Crush the TSP series. In particular, step 3 tells you how to figure out how much of your portfolio to devote toward bonds.

Buy the Big Three

Jonathan Clements was a longtime personal finance columnist for The Wall Street Journal, and he offers great advice at the best price you can get (free) on his blog Humble Dollar. Here is one piece of advice from his site:

“BUY THE BIG THREE. The global market portfolio consists of four major sectors, roughly equal in size: U.S. stocks, U.S. bonds, foreign shares and foreign bonds. Arguably, foreign bonds are optional, offering modest yields but wild currency swings. The other three sectors, however, are crucial to a diversified portfolio. Do you have enough exposure to all three?”

It’s a good thing that Mr. Clements considers foreign bonds optional, because they are not available in the Thrift Savings Plan (TSP). The rest of the asset classes are, though. U.S. stocks can be purchased in the C and S funds. U.S. bonds in the G and F funds. The I fund will get your foreign stocks, albeit not in any emerging markets.

In other words, you can get “the big three” very easily in the TSP. If you missed it, you can read about the TSP and all its funds here in my TSP guide.

Finance Friday Articles

There are continued pushes to keep the TSP I Fund from investing in China and other emerging markets:

Senate Measure Backs Pay Freeze, I Fund Limitation

Here are this week’s articles:

Throwback Thursday Classic Post: TSP Fund Deep Dive – The I Fund – The TSP’s Most Controversial Fund

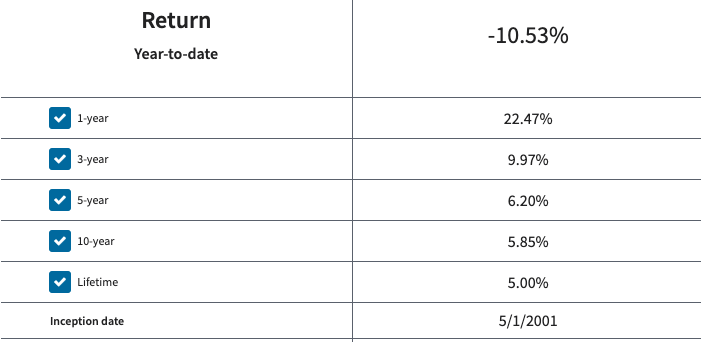

There are only five investments available in the Thrift Savings Plan (TSP), so let’s take a detailed look at them one at a time. In this post we’ll cover the I Fund, which is the most controversial of all the TSP funds.

What’s all the controversy? You can read about it below, but to give you a preview it is because of two things.

First, investment experts disagree on how much of your investments should go into international stocks, which is what the I Fund is composed of.

Second, the I Fund misses out on a key portion of a comprehensive international stock portfolio, emerging markets.

Inception Date

1 MAY 2001

Fund Management

The Federal Retirement Thrift Investment Board currently contracts BlackRock Institutional Trust Company, N.A. (BlackRock) to manage the I Fund assets. The I Fund remains invested regardless of the performance of the securities markets or the overall economy.

Investment Strategy

The I Fund is invested in a stock index fund that invests in international stocks of more than 20 developed countries. The I Fund’s objective is to match the performance of the MSCI EAFE (Europe, Australasia, Far East) Index. Also, some of the money in the I Fund is temporarily invested in the G Fund and earns the G Fund return.

The I Fund is a passively managed fund that remains invested according to its indexed investment strategy regardless of stock market movements or general economic conditions.

What is the Risk?

Your investment in the I Fund is subject to market risk because the prices of the stocks it invests in rise and fall. You are also exposed to inflation risk, meaning your I Fund investment may not grow enough to offset inflation. Unlike the C or S Funds, you are also exposed to currency risk. What’s that? The TSP defines it as:

The risk that the value of a currency will rise or fall relative to the value of other currencies. Currency risk could affect investments in the I Fund because of fluctuations in the value of the U.S. dollar in relation to the currencies of the 22 countries in the EAFE index.

