TSP

The Easiest Way to Figure Out Your Optimal TSP Investment Plan

If you invest in the Thrift Savings Plan (TSP), you need to come up with a plan for how you are going to invest. Here is the easiest way to come up with that plan.

Step 1 – Figure Out Your Asset Allocation

In the TSP, you can only invest in two broad asset classes – stocks and bonds. Because of this, the first decision you need to make is how you are going to divide your TSP among these asset classes.

To figure this out, take this Vanguard survey.

At the top of the page it will give you a suggested allocation, such as 80% stocks and 20% bonds. Jot this down somewhere.

Step 2 – Find the TSP Lifecycle Fund That Most Closely Matches This Asset Allocation

Here are the current broad asset allocations of the TSP Lifecycle Funds as of 13 OCT 2019:

| FUND | STOCKS | BONDS |

| L Income | 21% | 79% |

| L 2020 | 26% | 74% |

| L 2030 | 60% | 40% |

| L 2040 | 72% | 28% |

| L 2050 | 82% | 18% |

Pick the one that is closest to your suggested asset allocation from the Vanguard survey. For example, if the survey said you needed 80% stocks and 20% bonds, I’d pick the L 2050 fund because it is closest.

Step 3 – You’re Done

Seriously, it is that simple. I’m not saying this is the best strategy, but it is the easiest and in all honesty, if someone MADE me do this, I’d be fine with it. It is very reasonable way to approach saving for retirement, which is why I’m telling you about it.

Why do I make you take a Vanguard survey instead of just picking the Lifecycle fund that is closest to the year you want to retire? Because the Lifecycle funds are a little too conservative for my tastes and when you compare them with other target date funds. For example, the Lifecycle 2040 is 72% stocks and 28% bonds. The Vanguard Target Retirement Date 2040 is more aggressive at 83% stocks and 17% bonds, which I think is more appropriate.

TSP Fund Deep Dive – The Lifecycle Funds – Hitting the Easy Button

Target date funds are popular. You just pick the approximate year you want to retire, and you invest in the fund that has a year close to that in its name. Nothing could be easier!

Let’s take a look at the Thrift Savings Plan’s (TSP) target date funds – the Lifecycle Funds or L Funds.

Inception Date

1 AUG 2005

Fund Management

The L Funds are invested in the five individual TSP funds based on professionally determined asset allocations.

Investment Strategy

To provide professionally diversified portfolios based on various time horizons, using the G, F, C, S, and I Funds. The objective is to strike an optimal balance between the expected risk and return associated with each fund.

The L Funds’ strategy is to invest in an appropriate mix of the G, F, C, S, and I Funds for a particular time horizon, or target retirement date. The investment mix of each L Fund becomes more conservative as its target date approaches.

The strategy assumes that:

- The greater the number of years you have until retirement, the more willing and able you are to tolerate risk (fluctuation) in your TSP account value to pursue higher rates of return.

- For a given risk level and time horizon, there is an optimal mix of the G, F, C, S, and I Funds that provides the highest expected return.

Each quarter, the L Funds’ target asset allocations change, moving towards a less risky mix of investments as the target date approaches. So if you are invested in one of the L Funds, you will notice that as you get closer to your target date, your allocation to the riskier TSP funds will get smaller while your allocation to the more conservative G Fund gets larger.

The rate of change in the target asset allocation is small when the L Fund target dates are in the distant future. The rate increases as the funds approach their target dates.

When an L Fund has reached its target date, it will be rolled into the L Income Fund. The L Income Fund:

- Is the most conservative of the L Funds.

- Focuses on capital preservation while providing a small exposure to the TSP’s riskier assets (C, S, and I Funds) in order to reduce inflation’s effect on your purchasing power.

- Is designed to produce current income for participants who plan to start withdrawing from their TSP accounts in the near future and for those who are already receiving monthly payments from their accounts.

- Has a set asset allocation that does not change over time.

- The progression from a target date L Fund to the L Income Fund is automatic.

New Lifecycle funds will be added for distant target dates as they are needed.

What is the Risk?

Investors in the L Funds are exposed to all of the types of risk to which the individual TSP funds are exposed. Your account is not guaranteed against loss. The L Funds can have periods of gain and loss, just as the individual TSP funds do.

What is the Benefit?

The L Funds simplify fund selection, and investment risk is reduced through diversification among the five individual TSP funds. You choose the fund that is closest to your target date (or, if your target date falls between the target dates that are offered, you can split your account between the two target date funds closest to your time horizon).

When you invest in the L Funds:

- You can be sure that your TSP account is broadly diversified.

- You don’t have to remember to adjust your investment mix as your target date approaches – it’s done for you.

If you want to see the historical performance of the five L Funds or a visual representation of how the asset allocations change over time, go to this page and click on the tabs:

Types of Earnings

The L Funds earn the weighted average of the earnings of the underlying G, F, C, S, and I Funds calculated in proportion to their L Fund allocation.

Expenses

The net expenses paid by investors is 0.04% or 4 basis points, which like all the TSP funds is ridiculously low and is a major benefit of the TSP. It costs $0.40 for each $1,000 invested.

