personal finance

Lessons to Learn from the 2020 Stock Market Decline

In 2020, the US stock market took about a 30% dive in 22 days, followed by a rapid recovery. What lessons can we all learn from the 30% decline?

1. The stock market is volatile.

Since 2009, the stock market has quadrupled in value. This has given many investors the impression that the stock market does nothing but go up. Those of us with more grey hair (or less hair, in my case) have invested during market declines and know that what goes up can also come down.

Here is a telling chart that shows you the volatility of a portfolio constructed of various portions of stocks and bonds (Source: Vanguard.com):

| Stock/Bond Ratio | Maximum 1 Year Decline | Maximum 1 Year Increase |

| 100% Bonds | -8% | +32% |

| 80% Bonds/20% Stocks | -10% | +30% |

| 50% Stocks/50% Bonds | -23% | +32% |

| 80% Stocks/20% Bonds | -35% | +45% |

| 100% Stocks | -43% | +54% |

All investors need to take a hard look at this. Notice that a 100% stock portfolio has dropped as much as 43% in a year. In other words, the 30% drop wasn’t as bad as it could have been.

2. Everyone needs a plan they can stick to during market declines.

One of the biggest mistakes investors can make is to sell low. For this reason, you need a financial plan that you can stick to during market declines.

For example, my current overall target asset allocation is 80% stocks and 20% bonds. This is based on my own risk tolerance and retirement time-frame, and I know I can stick to it.

What did I do during the stock market decline? I purchased more stocks. Why? It had nothing to do with the decline, and everything to do with my plan.

When it was time to invest, I took a look at my desired asset allocation of 80/20. I saw that I had less than 80% in stocks, so I purchased more. It was that simple.

Everyone needs a written personal financial plan so that when the seas get rough, you don’t bail out. You stick to your plan. My plan was 80% stocks and 20% bonds, and I stuck to it.

What is your plan?

3. Regularly re-assess your own personal risk tolerance.

We’ve established that a 30% stock market decline is something that we should expect. In fact, it could be much worse.

It is time for some serious introspection. How did a 30% decline make you feel? Did you sell stocks low? Did you seriously contemplate it?

Me? As I already discussed, I just marched on with my plan, which is what I’d encourage you to do, but everyone is different.

If the decline spooked you, you need to reassess your personal risk tolerance. My favorite way is to take the Vanguard survey. There are other ways, though. It could be a conversation with your financial planner. It could be sitting down with your significant other and carefully examining the chart above and talking about it. It could be by getting a second opinion on your plan.

Whatever it is, you need to do it. For me, it is something I do on an annual basis.

The Bottom Line

Here are the three lessons we all need to learn from the 2020 30% market decline:

- The stock market is volatile.

- Everyone needs a plan they can stick to during market declines.

- Regularly re-assess your own personal risk tolerance.

Cap Alternative Investments

Jonathan Clements was a longtime personal finance columnist for The Wall Street Journal, and he offers great advice at the best price you can get (free) on his blog Humble Dollar. Here is one piece of advice from his site:

“CAP ALTERNATIVE INVESTMENTS. How much do you have in alternative investments—everything from gold to commodities to hedge funds? As a rule, keep your allocation to 10% or less of your total portfolio’s value, and favor simpler, less expensive options, such as funds that focus on gold stocks and on real estate investment trusts.”

As you may or may not know, you cannot invest in any alternative investments in the Thrift Savings Plan (TSP). When it comes to using alternative investments in other portions of your investing portfolio outside of the TSP, there are really two separate questions…

Do You NEED to Invest in Alternatives?

BLUF – No

I get this answer from my favorite investment company outside the TSP…Vanguard. In this article about alternatives, they say:

For most investors, a portfolio of stocks and bonds provides plenty of diversification. Only the most sophisticated investors should consider alternative options.

The answer to this question is no. You do not NEED to invest in alternatives. Globally diversified stocks and bonds are enough, and that is what I do because I prefer a simple life. I do not invest in alternatives.

SHOULD You Invest in Alternatives?

BLUF – The answer to this question is very individual. It really is up to you.