Because of its exposure to currency risk, the I Fund returns will rise or fall as the value of the U.S. dollar decreases or increases relative to the value of the currencies of the countries represented in the EAFE index.

What is the Benefit?

Historically, this increased risk has been rewarded with an increased return. It offers the opportunity to experience gains from equity ownership of international stocks of more than 20 developed countries. Here is all the performance data as of 7 NOV 2020:

Types of Earnings

The I Fund changes in value as the market price of its stocks change. In addition, the I Fund makes money for its investors when those stocks pay dividends. Unlike a traditional mutual fund, though, income from dividends is included in the share price calculation. It is not paid directly to participants’ accounts. Finally, the I fund will change in value due to currency risk, as described above.

It also makes some money on interest on short-term investments and securities lending income.

BlackRock credits interest and dividend income each business day. This income is then reflected in the TSP share prices.

Share Price Calculations

The value of your account is determined each business day based on the daily share price and the number of shares you hold. At the end of each business day, after the stock and bond markets have closed, the total value of the funds’ holdings (net of accrued administrative expenses) is divided by the total number of shares outstanding to determine the share price for that day. The daily change in TSP share prices reflects all investment income (interest on short-term investments, dividends, capital gains or losses, and securities lending income) net of TSP administrative expenses.

Expenses

The net expenses paid by investors is 0.042% or 4.2 basis points, which like all the TSP funds is ridiculously low and is a major benefit of the TSP. It cost $0.42 for each $1,000 invested.

How Should I Use the I Fund in my TSP Account?

The I Fund can be useful in a portfolio that also contains stock funds that track other indices, such as the C Fund (which tracks an index of large U.S. company stocks) and the S Fund (which tracks an index of small-medium U.S. company stocks). The C, S, and I Funds track different segments of the global stock market without overlapping. This is important because the prices of stocks in each market segment don’t always move in the same direction or by the same amount at the same time. By investing in all segments of the stock market (as opposed to just one), you reduce your exposure to market risk.

The controversy among investment experts, though, is how much of your stock portfolio should be invested internationally. You’ll find respected investment experts who recommend anywhere from 0% of your stocks being invested in international markets (like John Bogle, the founder of Vanguard) to about 50%. An extensive discussion on this can be found in Step 4 of our Crush the TSP Series – Invest. What’s the bottom line? Here is what I think…

A 40% international allocation is between the 0% Bogle viewpoint and the 50% global weighting viewpoint, so it seems fine to me and that is what I do. Ultimately, you can pick anywhere from 0% to 50% and find someone really smart who agrees with you. I’d encourage you to have some exposure to international, so I’d say you should pick at least 20%, but it really is up to you.

The I Fund can also be useful in a portfolio that contains bonds. Again, it is because the prices of stocks and bonds don’t always move in the same direction or by the same amount at the same time. So a retirement portfolio that contains a bond fund like the F Fund, along with other stock funds, like the C and S Funds, will tend to be less volatile than one that contains stock funds alone.

Advice from My Favorite Short Investing Book

Here is what my favorite investing book, The Elements of Investing: Easy Lessons for Every Investor, says about international stock funds like the I Fund:

We do believe that investors should combine one of the total U.S. stock market index funds with a total international stock market index fund.

How do you do this with the TSP? Well…you can’t, and that is why the I Fund is controversial.

If you want to invest in the total US stock market, you just combine the C Fund with the S Fund in a 3:1 ratio. To see how I use the S Fund, read the Crush the TSP series.

But you cannot invest in a total international stock market index fund in the TSP because the I Fund is its only international stock option and it does not invest in emerging markets. Emerging markets include some of the largest economies in the world, like China and India. You can read more about emerging markets here.

At one point, the TSP was going to have the I Fund switch its index to include emerging markets. They were going to be switching to the MSCI All Country World Index Ex-U.S. index, which is broader and includes both developed and emerging markets. These efforts were halted, however, due to controversy about investing in China.

Until this change occurs, you won’t be able to use the TSP to invest in a total international stock market index fund because that is what the I Fund will be. That’s why all my international stock exposure is through my investments at Vanguard.