How Should I Use the L Funds in my TSP Account?

Use the L Funds if you are looking for a simple, low maintenance way of investing money in your TSP account. The L Funds make the investing process easy for you because you do not have to figure out how to diversify your account or how and when to rebalance.

The L Funds are designed so that 100% of your TSP account can be invested in the single L Fund that most closely matches your time horizon (or in the two L Funds closest to your time horizon). Any other use of the L Funds may result in a greater amount of risk in your portfolio than is necessary in order to achieve the same expected rate of return.

Determine the date when, after leaving Federal service, you will need the money that is in your TSP account. Then identify the L Fund that matches your target date:

| Choose | If your target date is: |

|---|---|

| L 2050 | 2045 or later |

| L 2040 | 2035 through 2044 |

| L 2030 | 2025 through 2034 |

| L 2020 | 2019 through 2024 |

| L Income | If you are already withdrawing your account in monthly payments or expect to begin withdrawing before 2019 |

Advice from One of My Favorite Short Investing Books

Here is what one of my favorite investing books, The Little Book of Common Sense Investing: The Only Way to Guarantee Your Fair Share of Stock Market Returns (Little Books. Big Profits), says about target retirement date funds like the L Funds:

Target-date funds can be an excellent choice, not only for investors who are just getting started with their investment programs, but also for investors who decide to adopt a simple strategy for funding their retirement.

TSP Fund Deep Dive – The G Fund – Free Lunches Do Exist

There are only five investments available in the Thrift Savings Plan (TSP), so let’s take a detailed look at them one at a time. In this post we’ll cover the G Fund.

The G Fund is proof that free lunches do actually exist because in the G Fund the government is paying you more interest than they actually should. Read on to find out how and why.

Inception Date

1 APR 1987

Fund Management

Unlike the other TSP funds that are managed by Blackrock, the G Fund is managed internally by the Federal Retirement Thrift Investment Board. The G Fund buys a non-marketable U.S. Treasury security that is guaranteed by the U.S. Government. This means that the G Fund will not lose money.

Investment Strategy

The G Fund invests exclusively in a non-marketable short-term U.S. Treasury security that is specially issued to the TSP. The earnings consist entirely of interest income on the security.

The G Fund’s investment objective is to produce a rate of return that is higher than inflation while avoiding exposure to credit (default) risk and market price fluctuations. It is designed to provide investors with interest income without risk of loss of principal.

What is the Risk?

Your investment in the G Fund is subject to inflation risk, meaning your G Fund investment may not grow enough to offset the reduction in purchasing power that results from inflation.

What is the Benefit?

The payment of G Fund principal and interest is guaranteed by the U.S. Government. This means that the U.S. Government will always make the required payments. In other words, your G Fund investment is not subject to credit (default) risk.

The G Fund interest rate calculation is based on the weighted average yield of all outstanding Treasury notes and bonds with 4 or more years to maturity. As a result, participants who invest in the G Fund are rewarded with a long-term rate on what is essentially a short-term security. Generally, long-term interest rates are higher than short-term rates. This is the free lunch that the government periodically talks about getting rid of.

The G Fund is the lowest risk fund in the TSP and will have the lowest volatility, as you can see below. The major benefit is that you are guaranteed not to lose money. In trade for this you are receiving lower returns. Here is all the performance data as of 8 OCT 2019:

Types of Earnings

The G Fund makes money for its investors with interest paid by the U.S. Government.

Expenses

The net expenses paid by investors is 0.04% or 4 basis points, which like all the TSP funds is ridiculously low and is a major benefit of the TSP. It costs $0.40 for each $1,000 invested. You won’t find a lower cost U.S. government bond fund anywhere.

How Should I Use the G Fund in my TSP Account?

Consider investing in the G Fund if you would like to have all or a portion of your TSP account completely protected from loss. If you choose to invest in the G Fund, you are placing a higher priority on the stability and preservation of your money than on the opportunity to potentially achieve greater long-term growth in your account through investment in the other TSP funds.

It is the TSP equivalent of a U.S. Treasury bond fund you’d find at Vanguard or other investing firms.

Advice from My Favorite Short Investing Book

Here is what my favorite investing book, The Elements of Investing: Easy Lessons for Every Investor, says about U.S. government bond index funds like the G Fund:

The U.S. Treasury issues large amounts of bonds. These issues are considered the safest of all and these bonds are the one type of security where diversification is not essential…High quality bonds can moderate the risk of a common stock portfolio by providing offsetting variations to the inevitable ups and downs or the stock market.

If you want to know how to integrate the G fund into your own TSP investments, read the Crush the TSP series. In particular, step 3 tells you how to figure out how much of your portfolio to devote toward bonds.

TSP Fund Deep Dive – The F Fund

There are only five investments available in the Thrift Savings Plan (TSP), so let’s take a detailed look at them one at a time. In this post we’ll cover the F Fund.

Inception Date

29 JAN 1988

Fund Management

The Federal Retirement Thrift Investment Board currently contracts BlackRock Institutional Trust Company, N.A. (BlackRock) to manage the F Fund assets. The F Fund remains invested regardless of the performance of the securities markets or the overall economy.

