personal finance

Thrift Savings Plan Fund Deep Dive – The S Fund

There are only five investments available in the Thrift Savings Plan (TSP), so let’s take a detailed look at them one at a time. In this post we’ll cover the S Fund. You can combine the S Fund with the C Fund to invest in the entire US stock market.

Inception Date

1 MAY 2001

Fund Management

The Federal Retirement Thrift Investment Board currently contracts BlackRock Institutional Trust Company, N.A. (BlackRock) to manage the S Fund assets. The S Fund remains invested regardless of the performance of the securities markets or the overall economy.

Investment Strategy

The S Fund is invested in a stock index fund that invests in small to medium-sized U.S. companies that are not included in the C Fund. The S Fund’s objective is to match the performance of the Dow Jones U.S. Completion TSM Index, which means that when you combine the S Fund and C Fund you are investing in the entire US stock market. Also, some of the money in the S Fund is temporarily invested in the G Fund and earns the G Fund return.

The S Fund is a passively managed fund that remains invested according to its indexed investment strategy regardless of stock market movements or general economic conditions.

What is the Risk?

Your investment in the S Fund is subject to market risk because the prices of the stocks it invests in rise and fall. You are also exposed to inflation risk, meaning your S Fund investment may not grow enough to offset inflation.

What is the Benefit?

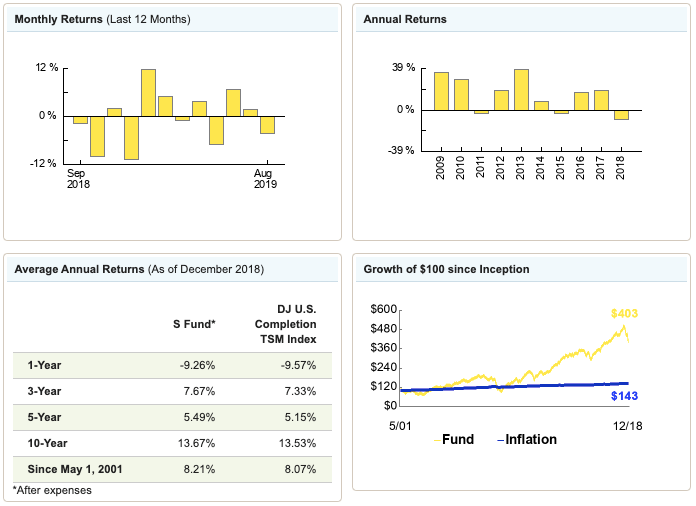

Historically, this increased risk has been rewarded with an increased return. It offers the opportunity to experience gains from equity ownership of small and medium-sized US company stocks. Here is all the performance data as of 26 SEP 2019:

Types of Earnings

The S Fund changes in value as the market price of its stocks change. In addition, the S Fund makes money for its investors when those stocks pay dividends. Unlike a traditional mutual fund, though, income from dividends is included in the share price calculation. It is not paid directly to participants’ accounts.

It also makes some money on interest on short-term investments and securities lending income.

BlackRock credits interest and dividend income each business day. This income is then reflected in the TSP share prices.

Share Price Calculations

The value of your account is determined each business day based on the daily share price and the number of shares you hold. At the end of each business day, after the stock and bond markets have closed, the total value of the funds’ holdings (net of accrued administrative expenses) is divided by the total number of shares outstanding to determine the share price for that day. The daily change in TSP share prices reflects all investment income (interest on short-term investments, dividends, capital gains or losses, and securities lending income) net of TSP administrative expenses.

Expenses

The net expenses paid by investors is 0.040% or 4 basis points, which like all the TSP funds is ridiculously low and is a major benefit of the TSP. It cost $0.40 for each $1,000 invested.

How Should I Use the S Fund in my TSP Account?

The S Fund can be useful in a portfolio that also contains stock funds that track other indexes such as the C Fund (which tracks an index of large U.S. company stocks) and the I Fund (which tracks an index of international stocks). The C, S, and I Funds track different segments of the overall stock market without overlapping. This is important because the prices of stocks in each market segment don’t always move in the same direction or by the same amount at the same time. By investing in all segments of the stock market (as opposed to just one), you reduce your exposure to market risk.