Lessons to Learn from the 2020 Stock Market Decline

In 2020, the US stock market took about a 30% dive in 22 days, followed by a rapid recovery. What lessons can we all learn from the 30% decline?

1. The stock market is volatile.

Since 2009, the stock market has quadrupled in value. This has given many investors the impression that the stock market does nothing but go up. Those of us with more grey hair (or less hair, in my case) have invested during market declines and know that what goes up can also come down.

Here is a telling chart that shows you the volatility of a portfolio constructed of various portions of stocks and bonds (Source: Vanguard.com):

| Stock/Bond Ratio | Maximum 1 Year Decline | Maximum 1 Year Increase |

| 100% Bonds | -8% | +32% |

| 80% Bonds/20% Stocks | -10% | +30% |

| 50% Stocks/50% Bonds | -23% | +32% |

| 80% Stocks/20% Bonds | -35% | +45% |

| 100% Stocks | -43% | +54% |

All investors need to take a hard look at this. Notice that a 100% stock portfolio has dropped as much as 43% in a year. In other words, the 30% drop wasn’t as bad as it could have been.

2. Everyone needs a plan they can stick to during market declines.

One of the biggest mistakes investors can make is to sell low. For this reason, you need a financial plan that you can stick to during market declines.

For example, my current overall target asset allocation is 80% stocks and 20% bonds. This is based on my own risk tolerance and retirement time-frame, and I know I can stick to it.

What did I do during the stock market decline? I purchased more stocks. Why? It had nothing to do with the decline, and everything to do with my plan.

When it was time to invest, I took a look at my desired asset allocation of 80/20. I saw that I had less than 80% in stocks, so I purchased more. It was that simple.

Everyone needs a written personal financial plan so that when the seas get rough, you don’t bail out. You stick to your plan. My plan was 80% stocks and 20% bonds, and I stuck to it.

What is your plan?

3. Regularly re-assess your own personal risk tolerance.

We’ve established that a 30% stock market decline is something that we should expect. In fact, it could be much worse.

It is time for some serious introspection. How did a 30% decline make you feel? Did you sell stocks low? Did you seriously contemplate it?

Me? As I already discussed, I just marched on with my plan, which is what I’d encourage you to do, but everyone is different.

If the decline spooked you, you need to reassess your personal risk tolerance. My favorite way is to take the Vanguard survey. There are other ways, though. It could be a conversation with your financial planner. It could be sitting down with your significant other and carefully examining the chart above and talking about it. It could be by getting a second opinion on your plan.

Whatever it is, you need to do it. For me, it is something I do on an annual basis.

The Bottom Line

Here are the three lessons we all need to learn from the 2020 30% market decline:

- The stock market is volatile.

- Everyone needs a plan they can stick to during market declines.

- Regularly re-assess your own personal risk tolerance.

Cap Alternative Investments

Jonathan Clements was a longtime personal finance columnist for The Wall Street Journal, and he offers great advice at the best price you can get (free) on his blog Humble Dollar. Here is one piece of advice from his site:

“CAP ALTERNATIVE INVESTMENTS. How much do you have in alternative investments—everything from gold to commodities to hedge funds? As a rule, keep your allocation to 10% or less of your total portfolio’s value, and favor simpler, less expensive options, such as funds that focus on gold stocks and on real estate investment trusts.”

As you may or may not know, you cannot invest in any alternative investments in the Thrift Savings Plan (TSP). When it comes to using alternative investments in other portions of your investing portfolio outside of the TSP, there are really two separate questions…

Do You NEED to Invest in Alternatives?

BLUF – No

I get this answer from my favorite investment company outside the TSP…Vanguard. In this article about alternatives, they say:

For most investors, a portfolio of stocks and bonds provides plenty of diversification. Only the most sophisticated investors should consider alternative options.

The answer to this question is no. You do not NEED to invest in alternatives. Globally diversified stocks and bonds are enough, and that is what I do because I prefer a simple life. I do not invest in alternatives.