Investment Strategy

The F Fund is invested in a bond index fund that invests in government, corporate, and mortgage-backed bonds. The F Fund’s objective is to match the performance of the Bloomberg Barclays U.S. Aggregate Bond Index.

The F Fund is a passively managed fund that remains invested according to its indexed investment strategy regardless of securities market movements or general economic conditions.

What is the Risk?

Your investment in the F Fund is subject to market risk, credit risk, prepayment risk, and inflation risk.

Because the F Fund returns move up and down with the returns in the bond market, your F Fund investment is subject to market risk. For example, when interest rates rise, bond prices (and thus, the returns of the index and the F Fund) fall. Conversely, in an environment of falling interest rates, bond prices, as well as the index and F Fund returns, rise.

As an F Fund investor, you are also exposed to credit (default) risk, or the possibility that principal and interest payments on the bonds that comprise the index will not be paid.

The F Fund is subject to inflation risk, meaning your F Fund investment may not grow enough to offset the reduction in purchasing power that results from inflation.

Your F Fund investment is also exposed to prepayment risk, which is the probability that if interest rates fall, bonds that are represented in the index will be paid back early thus forcing lenders to reinvest at lower rates.

What is the Benefit?

Although there are several types of risks associated with the F Fund, the overall risk is relatively low in comparison to certain other fixed income investments in the market because the F Fund includes only investment-grade securities. As a result, F Fund investors are rewarded with the opportunity to earn higher rates of return over the long term than they would from investments in short-term securities such as the G Fund. Here is all the performance data as of 6 OCT 2019:

Types of Earnings

The F Fund changes in value as the market price of its bond holdings change. In addition, the F Fund makes money for its investors with capital gains (net of trading costs), interest on notes and bonds, interest on short-term investments, and securities lending income.

BlackRock credits interest income each business day. This income is then reflected in the TSP share prices.

Share Price Calculations

The value of your account is determined each business day based on the daily share price and the number of shares you hold. At the end of each business day, after the stock and bond markets have closed, the total value of the funds’ holdings (net of accrued administrative expenses) is divided by the total number of shares outstanding to determine the share price for that day. The daily change in TSP share prices reflects all investment income (interest on short-term investments, dividends, capital gains or losses, and securities lending income) net of TSP administrative expenses.

Expenses

The net expenses paid by investors is 0.041% or 4.1 basis points, which like all the TSP funds is ridiculously low and is a major benefit of the TSP. It cost $0.41 for each $1,000 invested.

How Should I Use the F Fund in my TSP Account?

In periods of falling interest rates, the F Fund will experience gains from the resulting rise in bond prices. So in the long run, you may expect F Fund returns to exceed those of the G Fund; however, you should also expect greater price volatility (up and down movements).

It is also important to know that higher returns are not guaranteed. This is because losses may occur when interest rates are rising, causing bond prices to fall.

The F Fund can be useful in a portfolio that also contains stocks funds. This is because the prices of bonds and stocks don’t always move in the same direction or by the same amount at the same time. So a retirement portfolio that contains stock funds, like the C, S, and I Funds, along with the F Fund, will tend to be less volatile than one that contains stock funds alone.

Advice from My Favorite Short Investing Book

Here is what my favorite investing book, The Elements of Investing: Easy Lessons for Every Investor, says about investment-grade bond index funds like the F Fund:

If indexing has advantages in the stock market, its superiority is even greater in the bond market. You would never want to hold just one bond (such as an IOU from General Motors or Chrysler) in your portfolio – any single bond issuer could get into financial deficiency and be unable to repay you in full. That’s why you need a broadly diversified portfolio of bonds – making a mutual fund essential. And it’s wise to use bond index funds: They have regularly proved superior to actively managed bond funds.

They also say, “Well-diversified portfolios should have holdings of bonds as well as stocks.”

If you want to know how to integrate the F fund into your own TSP investments, read the Crush the TSP series. In particular, step 3 tells you how to figure out how much of your portfolio to devote toward bonds.

TSP Fund Deep Dive – The I Fund – The TSP’s Most Controversial Fund

There are only five investments available in the Thrift Savings Plan (TSP), so let’s take a detailed look at them one at a time. In this post we’ll cover the I Fund, which is the most controversial of all the TSP funds.

What’s all the controversy? You can read about it below, but to give you a preview it is because of two things.

First, investment experts disagree on how much of your investments should go into international stocks, which is what the I Fund is composed of.

Second, the I Fund misses out on a key portion of a comprehensive international stock portfolio, emerging markets. As you’ll read, this second point will soon be fixed.

Inception Date

1 MAY 2001

Fund Management

The Federal Retirement Thrift Investment Board currently contracts BlackRock Institutional Trust Company, N.A. (BlackRock) to manage the I Fund assets. The I Fund remains invested regardless of the performance of the securities markets or the overall economy.

Investment Strategy

The I Fund is invested in a stock index fund that invests in international stocks of more than 20 developed countries. The I Fund’s objective is to match the performance of the MSCI EAFE (Europe, Australasia, Far East) Index. Also, some of the money in the I Fund is temporarily invested in the G Fund and earns the G Fund return.