The S Fund can also be useful in a portfolio that contains bonds. Again, it is because the prices of stocks and bonds don’t always move in the same direction or by the same amount at the same time. So a retirement portfolio that contains a bond fund like the F Fund, along with other stock funds, like the C and I Funds, will tend to be less volatile than one that contains stock funds alone.

Advice from My Favorite Short Investing Book

Here is what my favorite investing book, The Elements of Investing: Easy Lessons for Every Investor, says about small and mid-cap funds like the S Fund:

The S&P 500 [C Fund in the TSP] represents only about 70 percent of the total value of all stocks traded in the United States. It excludes the 30 percent made up of smaller companies [which are in the S Fund], many of which are the most entrepreneurial and capable of the fastest future growth.

If you want to invest in the entire US stock market, you just combine the C Fund with the S Fund in a 3:1 ratio. To see how I use the S Fund, read the Crush the TSP series.

Thrift Savings Plan Fund Deep Dive – The C Fund

There are only five investments available in the Thrift Savings Plan (TSP), so let’s take a detailed look at them one at a time. First, we’ll cover the C Fund, which would probably be the fund you would pick if you were only allowed to pick one.

Inception Date

29 JAN 1988

Fund Management

The Federal Retirement Thrift Investment Board currently contracts BlackRock Institutional Trust Company, N.A. (BlackRock) to manage the C Fund assets. The C Fund remains invested regardless of the performance of the securities markets or the overall economy.

Investment Strategy

The C Fund is invested in a stock index fund that fully replicates the Standard and Poor’s 500 (S&P 500) Index, a broad market index made up of the stocks of 500 large to medium-sized U.S. companies. The C Fund’s objective is to match the performance of the S&P 500. Also, some of the money in the C Fund is temporarily invested in the G Fund and earns the G Fund return.

The C Fund is a passively managed fund that remains invested according to its indexed investment strategy regardless of stock market movements or general economic conditions.

What is the Risk?

Your investment in the C Fund is subject to market risk because the prices of the stocks in the S&P 500 Index rise and fall. You are also exposed to inflation risk, meaning your C Fund investment may not grow enough to offset inflation.

What is the Benefit?

Historically, this increased risk has been rewarded with an increased return. It offers the opportunity to experience gains from equity ownership of large and mid-sized U.S. company stocks. Here is all the performance data as of 25 SEP 2019:

Types of Earnings

The C Fund changes in value as the market price of its stocks change. In addition, the C Fund makes money for its investors when those stocks pay dividends. Unlike a traditional mutual fund, though, income from dividends is included in the share price calculation. It is not paid directly to participants’ accounts.

It also makes some money on interest on short-term investments and securities lending income.

BlackRock credits interest and dividend income each business day. This income is then reflected in the TSP share prices.

Share Price Calculations

The value of your account is determined each business day based on the daily share price and the number of shares you hold. At the end of each business day, after the stock and bond markets have closed, the total value of the funds’ holdings (net of accrued administrative expenses) is divided by the total number of shares outstanding to determine the share price for that day. The daily change in TSP share prices reflects all investment income (interest on short-term investments, dividends, capital gains or losses, and securities lending income) net of TSP administrative expenses.

Expenses

The net expenses paid by investors is 0.041% or 4.1 basis points, which like all the TSP funds is ridiculously low and is a major benefit of the TSP. It cost $0.41 for each $1,000 invested.

How Should I Use the C Fund in my TSP Account?

The C Fund can be useful in a portfolio that also contains stock funds that track other indexes such as the S Fund (which tracks an index of small US company stocks) and the I Fund (which tracks an index of international stocks). The C, S, and I Funds track different segments of the overall stock market without overlapping. This is important because the prices of stocks in each market segment don’t always move in the same direction or by the same amount at the same time. By investing in all segments of the stock market (as opposed to just one), you reduce your exposure to market risk.

The C Fund can also be useful in a portfolio that contains bonds. Again, it is because the prices of stocks and bonds don’t always move in the same direction or by the same amount at the same time. So a retirement portfolio that contains a bond fund like the F Fund, along with other stock funds, like the S and I Funds, will tend to be less volatile than one that contains stock funds alone.