SHOULD You Invest in Alternatives?

BLUF – The answer to this question is very individual. It really is up to you.

While I don’t invest in alternatives, I’ve certainly thought about it a lot. Although at times I’ve been tempted to do it, I’ve avoided the temptation thus far. Some additional sources to consider when trying to answer this question include:

White Coat Investor Alternative Investments Podcast

Humble Dollar Guide – Alternative Investments

This message string on the Bogleheads Forum

A great book on alternative investments – The Only Guide to Alternative Investments You’ll Ever Need: The Good, the Flawed, the Bad, and the Ugly (Bloomberg) – which happens to be on my bookshelf.

Finance Friday Articles

Here are this week’s articles:

Asset Allocation

Jonathan Clements was a longtime personal finance columnist for The Wall Street Journal, and he offers great advice at the best price you can get (free) on his blog Humble Dollar. Here is one piece of advice from his site:

“ASSET ALLOCATION. This is a portfolio’s split between the four asset classes: stocks, bonds, cash investments like savings accounts and money market funds, and alternative investments like gold, real estate and hedge funds. It’s arguably the most important decision an investor makes. The more a portfolio has in stocks, the greater its volatility—but the higher its expected return.”

Like Jonathan mentions above, this is arguably the most important decision you make. Once you make the decision, it solves many of your investing dilemmas.

For example, many people think that the stock market is an overvalued bubble about to burst. What do you do at the end of this month when you are looking to invest some money? You look at your desired asset allocation and invest in whatever is underweighted. If nothing is underweighted, you invest in them proportionally and consistent with your asset allocation. If your desired allocation is 80% stocks and 20% bonds, you invest 80% in stocks and 20% in bonds.

The bubble bursts tomorrow and it’s the end of the month. What do you do? Again, you look at your desired asset allocation and invest in whatever is underweighted (likely stocks).

Picking an appropriate asset allocation and sticking to it simplifies your financial life and solves mental dilemmas.

If you want some help, here’s my take on how to select an appropriate asset allocation. You can also find a discussion about it in our 6th step to financial security – Invest in Stock and Bond Index Funds or ETFs.

2021 TSP Contribution Limits Unchanged and Finance Friday Articles

Here’s a link to the TSP article:

TSP Investment Limits to Be Unchanged for 2021

Here are this week’s articles:

- 7 Reasons Not to Use a 100% Stock Portfolio

- Are We Trading Our Happiness for Modern Comforts? As society gets richer, people chase the wrong things.

- Doing Good

- Look Under the Hood (note that Tesla is included in the TSP S fund)

- The Importance of Diversification in Achieving Long-Term Goals

- The Taxman Cometh

- Why You Shouldn’t Max Out Your 401(k)

Throwback Thursday Classic Post – Thrift Savings Plan Fund Deep Dive – The S Fund

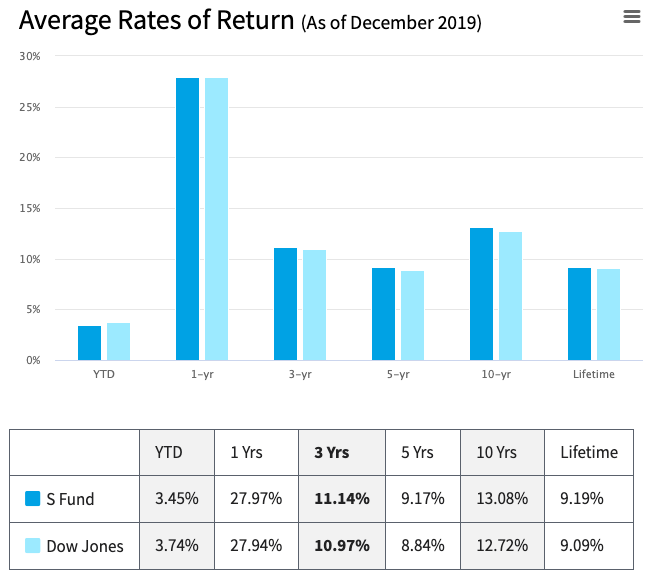

There are only five investments available in the Thrift Savings Plan (TSP), so let’s take a detailed look at them one at a time. In this post we’ll cover the S Fund. You can combine the S Fund with the C Fund to invest in the entire US stock market.