The I Fund is a passively managed fund that remains invested according to its indexed investment strategy regardless of stock market movements or general economic conditions.

What is the Risk?

Your investment in the I Fund is subject to market risk because the prices of the stocks it invests in rise and fall. You are also exposed to inflation risk, meaning your I Fund investment may not grow enough to offset inflation. Unlike the C or S Funds, you are also exposed to currency risk. What’s that? The TSP defines it as:

The risk that the value of a currency will rise or fall relative to the value of other currencies. Currency risk could affect investments in the I Fund because of fluctuations in the value of the U.S. dollar in relation to the currencies of the 22 countries in the EAFE index.

Because of its exposure to currency risk, the I Fund returns will rise or fall as the value of the U.S. dollar decreases or increases relative to the value of the currencies of the countries represented in the EAFE index.

What is the Benefit?

Historically, this increased risk has been rewarded with an increased return. It offers the opportunity to experience gains from equity ownership of international stocks of more than 20 developed countries. Here is all the performance data as of 29 SEP 2019:

Types of Earnings

The I Fund changes in value as the market price of its stocks change. In addition, the I Fund makes money for its investors when those stocks pay dividends. Unlike a traditional mutual fund, though, income from dividends is included in the share price calculation. It is not paid directly to participants’ accounts. Finally, the I fund will change in value due to currency risk, as described above.

It also makes some money on interest on short-term investments and securities lending income.

BlackRock credits interest and dividend income each business day. This income is then reflected in the TSP share prices.

Share Price Calculations

The value of your account is determined each business day based on the daily share price and the number of shares you hold. At the end of each business day, after the stock and bond markets have closed, the total value of the funds’ holdings (net of accrued administrative expenses) is divided by the total number of shares outstanding to determine the share price for that day. The daily change in TSP share prices reflects all investment income (interest on short-term investments, dividends, capital gains or losses, and securities lending income) net of TSP administrative expenses.

Expenses

The net expenses paid by investors is 0.041% or 4.1 basis points, which like all the TSP funds is ridiculously low and is a major benefit of the TSP. It cost $0.41 for each $1,000 invested.

How Should I Use the I Fund in my TSP Account?

The I Fund can be useful in a portfolio that also contains stock funds that track other indices, such as the C Fund (which tracks an index of large U.S. company stocks) and the S Fund (which tracks an index of small-medium U.S. company stocks). The C, S, and I Funds track different segments of the global stock market without overlapping. This is important because the prices of stocks in each market segment don’t always move in the same direction or by the same amount at the same time. By investing in all segments of the stock market (as opposed to just one), you reduce your exposure to market risk.

The controversy among investment experts, though, is how much of your stock portfolio should be invested internationally. You’ll find respected investment experts who recommend anywhere from 0% of your stocks being invested in international markets (like John Bogle, the founder of Vanguard) to about 50%. An extensive discussion on this can be found in Step 4 of our Crush the TSP Series – Invest. What’s the bottom line? Here is what I think…

A 40% international allocation is between the 0% Bogle viewpoint and the 50% global weighting viewpoint, so it seems fine to me and that is what I do. Ultimately, you can pick anywhere from 0% to 50% and find someone really smart who agrees with you. I’d encourage you to have some exposure to international, so I’d say you should pick at least 20%, but it really is up to you.

The I Fund can also be useful in a portfolio that contains bonds. Again, it is because the prices of stocks and bonds don’t always move in the same direction or by the same amount at the same time. So a retirement portfolio that contains a bond fund like the F Fund, along with other stock funds, like the C and S Funds, will tend to be less volatile than one that contains stock funds alone.

Advice from My Favorite Short Investing Book

Here is what my favorite investing book, The Elements of Investing: Easy Lessons for Every Investor, says about international stock funds like the I Fund:

We do believe that investors should combine one of the total U.S. stock market index funds with a total international stock market index fund.

How do you do this with the TSP? Well…you can’t, and that is why the I Fund is controversial.

If you want to invest in the total US stock market, you just combine the C Fund with the S Fund in a 3:1 ratio. To see how I use the S Fund, read the Crush the TSP series.

But you cannot invest in a total international stock market index fund in the TSP because the I Fund is its only international stock option and it does not invest in emerging markets. Emerging markets include some of the largest economies in the world, like China and India. You can read more about emerging markets here.

As part of upcoming changes to the TSP, the I Fund is switching its index to include emerging markets. They are going to be switching to the MSCI All Country World Index Ex-U.S. index. This index is broader and includes both developed and emerging markets.

Overall, this is a good thing. The current I Fund doesn’t provide worldwide stock representation, but the new one will. Original reports stated that the change was slated to take effect in early 2019, but as of SEP 2019 it has not occurred yet.

Once this change occurs, you’ll be able to use the TSP to invest in a total international stock market index fund because that is what the I Fund will be.

Thrift Savings Plan Fund Deep Dive – The S Fund

There are only five investments available in the Thrift Savings Plan (TSP), so let’s take a detailed look at them one at a time. In this post we’ll cover the S Fund. You can combine the S Fund with the C Fund to invest in the entire US stock market.