Advice from My Favorite Short Investing Book

Here is what my favorite investing book, The Elements of Investing: Easy Lessons for Every Investor, says about S&P 500 index funds like the C Fund:

The best-known of the broad stock market mutual funds and Exchange Traded Funds (ETFs) in the US track the S&P 500 index of the largest stocks. We prefer using a broader index that includes more smaller-company stocks…Funds that track these broader indexes are often referred to as ‘total stock market’ index funds. More than 80 years of stock market history confirm that portfolios of smaller stocks have produced a higher rate of return than the return of the S&P 500 large-company index. While smaller companies are undoubtedly less stable and riskier that large firms, they are likely – on average – to produce somewhat higher future returns. Total stock market index funds are the better way for investors to benefit from the long-run growth of economic activity.

If you want to follow their advice, you just combine the C Fund with the S Fund in a 3:1 ratio. To see how I use the C Fund, read the Crush the TSP series.

Finance Friday Articles

Here are this week’s articles:

5 Major Things To Look For In a Real Estate Fund

A Timely Reminder – Past Performance is No Guarantee of Future Results

End Game – The Downsides of Estimated Life Expectancy for Retirement Planning

Highly Functioning Teams as the Way to Wellness & Professional Fulfillment

How One Man Built A 6-Figure Online Business In Less Than 2 Years

I’ve Turned Into An Investment Collector, and I Love It

Practical Investing Advice for Doctors: The Pareto Principle

Since Market Timing is a Waste of Time, Why are you Still Trying?

Straight Talk – The Basics of Personal Finance

The Financial Advantages of Emergency Physicians

The New Attending Financial Planning Checklist

Vanguard to Offer a New Robo-Advisor with Vanguard Digital Advisory Service

Step 6 to Crush the TSP – Rebalance Annually

We’ve talked about steps 1-5 to crush the Thrift Savings Plan (TSP). Now we move on to the final step (unless I think of more), step 6 – rebalance annually.

What is Rebalancing?

Let’s say that your desired TSP asset allocation is 70% stocks and 30% bonds. After the last year, though, stocks earned more than bonds and now you’re sitting at 85% stocks and 15% bonds. In order to rebalance back to your desired asset allocation, you’d sell approximately 15% of your stocks and buy bonds, restoring your desired asset allocation. It’s that simple.

Why Should You Rebalance?

If you don’t, you may be assuming more or less risk than you desire.

Also, by rebalancing you force yourself to sell what has overperformed and buy what has underperformed. Although this seems counter-intuitive because you are selling what has given you the largest return, by doing this you are systematically selling high and buying low. When left to themselves, investors typically buy high and sell low, the opposite of what you want to do. Rebalancing forces you to do it right.

How Often Should You Rebalance?

Vanguard has researched this, and you can read their full report here:

Best Practices for Portfolio Rebalancing

Their conclusion is:

We conclude that for most broadly diversified stock and bond fund portfolios (assuming reasonable expectations regarding return patterns, average returns, and risk), annual or semiannual monitoring, with rebalancing at 5% thresholds, is likely to produce a reasonable balance between risk control and cost minimization for most investors.

In other words, you rebalance annually or semiannually (twice per year) whenever your current asset allocations are off by 5% or more from your desired allocations. If the current and desired allocations are within 5% of each other, you do nothing.

How Do You Rebalance in the TSP?

You just log on and do what they call an “interfund transfer” or IFT. You can read all about it on this page from the TSP website.

Because you are doing it in a tax-advantaged retirement account, there are no expenses, fees, or taxes associated with rebalancing (unlike if you were rebalancing a taxable account).

You can only do it twice per month without restrictions, but since you are smart you are only doing it once per year anyway.

Do You Need to Rebalance With Lifecycle Funds?

No, you don’t. This is one of the major advantages of the L funds. If you are hitting the easy button on your TSP and just using a Lifecycle fund, you don’t need to rebalance…EVER!

That’s It. Crush the TSP!

That’s the final step to crush it in your TSP account. Read the whole series, maximize your TSP contributions, and get rich in the military.

Step 5 to Crush the TSP – Roth vs Traditional

We’ve talked about steps 1-4 to crush the Thrift Savings Plan (TSP). Now we’re on to step 5, deciding between the Roth vs traditional TSP. Let’s take a look at the difference between the two and help you to decide which is the right choice for you.