Inception Date

1 MAY 2001

Fund Management

The Federal Retirement Thrift Investment Board currently contracts BlackRock Institutional Trust Company, N.A. (BlackRock) to manage the S Fund assets. The S Fund remains invested regardless of the performance of the securities markets or the overall economy.

Investment Strategy

The S Fund is invested in a stock index fund that invests in small to medium-sized U.S. companies that are not included in the C Fund. The S Fund’s objective is to match the performance of the Dow Jones U.S. Completion TSM Index, which means that when you combine the S Fund and C Fund you are investing in the entire US stock market. Also, some of the money in the S Fund is temporarily invested in the G Fund and earns the G Fund return.

The S Fund is a passively managed fund that remains invested according to its indexed investment strategy regardless of stock market movements or general economic conditions.

What is the Risk?

Your investment in the S Fund is subject to market risk because the prices of the stocks it invests in rise and fall. You are also exposed to inflation risk, meaning your S Fund investment may not grow enough to offset inflation.

What is the Benefit?

Historically, this increased risk has been rewarded with an increased return. It offers the opportunity to experience gains from equity ownership of small and medium-sized US company stocks. Here is all the performance data as of 24 OCT 2020:

Types of Earnings

The S Fund changes in value as the market price of its stocks change. In addition, the S Fund makes money for its investors when those stocks pay dividends. Unlike a traditional mutual fund, though, income from dividends is included in the share price calculation. It is not paid directly to participants’ accounts.

It also makes some money on interest on short-term investments and securities lending income.

BlackRock credits interest and dividend income each business day. This income is then reflected in the TSP share prices.

Share Price Calculations

The value of your account is determined each business day based on the daily share price and the number of shares you hold. At the end of each business day, after the stock and bond markets have closed, the total value of the funds’ holdings (net of accrued administrative expenses) is divided by the total number of shares outstanding to determine the share price for that day. The daily change in TSP share prices reflects all investment income (interest on short-term investments, dividends, capital gains or losses, and securities lending income) net of TSP administrative expenses.

Expenses

The net expenses paid by investors is 0.042% or 4.2 basis points, which like all the TSP funds is ridiculously low and is a major benefit of the TSP. It cost $0.42 for each $1,000 invested.

How Should I Use the S Fund in my TSP Account?

The S Fund can be useful in a portfolio that also contains stock funds that track other indexes such as the C Fund (which tracks an index of large U.S. company stocks) and the I Fund (which tracks an index of international stocks). The C, S, and I Funds track different segments of the overall stock market without overlapping. This is important because the prices of stocks in each market segment don’t always move in the same direction or by the same amount at the same time. By investing in all segments of the stock market (as opposed to just one), you reduce your exposure to market risk.

The S Fund can also be useful in a portfolio that contains bonds. Again, it is because the prices of stocks and bonds don’t always move in the same direction or by the same amount at the same time. So a retirement portfolio that contains a bond fund like the F Fund, along with other stock funds, like the C and I Funds, will tend to be less volatile than one that contains stock funds alone.

Advice from My Favorite Short Investing Book

Here is what my favorite investing book, The Elements of Investing: Easy Lessons for Every Investor, says about small and mid-cap funds like the S Fund:

The S&P 500 [C Fund in the TSP] represents only about 70 percent of the total value of all stocks traded in the United States. It excludes the 30 percent made up of smaller companies [which are in the S Fund], many of which are the most entrepreneurial and capable of the fastest future growth.

If you want to invest in the entire US stock market, you just combine the C Fund with the S Fund in a 3:1 ratio. To see how I use the S Fund, read the Crush the TSP series.