Inception Date

1 MAY 2001

Fund Management

The Federal Retirement Thrift Investment Board currently contracts BlackRock Institutional Trust Company, N.A. (BlackRock) to manage the S Fund assets. The S Fund remains invested regardless of the performance of the securities markets or the overall economy.

Investment Strategy

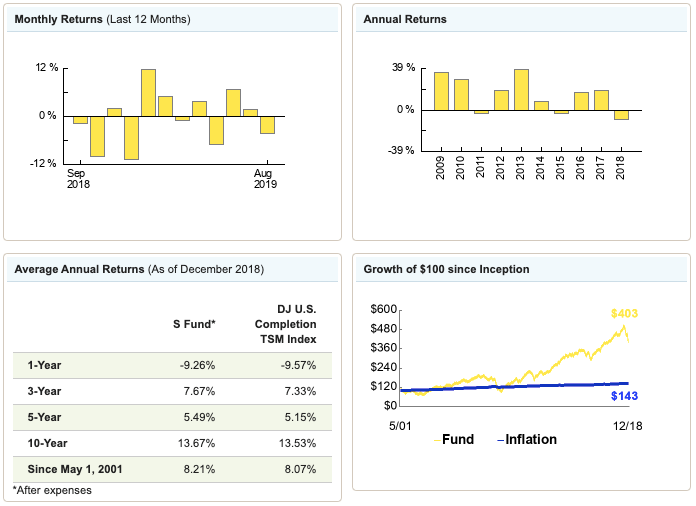

The S Fund is invested in a stock index fund that invests in small to medium-sized U.S. companies that are not included in the C Fund. The S Fund’s objective is to match the performance of the Dow Jones U.S. Completion TSM Index, which means that when you combine the S Fund and C Fund you are investing in the entire US stock market. Also, some of the money in the S Fund is temporarily invested in the G Fund and earns the G Fund return.

The S Fund is a passively managed fund that remains invested according to its indexed investment strategy regardless of stock market movements or general economic conditions.

What is the Risk?

Your investment in the S Fund is subject to market risk because the prices of the stocks it invests in rise and fall. You are also exposed to inflation risk, meaning your S Fund investment may not grow enough to offset inflation.

What is the Benefit?

Historically, this increased risk has been rewarded with an increased return. It offers the opportunity to experience gains from equity ownership of small and medium-sized US company stocks. Here is all the performance data as of 26 SEP 2019:

Types of Earnings

The S Fund changes in value as the market price of its stocks change. In addition, the S Fund makes money for its investors when those stocks pay dividends. Unlike a traditional mutual fund, though, income from dividends is included in the share price calculation. It is not paid directly to participants’ accounts.

It also makes some money on interest on short-term investments and securities lending income.

BlackRock credits interest and dividend income each business day. This income is then reflected in the TSP share prices.

Share Price Calculations

The value of your account is determined each business day based on the daily share price and the number of shares you hold. At the end of each business day, after the stock and bond markets have closed, the total value of the funds’ holdings (net of accrued administrative expenses) is divided by the total number of shares outstanding to determine the share price for that day. The daily change in TSP share prices reflects all investment income (interest on short-term investments, dividends, capital gains or losses, and securities lending income) net of TSP administrative expenses.

Expenses

The net expenses paid by investors is 0.040% or 4 basis points, which like all the TSP funds is ridiculously low and is a major benefit of the TSP. It cost $0.40 for each $1,000 invested.

How Should I Use the S Fund in my TSP Account?

The S Fund can be useful in a portfolio that also contains stock funds that track other indexes such as the C Fund (which tracks an index of large U.S. company stocks) and the I Fund (which tracks an index of international stocks). The C, S, and I Funds track different segments of the overall stock market without overlapping. This is important because the prices of stocks in each market segment don’t always move in the same direction or by the same amount at the same time. By investing in all segments of the stock market (as opposed to just one), you reduce your exposure to market risk.

The S Fund can also be useful in a portfolio that contains bonds. Again, it is because the prices of stocks and bonds don’t always move in the same direction or by the same amount at the same time. So a retirement portfolio that contains a bond fund like the F Fund, along with other stock funds, like the C and I Funds, will tend to be less volatile than one that contains stock funds alone.

Advice from My Favorite Short Investing Book

Here is what my favorite investing book, The Elements of Investing: Easy Lessons for Every Investor, says about small and mid-cap funds like the S Fund:

The S&P 500 [C Fund in the TSP] represents only about 70 percent of the total value of all stocks traded in the United States. It excludes the 30 percent made up of smaller companies [which are in the S Fund], many of which are the most entrepreneurial and capable of the fastest future growth.

If you want to invest in the entire US stock market, you just combine the C Fund with the S Fund in a 3:1 ratio. To see how I use the S Fund, read the Crush the TSP series.

Thrift Savings Plan Fund Deep Dive – The C Fund

There are only five investments available in the Thrift Savings Plan (TSP), so let’s take a detailed look at them one at a time. First, we’ll cover the C Fund, which would probably be the fund you would pick if you were only allowed to pick one.