The Traditional TSP

The traditional TSP is the first of two potential tax treatments for your TSP contributions. If you elect it, you defer paying taxes on your contributions and their earnings until you withdraw them. This is the only option for any money you get as a result of the 5% government match in the new Blended Retirement System (BRS).

If you are in a combat zone making tax-free contributions, your contributions will be tax-free at withdrawal but your earnings will be subject to tax.

The Roth TSP

The Roth TSP is the second of two potential tax treatments for your TSP contributions. If you contribute to it, you pay taxes on your contributions now and your earnings are tax-free at withdrawal.

The Roth TSP is similar to a Roth 401(k) that a civilian would have, not a Roth IRA. There are no income limits for Roth TSP contributions. You can contribute to both your Roth TSP and a Roth IRA without contributions to one affecting how much you can contribute to the other. For example, in 2019 you can contribute the full $19,000 to your Roth TSP and $6,000 to your Roth IRA.

Which One is Best for You?

Here’s a table that compares the two options from the TSP website:

| The Treatment of… | Traditional TSP | Roth TSP |

|---|---|---|

| Contributions | Pre-tax | After-tax1 |

| Your Paycheck | Taxes are deferred*, so less money is taken out of your paycheck. | Taxes are paid up front*, so more money comes out of your paycheck. |

| Transfers In | Transfers allowed from eligible employer plans and traditional IRAs | Transfers allowed from Roth 401(k)s, Roth 403(b)s, and Roth 457(b)s |

| Transfers Out | Transfers allowed to eligible employer plans, traditional IRAs, and Roth IRAs2 | Transfers allowed to Roth 401(k)s, Roth 403(b)s, Roth 457(b)s, and Roth IRAs3 |

| Withdrawals | Taxable when withdrawn | Tax-free earnings if five years have passed since January 1 of the year you made your first Roth contribution, AND you are age 59½ or older, permanently disabled, or deceased |

* If you are a member of the uniformed services receiving tax-exempt pay (i.e., pay that is subject to the combat zone tax exclusion), your contributions from that pay will also be tax-exempt.

1. Roth contributions are subject to Federal (and, where applicable, state and local) income taxes, while traditional contributions are not taxed until withdrawn. However, both Roth contributions and traditional contributions are included in the amount of wages used to calculate payroll taxes (e.g., Social Security taxes).

2. You would have to pay taxes on any pre-tax amount transferred to a Roth IRA.

3. Transfers to a Roth IRA from a Roth TSP are not subject to the income restrictions that apply to Roth IRA contributions.

The issue of whether Roth is a good option for you was discussed in this TSP Highlights called Is Roth For You?

If you are more of a visual learner, you might enjoy this video from the TSP called “Is Roth Right for Me?”

If you like interactive calculators, this one from Betterment is pretty good.

If you don’t trust anything I say and want to read what someone else thinks, I don’t blame you. Here’s a good article from Money.

The decision really boils down to whether you’d like to pay taxes now (Roth) or later (traditional) and how your current tax rate compares to your likely future tax rate during retirement. While predicting the future is not easy, if you are young or early in your career, your earnings and tax rate are likely to rise in the future, so you should probably lean toward the Roth option. If you are in your peak earning years and you expect your tax rate to fall in retirement, you should probably lean toward the traditional and defer taxes to a future date.

If you are not sure which option to choose, many people recommend you diversify your retirement accounts and simply split the Roth and traditional 50/50. That way in the future you’ll have options depending on how future tax rates and your financial situation changes.

What do I do? I can afford the taxes now and want as much tax-free money available to me as I can get, so I put all the money in the Roth TSP that I can. That said, the first part of my career I didn’t have a Roth option, so a large percentage of my TSP balance is in the traditional TSP as well, so I’m about 50/50 split between the two options.

Some Rules to Be Aware Of

The TSP keeps your traditional and Roth money in separate “buckets” in your TSP account.

You cannot convert any portion of your existing traditional TSP balance to a Roth balance.

You can make both traditional and Roth contributions if you want. You can contribute in any percentages or amounts you choose and can change your election at any time.