While I don’t invest in alternatives, I’ve certainly thought about it a lot. Although at times I’ve been tempted to do it, I’ve avoided the temptation thus far. Some additional sources to consider when trying to answer this question include:

White Coat Investor Alternative Investments Podcast

Humble Dollar Guide – Alternative Investments

This message string on the Bogleheads Forum

A great book on alternative investments – The Only Guide to Alternative Investments You’ll Ever Need: The Good, the Flawed, the Bad, and the Ugly (Bloomberg) – which happens to be on my bookshelf.

Finance Friday Articles

Here are this week’s articles:

Asset Allocation

Jonathan Clements was a longtime personal finance columnist for The Wall Street Journal, and he offers great advice at the best price you can get (free) on his blog Humble Dollar. Here is one piece of advice from his site:

“ASSET ALLOCATION. This is a portfolio’s split between the four asset classes: stocks, bonds, cash investments like savings accounts and money market funds, and alternative investments like gold, real estate and hedge funds. It’s arguably the most important decision an investor makes. The more a portfolio has in stocks, the greater its volatility—but the higher its expected return.”

Like Jonathan mentions above, this is arguably the most important decision you make. Once you make the decision, it solves many of your investing dilemmas.

For example, many people think that the stock market is an overvalued bubble about to burst. What do you do at the end of this month when you are looking to invest some money? You look at your desired asset allocation and invest in whatever is underweighted. If nothing is underweighted, you invest in them proportionally and consistent with your asset allocation. If your desired allocation is 80% stocks and 20% bonds, you invest 80% in stocks and 20% in bonds.

The bubble bursts tomorrow and it’s the end of the month. What do you do? Again, you look at your desired asset allocation and invest in whatever is underweighted (likely stocks).

Picking an appropriate asset allocation and sticking to it simplifies your financial life and solves mental dilemmas.

If you want some help, here’s my take on how to select an appropriate asset allocation. You can also find a discussion about it in our 6th step to financial security – Invest in Stock and Bond Index Funds or ETFs.

2021 TSP Contribution Limits Unchanged and Finance Friday Articles

Here’s a link to the TSP article:

TSP Investment Limits to Be Unchanged for 2021

Here are this week’s articles:

- 7 Reasons Not to Use a 100% Stock Portfolio

- Are We Trading Our Happiness for Modern Comforts? As society gets richer, people chase the wrong things.

- Doing Good

- Look Under the Hood (note that Tesla is included in the TSP S fund)

- The Importance of Diversification in Achieving Long-Term Goals

- The Taxman Cometh

- Why You Shouldn’t Max Out Your 401(k)

Throwback Thursday Classic Post – Thrift Savings Plan Fund Deep Dive – The S Fund

There are only five investments available in the Thrift Savings Plan (TSP), so let’s take a detailed look at them one at a time. In this post we’ll cover the S Fund. You can combine the S Fund with the C Fund to invest in the entire US stock market.

Inception Date

1 MAY 2001

Fund Management

The Federal Retirement Thrift Investment Board currently contracts BlackRock Institutional Trust Company, N.A. (BlackRock) to manage the S Fund assets. The S Fund remains invested regardless of the performance of the securities markets or the overall economy.

Investment Strategy

The S Fund is invested in a stock index fund that invests in small to medium-sized U.S. companies that are not included in the C Fund. The S Fund’s objective is to match the performance of the Dow Jones U.S. Completion TSM Index, which means that when you combine the S Fund and C Fund you are investing in the entire US stock market. Also, some of the money in the S Fund is temporarily invested in the G Fund and earns the G Fund return.

The S Fund is a passively managed fund that remains invested according to its indexed investment strategy regardless of stock market movements or general economic conditions.

What is the Risk?

Your investment in the S Fund is subject to market risk because the prices of the stocks it invests in rise and fall. You are also exposed to inflation risk, meaning your S Fund investment may not grow enough to offset inflation.

What is the Benefit?