Inception Date

29 JAN 1988

Fund Management

The Federal Retirement Thrift Investment Board currently contracts BlackRock Institutional Trust Company, N.A. (BlackRock) to manage the C Fund assets. The C Fund remains invested regardless of the performance of the securities markets or the overall economy.

Investment Strategy

The C Fund is invested in a stock index fund that fully replicates the Standard and Poor’s 500 (S&P 500) Index, a broad market index made up of the stocks of 500 large to medium-sized U.S. companies. The C Fund’s objective is to match the performance of the S&P 500. Also, some of the money in the C Fund is temporarily invested in the G Fund and earns the G Fund return.

The C Fund is a passively managed fund that remains invested according to its indexed investment strategy regardless of stock market movements or general economic conditions.

What is the Risk?

Your investment in the C Fund is subject to market risk because the prices of the stocks in the S&P 500 Index rise and fall. You are also exposed to inflation risk, meaning your C Fund investment may not grow enough to offset inflation.

What is the Benefit?

Historically, this increased risk has been rewarded with an increased return. It offers the opportunity to experience gains from equity ownership of large and mid-sized U.S. company stocks. Here is all the performance data as of 25 SEP 2019:

Types of Earnings

The C Fund changes in value as the market price of its stocks change. In addition, the C Fund makes money for its investors when those stocks pay dividends. Unlike a traditional mutual fund, though, income from dividends is included in the share price calculation. It is not paid directly to participants’ accounts.

It also makes some money on interest on short-term investments and securities lending income.

BlackRock credits interest and dividend income each business day. This income is then reflected in the TSP share prices.

Share Price Calculations

The value of your account is determined each business day based on the daily share price and the number of shares you hold. At the end of each business day, after the stock and bond markets have closed, the total value of the funds’ holdings (net of accrued administrative expenses) is divided by the total number of shares outstanding to determine the share price for that day. The daily change in TSP share prices reflects all investment income (interest on short-term investments, dividends, capital gains or losses, and securities lending income) net of TSP administrative expenses.

Expenses

The net expenses paid by investors is 0.041% or 4.1 basis points, which like all the TSP funds is ridiculously low and is a major benefit of the TSP. It cost $0.41 for each $1,000 invested.

How Should I Use the C Fund in my TSP Account?

The C Fund can be useful in a portfolio that also contains stock funds that track other indexes such as the S Fund (which tracks an index of small US company stocks) and the I Fund (which tracks an index of international stocks). The C, S, and I Funds track different segments of the overall stock market without overlapping. This is important because the prices of stocks in each market segment don’t always move in the same direction or by the same amount at the same time. By investing in all segments of the stock market (as opposed to just one), you reduce your exposure to market risk.

The C Fund can also be useful in a portfolio that contains bonds. Again, it is because the prices of stocks and bonds don’t always move in the same direction or by the same amount at the same time. So a retirement portfolio that contains a bond fund like the F Fund, along with other stock funds, like the S and I Funds, will tend to be less volatile than one that contains stock funds alone.

Advice from My Favorite Short Investing Book

Here is what my favorite investing book, The Elements of Investing: Easy Lessons for Every Investor, says about S&P 500 index funds like the C Fund:

The best-known of the broad stock market mutual funds and Exchange Traded Funds (ETFs) in the US track the S&P 500 index of the largest stocks. We prefer using a broader index that includes more smaller-company stocks…Funds that track these broader indexes are often referred to as ‘total stock market’ index funds. More than 80 years of stock market history confirm that portfolios of smaller stocks have produced a higher rate of return than the return of the S&P 500 large-company index. While smaller companies are undoubtedly less stable and riskier that large firms, they are likely – on average – to produce somewhat higher future returns. Total stock market index funds are the better way for investors to benefit from the long-run growth of economic activity.

If you want to follow their advice, you just combine the C Fund with the S Fund in a 3:1 ratio. To see how I use the C Fund, read the Crush the TSP series.

Step 6 to Crush the TSP – Rebalance Annually

We’ve talked about steps 1-5 to crush the Thrift Savings Plan (TSP). Now we move on to the final step (unless I think of more), step 6 – rebalance annually.

What is Rebalancing?

Let’s say that your desired TSP asset allocation is 70% stocks and 30% bonds. After the last year, though, stocks earned more than bonds and now you’re sitting at 85% stocks and 15% bonds. In order to rebalance back to your desired asset allocation, you’d sell approximately 15% of your stocks and buy bonds, restoring your desired asset allocation. It’s that simple.

Why Should You Rebalance?

If you don’t, you may be assuming more or less risk than you desire.

Also, by rebalancing you force yourself to sell what has overperformed and buy what has underperformed. Although this seems counter-intuitive because you are selling what has given you the largest return, by doing this you are systematically selling high and buying low. When left to themselves, investors typically buy high and sell low, the opposite of what you want to do. Rebalancing forces you to do it right.

How Often Should You Rebalance?

Vanguard has researched this, and you can read their full report here:

Best Practices for Portfolio Rebalancing

Their conclusion is:

We conclude that for most broadly diversified stock and bond fund portfolios (assuming reasonable expectations regarding return patterns, average returns, and risk), annual or semiannual monitoring, with rebalancing at 5% thresholds, is likely to produce a reasonable balance between risk control and cost minimization for most investors.