If you are getting government contributions (perhaps because you are in the Blended Retirement System), they are deposited into your traditional TSP. You can put your portion in the Roth, but the government’s portion must go in the traditional.

The Bottom Line

Use the resources above to decide if you want to invest in the traditional TSP, the Roth TSP, or some combination of the two. If you’re not sure what to do, I’d just split it 50/50 so you have options in the future.

Keep your eye out for the last step to crush the TSP, rebalancing.

Finance Friday Articles

Here are this week’s articles:

4 Unique Side Income Opportunities Using Your Medical Degree

5 Things You Can Do Today to Become Financially Independent

5 ways to get an advanced education while minimizing debt

10 Ways to Pay Off a Mortgage Quickly

All troops will now get free credit monitoring service

Are Side Hustles the Best Kind of Asset Protection?

Educational Debt and Physician Employment

Explaining the Stock Market to Big Cat

Investing: Where to Put Your Money Now

Maximize Your Dead Time For a New Approach To Life

Questions and Answers about Changes to TSP Withdrawal Options

You Need to Know About Present Value

Right Turn – Shopping for Auto Insurance

Saving For College: Understanding 529s and Other Options

Should You Invest In Variable Annuities and Non-Deductible IRAs?

SIX PERCENT IS THE NEW FOUR PERCENT

Tax-smart charitable giving strategies

Step 4 to Crush the TSP – Invest

You’ve read steps 1, 2, and 3 to crush the Thrift Savings Plan (TSP), and now you’re ready for step 4 and to start investing. In step 3 you came up with your desired asset allocation, so make sure you have that. You’re going to need it for the rest of the post. Just to make life a little easier, we’re going to use an example asset allocation of 80% stocks and 20% bonds.

Bond…James Bond

For the bond portion of your asset allocation, you only have two investment choices:

- G Fund – US government bonds (specially issued to the TSP)

- F Fund – US government, corporate, and mortgage-backed bonds

Both of these are US bond options, which is just fine. There are no international bonds available in the TSP.

We could have an intellectual discussion about the subtle differences between these two bond funds, but we’re not going to. It isn’t necessary. They’re both fine bond funds, so just split the difference, diversify, and put half of your bond allocation in the G fund and half in the F fund.

To illustrate, in the example allocation of 80% stocks and 20% bonds, we’d put 10% in the G fund and 10% in the F fund.

That’s it. The bonds are done.

The Stock Allocation

This is a little more complicated. The largest decision you have to make is how you’re going to divide your stocks between the three options. Here are your choices:

- C Fund – stocks of large and medium-sized US companies

- S Fund – stocks of small to medium-sized US companies (not included in the C Fund)

- I Fund – international stocks of more than 20 developed countries

The first question is what percentage of your stock allocation should go to the I fund. There are a few schools of thought on this.

John Bogle, the founder of Vanguard, is famous for believing that you don’t need to invest any of your stocks in international stocks. His long held belief was that the US companies are doing business globally, so they are already worldwide diversified. For example, Coca-Cola is clearly selling Coke products all over the globe. He would say you should put 0% of your stocks in the I fund.

At the other end of the spectrum are people who believe that you should invest proportionally. If you look at the worldwide value of stocks, it is about a 50/50 split between the US and the rest of the world. These people would say you should put 50% of your allocation in international stocks.

Both of these opinions are reasonable, so anything between 0% and 50% allocated to the I fund is fine. What do I do?

I rely on the research done by Vanguard, an institution managing over $5 trillion. I figure they have more money and resources to research this stuff than I do. What does Vanguard do?

If you look at their Target Retirement Funds, which are meant to be a “one stop shop” kind of investment fund, you’ll notice that they split their stock allocation so that 60% is US and 40% is international. They used to do it 70% US and 30% international, but their research showed 60/40 to be a better split so they moved to it a few years ago.

You’ll notice that a 40% international allocation is between the 0% Bogle viewpoint and the 50% global weighting viewpoint, so it seems fine to me and that is what I do.

If you want another opinion, you can look at the TSP Lifecycle funds. You’ll notice that they do about a 70% US and 30% international split, like Vanguard used to do. Again, that seems reasonable.