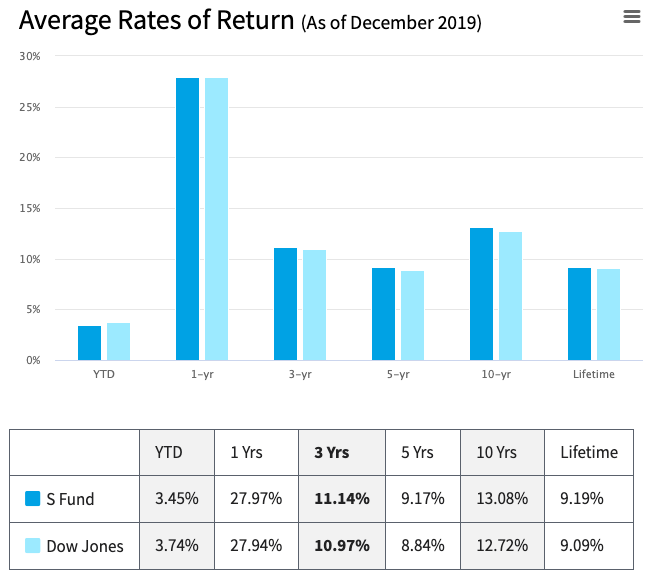

Historically, this increased risk has been rewarded with an increased return. It offers the opportunity to experience gains from equity ownership of small and medium-sized US company stocks. Here is all the performance data as of 24 OCT 2020:

Types of Earnings

The S Fund changes in value as the market price of its stocks change. In addition, the S Fund makes money for its investors when those stocks pay dividends. Unlike a traditional mutual fund, though, income from dividends is included in the share price calculation. It is not paid directly to participants’ accounts.

It also makes some money on interest on short-term investments and securities lending income.

BlackRock credits interest and dividend income each business day. This income is then reflected in the TSP share prices.

Share Price Calculations

The value of your account is determined each business day based on the daily share price and the number of shares you hold. At the end of each business day, after the stock and bond markets have closed, the total value of the funds’ holdings (net of accrued administrative expenses) is divided by the total number of shares outstanding to determine the share price for that day. The daily change in TSP share prices reflects all investment income (interest on short-term investments, dividends, capital gains or losses, and securities lending income) net of TSP administrative expenses.

Expenses

The net expenses paid by investors is 0.042% or 4.2 basis points, which like all the TSP funds is ridiculously low and is a major benefit of the TSP. It cost $0.42 for each $1,000 invested.

How Should I Use the S Fund in my TSP Account?

The S Fund can be useful in a portfolio that also contains stock funds that track other indexes such as the C Fund (which tracks an index of large U.S. company stocks) and the I Fund (which tracks an index of international stocks). The C, S, and I Funds track different segments of the overall stock market without overlapping. This is important because the prices of stocks in each market segment don’t always move in the same direction or by the same amount at the same time. By investing in all segments of the stock market (as opposed to just one), you reduce your exposure to market risk.

The S Fund can also be useful in a portfolio that contains bonds. Again, it is because the prices of stocks and bonds don’t always move in the same direction or by the same amount at the same time. So a retirement portfolio that contains a bond fund like the F Fund, along with other stock funds, like the C and I Funds, will tend to be less volatile than one that contains stock funds alone.

Advice from My Favorite Short Investing Book

Here is what my favorite investing book, The Elements of Investing: Easy Lessons for Every Investor, says about small and mid-cap funds like the S Fund:

The S&P 500 [C Fund in the TSP] represents only about 70 percent of the total value of all stocks traded in the United States. It excludes the 30 percent made up of smaller companies [which are in the S Fund], many of which are the most entrepreneurial and capable of the fastest future growth.

If you want to invest in the entire US stock market, you just combine the C Fund with the S Fund in a 3:1 ratio. To see how I use the S Fund, read the Crush the TSP series.

Fidelity’s Free Mutual Funds

If you read financial blogs or follow the financial news, you’ve probably read multiple articles about Fidelity’s free index mutual funds. Yes…completely free with a 0% expense ratio.

What does this mean for the military investor? Let’s take a look…

What Happened?

All of the major investment companies – Fidelity, Schwab, and Vanguard – are competing for your business by lowering their investment fees. Vanguard has been the low cost leader and used that focus and their unique non-profit structure to become the largest investment company, managing over $5 trillion. For comparison, Fidelity oversees $2.5 trillion. Yes, TRILLION.

Vanguard’s mantra emphasizes the following central tenets of investing:

- The lower your investment fees, the more of the investment return you get to keep.