In other words, you rebalance annually or semiannually (twice per year) whenever your current asset allocations are off by 5% or more from your desired allocations. If the current and desired allocations are within 5% of each other, you do nothing.

How Do You Rebalance in the TSP?

You just log on and do what they call an “interfund transfer” or IFT. You can read all about it on this page from the TSP website.

Because you are doing it in a tax-advantaged retirement account, there are no expenses, fees, or taxes associated with rebalancing (unlike if you were rebalancing a taxable account).

You can only do it twice per month without restrictions, but since you are smart you are only doing it once per year anyway.

Do You Need to Rebalance With Lifecycle Funds?

No, you don’t. This is one of the major advantages of the L funds. If you are hitting the easy button on your TSP and just using a Lifecycle fund, you don’t need to rebalance…EVER!

That’s It. Crush the TSP!

That’s the final step to crush it in your TSP account. Read the whole series, maximize your TSP contributions, and get rich in the military.

Step 5 to Crush the TSP – Roth vs Traditional

We’ve talked about steps 1-4 to crush the Thrift Savings Plan (TSP). Now we’re on to step 5, deciding between the Roth vs traditional TSP. Let’s take a look at the difference between the two and help you to decide which is the right choice for you.

The Traditional TSP

The traditional TSP is the first of two potential tax treatments for your TSP contributions. If you elect it, you defer paying taxes on your contributions and their earnings until you withdraw them. This is the only option for any money you get as a result of the 5% government match in the new Blended Retirement System (BRS).

If you are in a combat zone making tax-free contributions, your contributions will be tax-free at withdrawal but your earnings will be subject to tax.

The Roth TSP

The Roth TSP is the second of two potential tax treatments for your TSP contributions. If you contribute to it, you pay taxes on your contributions now and your earnings are tax-free at withdrawal.

The Roth TSP is similar to a Roth 401(k) that a civilian would have, not a Roth IRA. There are no income limits for Roth TSP contributions. You can contribute to both your Roth TSP and a Roth IRA without contributions to one affecting how much you can contribute to the other. For example, in 2019 you can contribute the full $19,000 to your Roth TSP and $6,000 to your Roth IRA.

Which One is Best for You?

Here’s a table that compares the two options from the TSP website:

| The Treatment of… | Traditional TSP | Roth TSP |

|---|---|---|

| Contributions | Pre-tax | After-tax1 |

| Your Paycheck | Taxes are deferred*, so less money is taken out of your paycheck. | Taxes are paid up front*, so more money comes out of your paycheck. |

| Transfers In | Transfers allowed from eligible employer plans and traditional IRAs | Transfers allowed from Roth 401(k)s, Roth 403(b)s, and Roth 457(b)s |

| Transfers Out | Transfers allowed to eligible employer plans, traditional IRAs, and Roth IRAs2 | Transfers allowed to Roth 401(k)s, Roth 403(b)s, Roth 457(b)s, and Roth IRAs3 |

| Withdrawals | Taxable when withdrawn | Tax-free earnings if five years have passed since January 1 of the year you made your first Roth contribution, AND you are age 59½ or older, permanently disabled, or deceased |

* If you are a member of the uniformed services receiving tax-exempt pay (i.e., pay that is subject to the combat zone tax exclusion), your contributions from that pay will also be tax-exempt.

1. Roth contributions are subject to Federal (and, where applicable, state and local) income taxes, while traditional contributions are not taxed until withdrawn. However, both Roth contributions and traditional contributions are included in the amount of wages used to calculate payroll taxes (e.g., Social Security taxes).

2. You would have to pay taxes on any pre-tax amount transferred to a Roth IRA.

3. Transfers to a Roth IRA from a Roth TSP are not subject to the income restrictions that apply to Roth IRA contributions.

The issue of whether Roth is a good option for you was discussed in this TSP Highlights called Is Roth For You?

If you are more of a visual learner, you might enjoy this video from the TSP called “Is Roth Right for Me?”

If you like interactive calculators, this one from Betterment is pretty good.

If you don’t trust anything I say and want to read what someone else thinks, I don’t blame you. Here’s a good article from Money.

The decision really boils down to whether you’d like to pay taxes now (Roth) or later (traditional) and how your current tax rate compares to your likely future tax rate during retirement. While predicting the future is not easy, if you are young or early in your career, your earnings and tax rate are likely to rise in the future, so you should probably lean toward the Roth option. If you are in your peak earning years and you expect your tax rate to fall in retirement, you should probably lean toward the traditional and defer taxes to a future date.

If you are not sure which option to choose, many people recommend you diversify your retirement accounts and simply split the Roth and traditional 50/50. That way in the future you’ll have options depending on how future tax rates and your financial situation changes.

What do I do? I can afford the taxes now and want as much tax-free money available to me as I can get, so I put all the money in the Roth TSP that I can. That said, the first part of my career I didn’t have a Roth option, so a large percentage of my TSP balance is in the traditional TSP as well, so I’m about 50/50 split between the two options.