Ultimately, you can pick anywhere from 0% to 50% and find someone really smart who agrees with you. I’d encourage you to have some exposure to international, so I’d say you should pick at least 20%, but it really is up to you.

Not sure what to do? Go with 30% (the TSP Lifecycle approach) or 40% (the Vanguard approach) for the I fund and call it a day.

How to Split the C and S Funds

This is easier, or at least I think it is. The C fund is basically an S&P 500 index fund of large companies, with the S fund having the rest of the small and medium sized companies. If you want to mirror the US stock market, you want to put about 75% of your US stock allocation in the C fund and the other 25% in the S fund. You’ll notice that this is what the TSP Lifecycle funds do, further backing up my assertion.

So, I recommend that you split your C and S fund allocation 75/25, respectively.

Putting the Stock Portion All Together

For the stocks, here’s the math:

- (Your desired international stock %) X (your total stock allocation %) = % that goes in the I fund

- (Your total stock allocation %) – (% you are putting in the I fund) = % you must divide into the C and S funds

- (Your % you must divide into the C and S funds) X 0.75 = % that goes in the C fund

- (Your % you must divide into the C and S funds) X 0.25 = % that goes in the S fund

Let’s use the 80% stock and 20% bond example we started with to illustrate. Let’s assume we’re going with a 40% desired allocation to international (like I personally use):

- (Desired international stock = 40%) X (total stock allocation = 80%) = 32% goes in the I fund

- (Total stock allocation = 80%) – (32% that is going in the I fund) = 48% we must divide into the C and S funds

- (48% we must divide into the C and S funds) X 0.75 = 36% that goes in the C fund

- (48% we must divide into the C and S funds) X 0.25 = 12% that goes in the S fund

That gives us a stock allocation of 32% I fund, 36% C fund, and 12% S fund.

The Bottom Line

We split our bond allocation 50/50 between the G and F funds. We put the desired percentage for international stocks in the I fund. We split the remaining stock allocation 75/25 between the C and S funds, respectively.

For the 80% stock and 20% bond portfolio we are using as an example, this plays out:

- 10% in the G fund

- 10% in the F fund

- 32% in the I fund (based on a hypothetical 60/40 US/international stock split, which can vary as discussed above)

- 36% in the C fund

- 12% in the S fund

This can be tough to grasp in a blog post, so if there are questions or points that need clarification just put them in the comments section and we’ll straighten them out.

The next step you need to crush the TSP is to decide if you’re going to go Roth or traditional.

Finance Friday Articles

Here are this week’s articles:

Attending Your Own Funeral: Thoughts on Finances and Legacies

A User’s Manual for Human Financial Behavior

Best Time to Buy a Car and How to Get the Best Deal

Financial Independence With Kids: How Procreation Impacts FIRE

Financial Mistakes for the Financially Literate

Giving Voice – Make Sure You Discuss Major Financial Moves with Your Spouse/Partner

I’m 100% Stocks and Happy with my Diversification

Investing Doesn’t Have To Be Complicated

Is It Ever Too Late To Start Investing In Real Estate?

“I Want To Lower My Taxes” Is a Stupid Goal

Michael Burry Trashes Index Funds – Are We Screwed?

The Best and Worst Case Scenarios for Bonds from Here

The Big Short’s Michael Burry Explains Why Index Funds Are Like Subprime CDOs

‘The Big Short’ Whiffs On Indexing

What The Bible Can Teach You About Money

What to Make of a Stock Market That Has Gone Nowhere for a Year-and-a-Half

Step 3 to Crush the Thrift Savings Plan – Asset Allocation

The Thrift Savings Plan (TSP) is the military’s retirement account. Learning how to maximize its utility should be high on your financial priority list. At MCCareer.org, I’m going to create a guide that will show you how to crush it with the TSP. We already showed you step 1 and step 2 in that guide. Here’s step 3…

The 3rd Step to Crush the TSP – Asset Allocation

You’ve probably heard that you shouldn’t put all of your eggs in one basket. That is what asset allocation is all about…making sure your eggs are in multiple baskets.

Asset allocation can be complex. There are entire books written about nothing but asset allocation, like The Intelligent Asset Allocator: How to Build Your Portfolio to Maximize Returns and Minimize Risk. That’s a good book if you want to nerd out, but I’m going to try and simplify asset allocation for you.