- Costs last forever.

- You should invest with low cost, broadly diversified index funds.

As you might have guessed, this is what I do at Vanguard and with my Thrift Savings Plan (TSP) accounts.

In 2018, Fidelity announced that they were offering two new mutual funds at no cost – free – to investors with no investment minimums. The funds are the:

- Fidelity ZERO Total Market Index Fund (FZROX) – a diversified US stock index fund

- Fidelity ZERO International Index Fund (FZILX) – a diversified international stock index fund

Everyone was waiting for one of these investment giants to offer free mutual funds. Fidelity became the first.

Fidelity Mania

When this announcement came out, there were countless news articles and blog posts about the free funds. People have been clamoring to switch to Fidelity funds, but a closer look will show you that switching to Fidelity is not guaranteed to be a good move or even what most people trying to minimize their fees should do.

They’re Free! Why Not Switch?

First, Fidelity is not a stupid company. There is no such thing as a free lunch (except for the Thrift Savings Plan G Fund), and they are going to make money from their customers somehow. One way would be by luring you to Fidelity for these free funds, but charging you more on other investments. As the author of this article on Morningstar stated:

But, ultimately, no companies toil for free. What they give away in one place, they recoup in another.

They’ll make up the difference with other funds or brokerage services.

In addition, The White Coat Investor wrote one heck of an article that deep dives on expense ratios and the new Fidelity funds. In it he points out that when you look at equivalent Vanguard, Schwab, and Fidelity funds you’ll see that Vanguard seems to win even with slightly higher expenses and they have a tax efficiency advantage that Schwab and Fidelity don’t have. As he notes:

It just turns out that Vanguard is better at indexing than Fidelity and Schwab. Is that really a surprise to anyone?

I hate to reinvent the wheel, so those interested in the details should really read his article.

What Does This Mean for Investors?

If you are already a Fidelity investor, their drive to compete with Vanguard is going to give you some really useful low cost investment opportunities.

If you are not already a Fidelity investor, realize that if you sell any investments in a regular taxable account (outside of a tax advantaged retirement account like a 401k, IRA, or the TSP), you will have to pay taxes on any capital gains you have. Unless selling won’t generate any taxes (you don’t have any gains) or what you are invested in is an extremely poor choice, I wouldn’t give Uncle Sam some of your money just to save a few hundredths of a percentage point on your expense ratio.

Here’s a good quote from another Morningstar article about the new Fidelity funds that demonstrates how little of a difference these small percentages can have on your bottom line:

To illustrate the modest stakes for your portfolio, let’s look at the growth of a $10,000 investment in Fidelity Total Market Index (FSKAX), Schwab Total Stock Market Index (SWTSX), and Vanguard Total Stock Market Index (VTSAX). Over the years, the three have changed leadership on fees, and investment minimums have changed, too. For the past 10 years, $10,000 in Vanguard Total Stock Market Index would have grown to $28,520, while the Schwab fund would have grown to $28,460 and the Fidelity fund to $28,350. And the differences at times were greater than they are today. So, keep costs low and save as best you can, but don’t worry too much about a couple of basis points.

In addition, you can’t underestimate the benefit of simplicity when it comes to your investment portfolio. I had the TSP and Vanguard. That was it. Then my wife changed employers and now we have a less than optimal 401k with Fidelity that drives me nuts.

While I keep track of everything with a Google spreadsheet and that makes it pretty easy, having yet another website (Fidelity) I have to log in to when I want to make changes is kind of a pain. Don’t underestimate the peace of mind that comes with simplicity, and adding Fidelity to the mix for a few basis points might not be worth the hassle.

If you are just starting out as an investor or you haven’t invested outside of the TSP yet, just realize that you really can’t go wrong with Fidelity, Schwab, or Vanguard as long as you focus on their low cost funds. At Vanguard, all the funds are low cost, so that simplifies your investing life, but Schwab and Fidelity are fine as well.

What’s the Bottom Line?

- If you’re already invested with Fidelity, enjoy the new free funds and use them for your US and international stock investments.

- If you haven’t picked an investment company outside the TSP yet, Fidelity is certainly one to consider but I’d still go with Vanguard if it was up to me.