Some Rules to Be Aware Of

The TSP keeps your traditional and Roth money in separate “buckets” in your TSP account.

You cannot convert any portion of your existing traditional TSP balance to a Roth balance.

You can make both traditional and Roth contributions if you want. You can contribute in any percentages or amounts you choose and can change your election at any time.

If you are getting government contributions (perhaps because you are in the Blended Retirement System), they are deposited into your traditional TSP. You can put your portion in the Roth, but the government’s portion must go in the traditional.

The Bottom Line

Use the resources above to decide if you want to invest in the traditional TSP, the Roth TSP, or some combination of the two. If you’re not sure what to do, I’d just split it 50/50 so you have options in the future.

Keep your eye out for the last step to crush the TSP, rebalancing.

Step 3 to Crush the Thrift Savings Plan – Asset Allocation

The Thrift Savings Plan (TSP) is the military’s retirement account. Learning how to maximize its utility should be high on your financial priority list. At MCCareer.org, I’m going to create a guide that will show you how to crush it with the TSP. We already showed you step 1 and step 2 in that guide. Here’s step 3…

The 3rd Step to Crush the TSP – Asset Allocation

You’ve probably heard that you shouldn’t put all of your eggs in one basket. That is what asset allocation is all about…making sure your eggs are in multiple baskets.

Asset allocation can be complex. There are entire books written about nothing but asset allocation, like The Intelligent Asset Allocator: How to Build Your Portfolio to Maximize Returns and Minimize Risk. That’s a good book if you want to nerd out, but I’m going to try and simplify asset allocation for you.

What Assets are Available in the TSP?

There are only five assets available:

- G Fund – US government bonds specially issued to the TSP

- F Fund – US government, corporate, and mortgage-backed bonds

- C Fund – stocks of large and medium-sized US companies

- S Fund – stocks of small to medium-sized US companies (not included in the C Fund)

- I Fund – international stocks of more than 20 developed countries (soon to include emerging markets)

What is not available? There are a few major asset classes unavailable. You cannot invest in real estate or international bonds. International emerging markets will be added to the I Fund soon but are not currently available. If you want exposure to any of these asset classes right now, you’ll have to get them in your other investment accounts, like your IRA or taxable account.

How Do I Pick My Asset Allocation?

If in step 2 you decided to use L Funds, you don’t need to pick an asset allocation for your TSP. The L Fund takes care of it for you.

If you are not going to use L Funds, one way to decide on an asset allocation is to take this Vanguard survey. At the top of the page it will give you a suggested allocation, such as 80% stocks and 20% bonds.

Another way is to borrow from trusted investment experts. Here are a few opinions.

In The Elements of Investing: Easy Lessons for Every Investor

, Burton Malkiel recommends these age-based asset allocations:

- 20-30s – bonds 10-25%, stocks 75-90%

- 40-50s – bonds 25-35%, stocks 65-75%

- 60s – bonds 35-55%, stocks 45-65%

- 70s – bonds 50-65%, stocks 35-50%

- 80s+ – bonds 60-80%, stocks 20-40%

In the same book, Charlie Ellis recommends these asset allocations:

- 20-30s – bonds 0%, stocks 100%

- 40s – bonds 0-10%, stocks 90-100%

- 50s – bonds 15-25%, stocks 75-85%

- 60s – bonds 20-30%, stocks 70-80%

- 70s – bonds 40-60%, stocks 40-60%

- 80s+ – bonds 50-70%, stocks 30-50%

Mr. Ellis is a little more aggressive than Mr. Malkiel because he recommends a higher allocation of stocks.

There are other ways to come up with a reasonable asset allocation, such as financial “rules of thumb.” The founder of Vanguard, John Bogle, is famous for creating the “age in bonds” rule of thumb. It says that whatever your age is, that is the percentage of your investments that should be in bonds. The rest should be in stocks.

For example, I’m 43 years old, so his rule would say I should have 43% in bonds and 57% in stocks.

This rule has been criticized as being too conservative, so some have changed it to 110 or 120 minus your age as the percentage you should have in stocks. For example, for me this would mean:

- 110 minus age 43 = 67% in stocks, the rest (33%) in bonds

- 120 minus age 43 = 77% in stocks, the rest (23%) in bonds

There are certainly other ways to come up with your asset allocation. You could ask a financial advisor. You could read other books. You could read other blog posts, like this one on the Bogleheads Wiki.

What About Other Assets Like Your Pension and Social Security?

This is a tough issue. Some would argue that pensions and social security are income streams and that they should not play into your asset allocation decision. This is what Vanguard argues. Others would argue that they are “bond-like” and should be factored into your asset allocation and counted as a large pile of bonds. Here are a few thoughts on the subject from blogs I follow and trust:

- The Oblivious Investor – How Pensions and Social Security Affect Asset Allocation

- Humble Dollar – A Price on Your Head

The Bottom Line – Asset Allocation

Somehow you have to figure out your desired asset allocation. The info above will hopefully facilitate that. Once you have a target asset allocation, now you have to apply it to the investments available in the TSP. Take the 4th Step…invest.

- ← Previous

- 1

- …

- 3

- 4

- 5

- Next →