What Assets are Available in the TSP?

There are only five assets available:

- G Fund – US government bonds specially issued to the TSP

- F Fund – US government, corporate, and mortgage-backed bonds

- C Fund – stocks of large and medium-sized US companies

- S Fund – stocks of small to medium-sized US companies (not included in the C Fund)

- I Fund – international stocks of more than 20 developed countries (soon to include emerging markets)

What is not available? There are a few major asset classes unavailable. You cannot invest in real estate or international bonds. International emerging markets will be added to the I Fund soon but are not currently available. If you want exposure to any of these asset classes right now, you’ll have to get them in your other investment accounts, like your IRA or taxable account.

How Do I Pick My Asset Allocation?

If in step 2 you decided to use L Funds, you don’t need to pick an asset allocation for your TSP. The L Fund takes care of it for you.

If you are not going to use L Funds, one way to decide on an asset allocation is to take this Vanguard survey. At the top of the page it will give you a suggested allocation, such as 80% stocks and 20% bonds.

Another way is to borrow from trusted investment experts. Here are a few opinions.

In The Elements of Investing: Easy Lessons for Every Investor

, Burton Malkiel recommends these age-based asset allocations:

- 20-30s – bonds 10-25%, stocks 75-90%

- 40-50s – bonds 25-35%, stocks 65-75%

- 60s – bonds 35-55%, stocks 45-65%

- 70s – bonds 50-65%, stocks 35-50%

- 80s+ – bonds 60-80%, stocks 20-40%

In the same book, Charlie Ellis recommends these asset allocations:

- 20-30s – bonds 0%, stocks 100%

- 40s – bonds 0-10%, stocks 90-100%

- 50s – bonds 15-25%, stocks 75-85%

- 60s – bonds 20-30%, stocks 70-80%

- 70s – bonds 40-60%, stocks 40-60%

- 80s+ – bonds 50-70%, stocks 30-50%

Mr. Ellis is a little more aggressive than Mr. Malkiel because he recommends a higher allocation of stocks.

There are other ways to come up with a reasonable asset allocation, such as financial “rules of thumb.” The founder of Vanguard, John Bogle, is famous for creating the “age in bonds” rule of thumb. It says that whatever your age is, that is the percentage of your investments that should be in bonds. The rest should be in stocks.

For example, I’m 43 years old, so his rule would say I should have 43% in bonds and 57% in stocks.

This rule has been criticized as being too conservative, so some have changed it to 110 or 120 minus your age as the percentage you should have in stocks. For example, for me this would mean:

- 110 minus age 43 = 67% in stocks, the rest (33%) in bonds

- 120 minus age 43 = 77% in stocks, the rest (23%) in bonds

There are certainly other ways to come up with your asset allocation. You could ask a financial advisor. You could read other books. You could read other blog posts, like this one on the Bogleheads Wiki.

What About Other Assets Like Your Pension and Social Security?

This is a tough issue. Some would argue that pensions and social security are income streams and that they should not play into your asset allocation decision. This is what Vanguard argues. Others would argue that they are “bond-like” and should be factored into your asset allocation and counted as a large pile of bonds. Here are a few thoughts on the subject from blogs I follow and trust:

- The Oblivious Investor – How Pensions and Social Security Affect Asset Allocation

- Humble Dollar – A Price on Your Head

The Bottom Line – Asset Allocation

Somehow you have to figure out your desired asset allocation. The info above will hopefully facilitate that. Once you have a target asset allocation, now you have to apply it to the investments available in the TSP. Take the 4th Step…invest.

Finance Friday Articles

Here are this week’s articles…

8 Things To Do With Financial Independence Besides Retire Early

Automated Cash Flow Systems: Put Your Money on Autopilot

Comprehensive List of Physician Finance Bloggers, Past and Present

Debunking the Silly “Passive is a Bubble” Myth

Disability Insurance for Two-Doctor Couples

Risk Adjusted Returns: What’s the Point?

The Road to Burnout Helped Me Find My Purpose

Top 5 Expenses that Go Down in Retirement

Why Does The Stock Market Go Up?