- You probably should not switch from another company just for free funds, and certainly should not sell anything that would trigger a capital gain just to switch.

The White Coat Investor summarized the strategy you’d employ no matter what company you pick in his article about the Fidelity funds:

There is no new investing strategy going on here. It’s the same old, same old investing strategy – buy all the stocks, hold them, keep your costs and taxes down, and in the long run, your money grows at the same rate as the market and if you save enough, you become financially independent

Change in Catch-Up TSP Contributions and Finance Friday Articles

Here’s a cut/paste from the TSP announcement about a change for catch-up contributions:

Catch-up contributions will soon get easier

Starting in January 2021, we will make the catch-up process easier: if you’re turning 50 or older, you’ll no longer need to make two separate elections each year in order to take advantage of catch-up contributions.

Instead, your contributions will automatically count toward the IRS catch-up limit if you meet the elective deferral limit and keep saving. If you’re eligible for an agency or service match, contributions spilling over toward the catch-up limit will qualify for the match on up to 5% of your salary. Your election will carry over each year unless you submit a new election.

For 2020 catch-up contributions, you do still need to complete the current process and make a separate election. Check current contribution limits to make sure you’re on track this year.

Here are this week’s articles:

- Diagnosing Debt: Demystifying Interest Rates & Loan Terminology

- Does Dry Powder Work?

- Follow the Fed

- Investors Need to Become More Comfortable With Volatility in Their Portfolios

- What If The 4% Rule For Retirement Withdrawals is Now the 5% Rule?

- When You Have Enough, It’s Time to Help Others

- Why Own Bonds When Rates are So Low?

What is an Expense Ratio?

Whether you are managing your investments by yourself or getting help, you need to understand one critical concept, the expense ratio of your investments. Every mutual fund and exchange-traded fund (ETF) that you invest in has an expense ratio, and keeping it as low as possible is key to your long-term financial success.

What is an expense ratio? An expense ratio is the percentage of a fund’s assets that is used for expenses. In other words, if you invest in a mutual fund with a 1% expense ratio and that fund makes 10% in 2020, you’ll only get a 9% return on your investment because 1% goes to pay expenses. The less of your return you use to pay expenses, the more you get to keep.

What is an average expense ratio? An average stock mutual fund has an expense ratio of 0.6% in 2019, but the expense ratios for mutual funds that are similar in their composition can vary wildly. For example, if you look at a list of Standard & Poor 500 index funds offered by investment companies, you’d find expense ratios as low as 0.04% (like the TSP C Fund) and as high as 2.43% (ticker RYSYX). While 2.39% does not seem like that large of a difference, keep in mind that costs last forever and that small differences compounded over years will cost you a lot of money.

Let’s pretend that when you are 25 years old your grandparents give you $10,000 to invest in an S&P 500 index fund for 50 years, during which you earn a 9.5% return. If you invested in an average mutual fund with a 0.6% expense ratio, you would have $683K. If you invested in the Vanguard index fund (another low cost S&P 500 index fund like the TSP C Fund) with a 0.05% expense ratio, you would have $902K. That 0.55% difference in the expense ratios cost you $219K! Small differences in expenses can make huge differences in long-term investment returns, so you need to pay attention to the expense ratios of your investments.

This difference is even more dramatic when you compare actively managed funds to passively managed index funds. Because actively managed funds have higher expense ratios than index funds, it is very difficult for an active manager to beat his/her comparative index over the long-term. This is why I invest 100% in index funds.

When you are picking your investments, keep in mind that you can’t control what happens to the market, but you can control which investments you choose and the expenses that they charge. Any time you are looking to invest in a mutual fund or ETF, you should search for similar funds and compare expense ratios, which you should try to keep below 0.5% (or even 0.25% if possible). Make sure that at a minimum you take a look at the Vanguard version of the investment you are considering since their expense ratios are among the lowest in the industry and they never charge extraneous fees, like loads. There is no reason to pay more expenses for what is essentially the same investment product. It could cost you A TON of money over the long-term.

Finance Friday Articles

It takes a LONG TIME to compile all the articles for Finance Friday, and not that many people click on them, so I’m going to just start listing my favorites instead of my favorites plus the rest of the articles. Here are my favorites this week: